Breaking Point? The Impending Credit Crunch in America

Get ready for America's looming credit crunch!

We anticipate that the US economy is either heading for or already in a credit crunch, which will worsen with an additional rate hike from the Federal Reserve in June or July. Today’s Daily Insight will focus on some of the most telling charts that provide valuable insights into US credit growth.

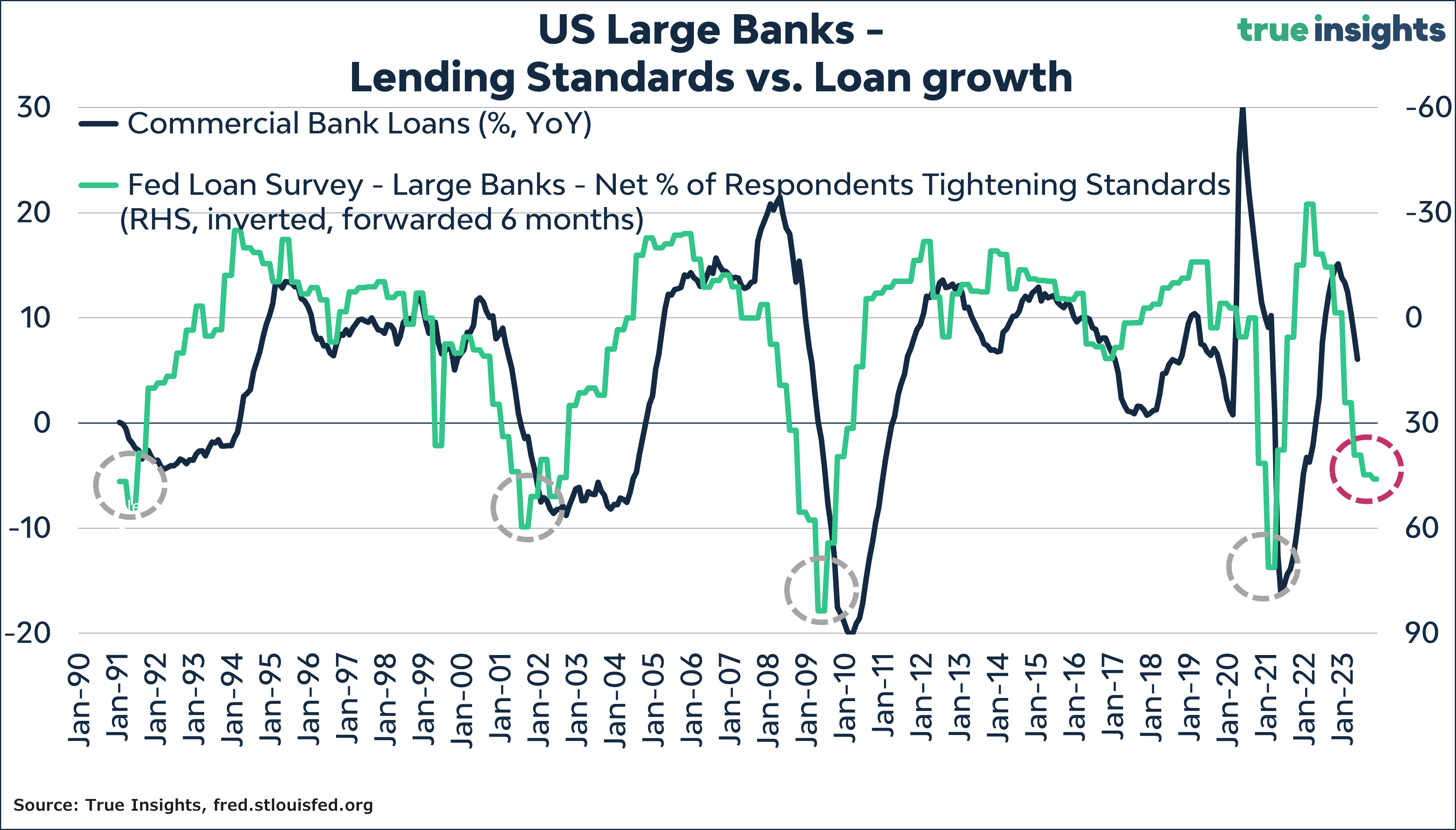

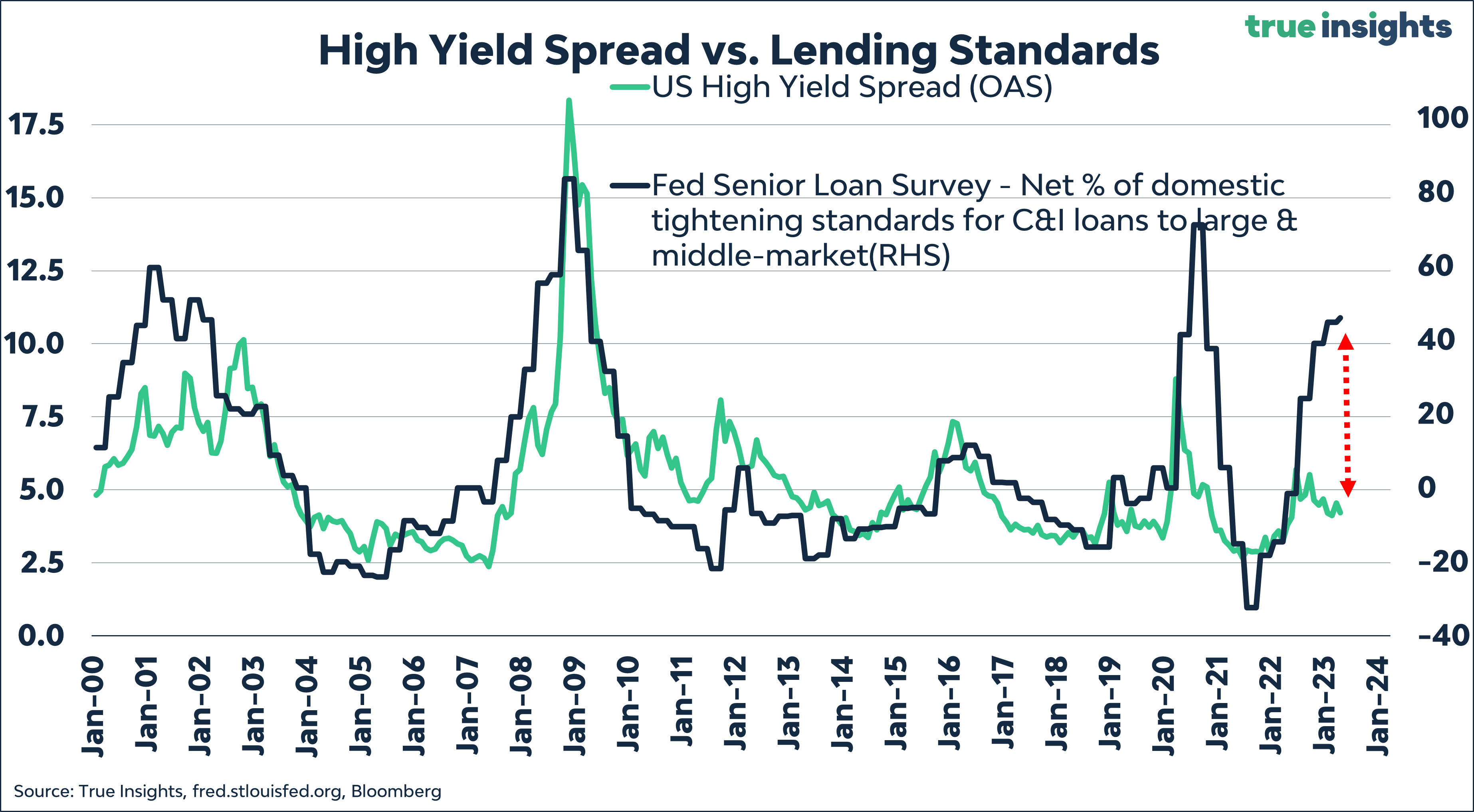

Obviously, the tightening of lending standards, as reported in the Fed Senior Loan Survey, is key here. As the chart reveals, since the beginning of 2022, lending standards have significantly tightened. Last year, tighter financial conditions played a decisive role in the performance of financial markets. Despite the recovery observed in the markets this year, lending standards have continued to worsen, pointing to negative (year-on-year) loan growth going forward.

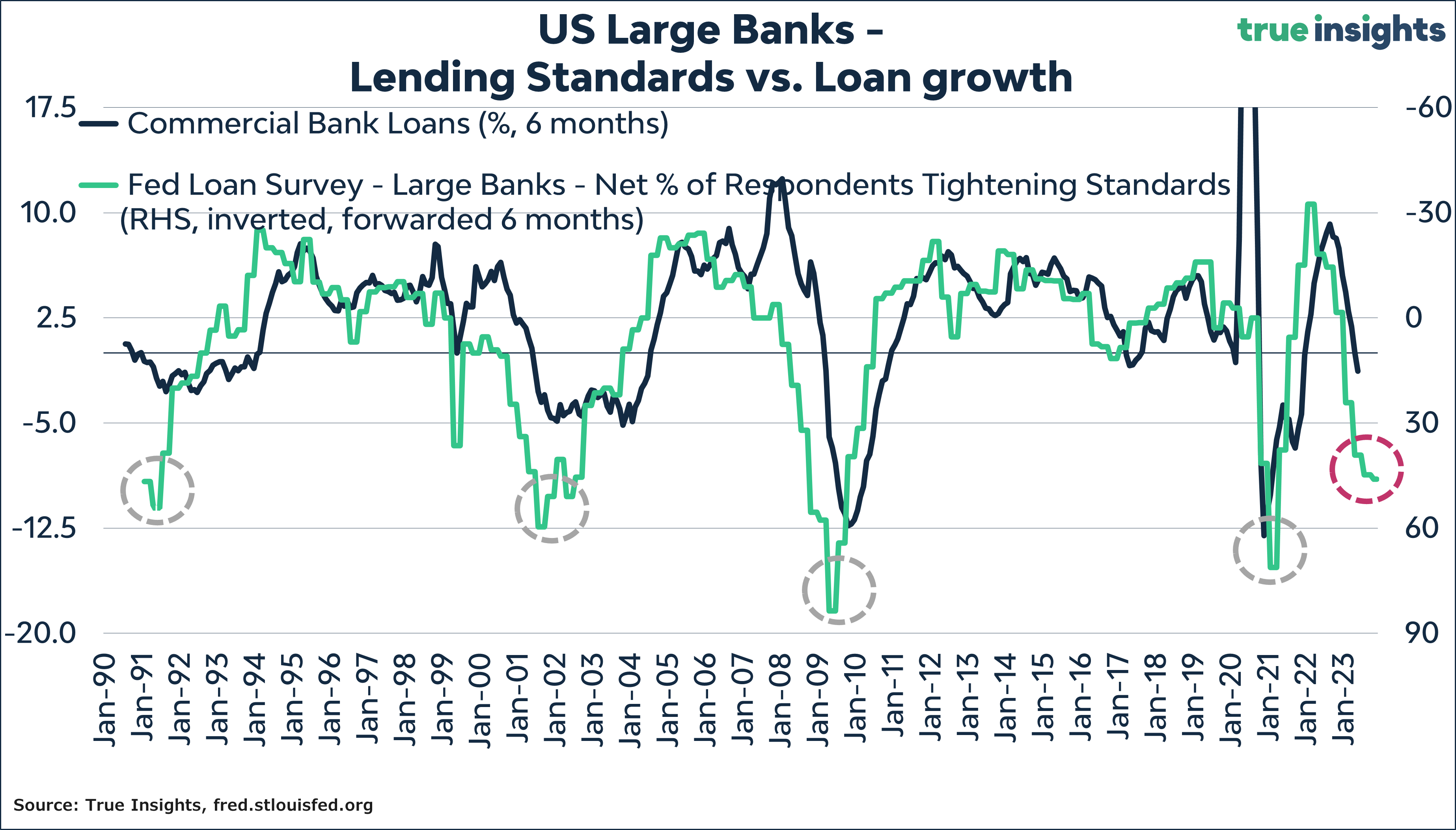

Focusing on more recent developments – in this case, the last six months – reveals that credit growth of large US banks has turned negative. However, the very tight lending standards suggest that the decline in loan growth will accelerate in the coming months and quarters.

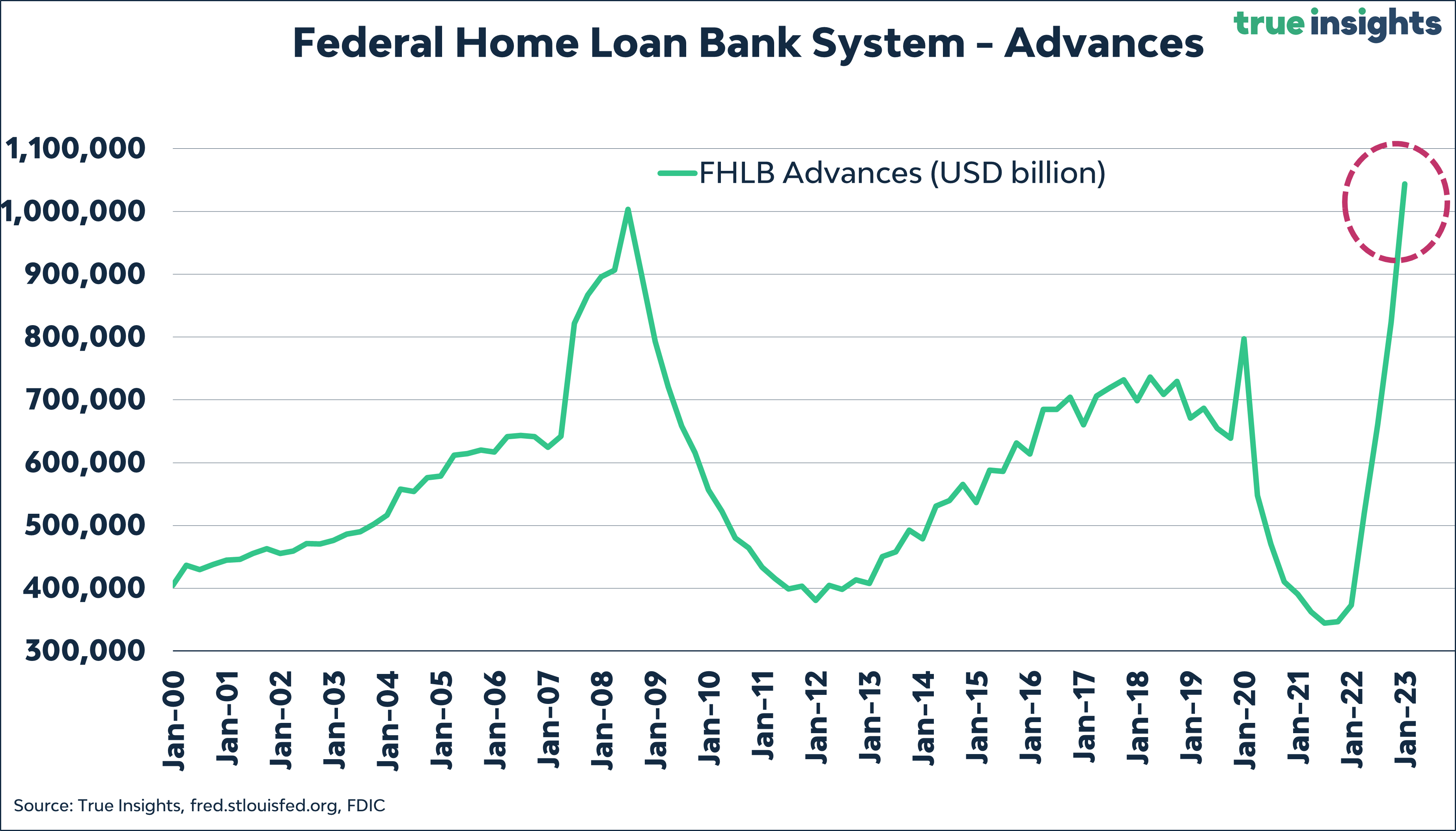

While often overlooked, the advances disbursed by the Federal Home Loan Bank System (FHLB) represent a crucial measure of liquidity. Functioning as a lender-of-last-resort alongside the Federal Reserve, the FHLB system was established to support homeownership following the Great Depression. But in recent times, it has also served as an early indicator of rising banking stress. For instance, during the second half of 2007, FHLB advances spiked by nearly USD 230 billion, while there was no such activity at the Fed’s Discount Window. Although linking increases in FHLB advances to rising banking stress is not always straightforward due to their common usage by banks, the expansion observed in the last two quarters, if deemed stress-related, indicates that banks required approximately USD 380 billion in additional liquidity.

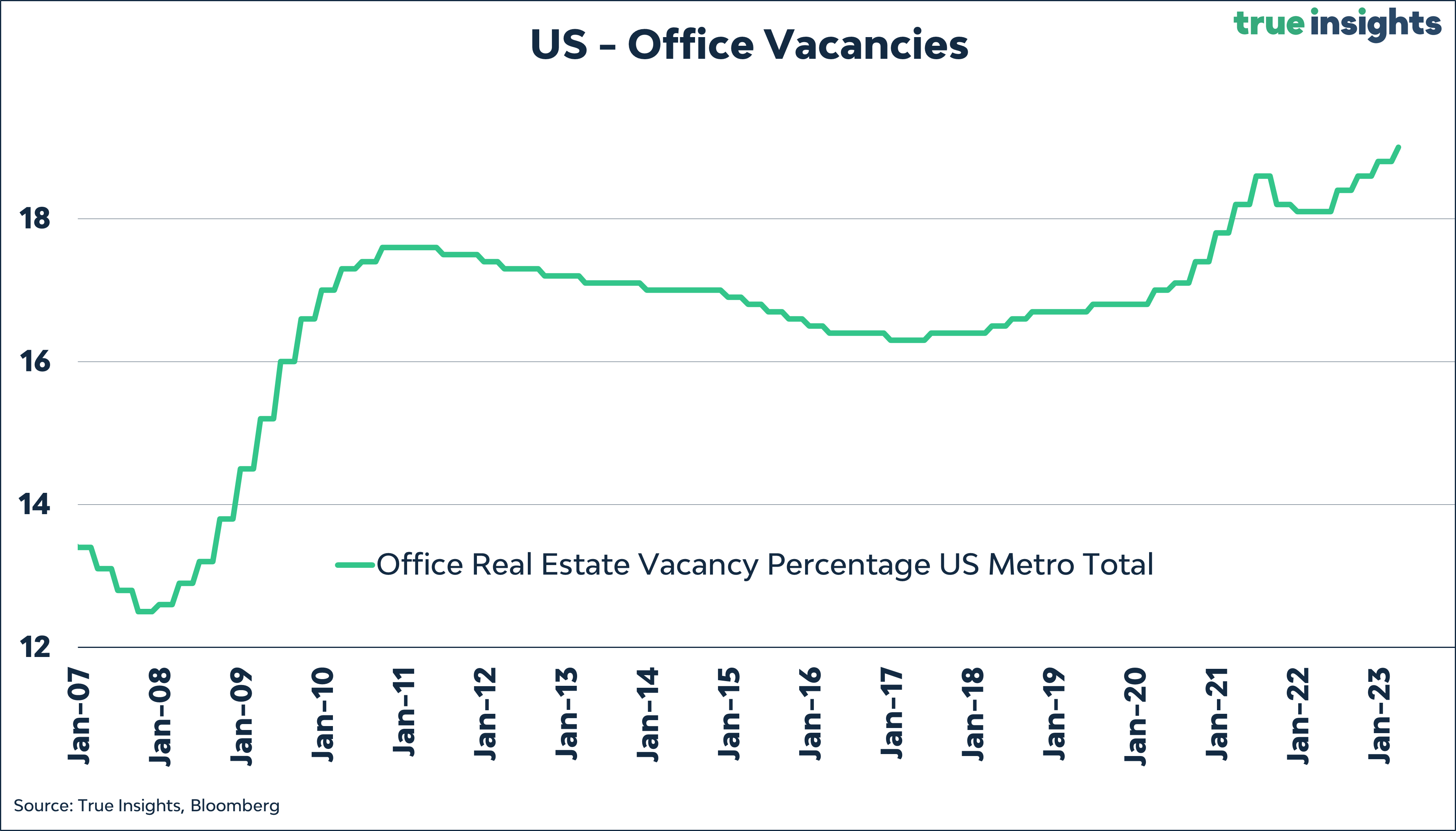

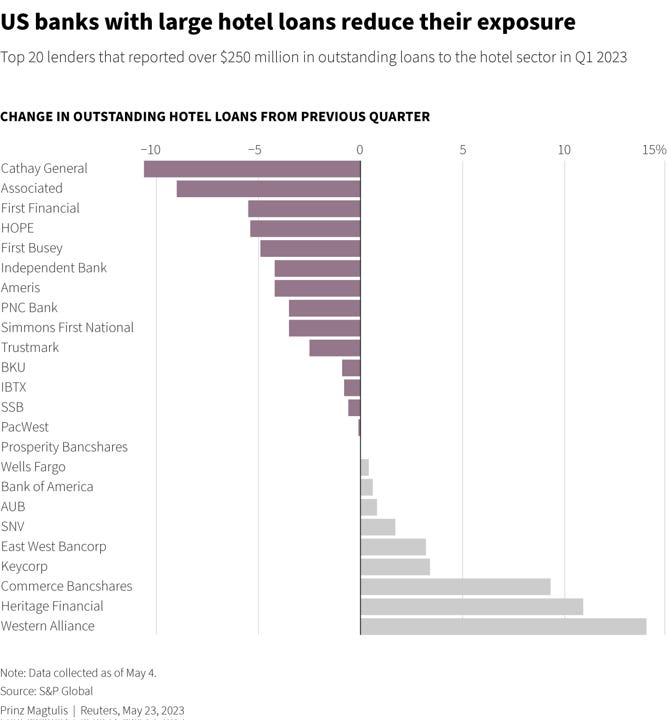

Another area facing challenges is the refinancing of Commercial Real Estate (CRE). CRE values are under significant pressure due to the highest office vacancy rate on record, amongst others. With banks reluctant to increase their loan-to-value ratios, property owners and managers are encountering difficulties in securing refinancing. In most cases, refinancing requires the injection of additional equity capital, and failure to do so may lead to default.

Moreover, the commercial real estate credit crunch extends beyond offices.

Prominent hotel companies such as Hilton and Marriott have warned about reduced hotel development due to expensive and less available credit. Following the collapse of several banks, regional lenders have reduced their exposure to commercial real estate development by tightening lending standards and reducing loan volume. Private equity firms have stepped in to provide construction loans, albeit at higher costs. Interest rates have more than doubled in the past two-and-a-half years, increasing from 4% to 9-10% today.

High Yield is the one to watch here

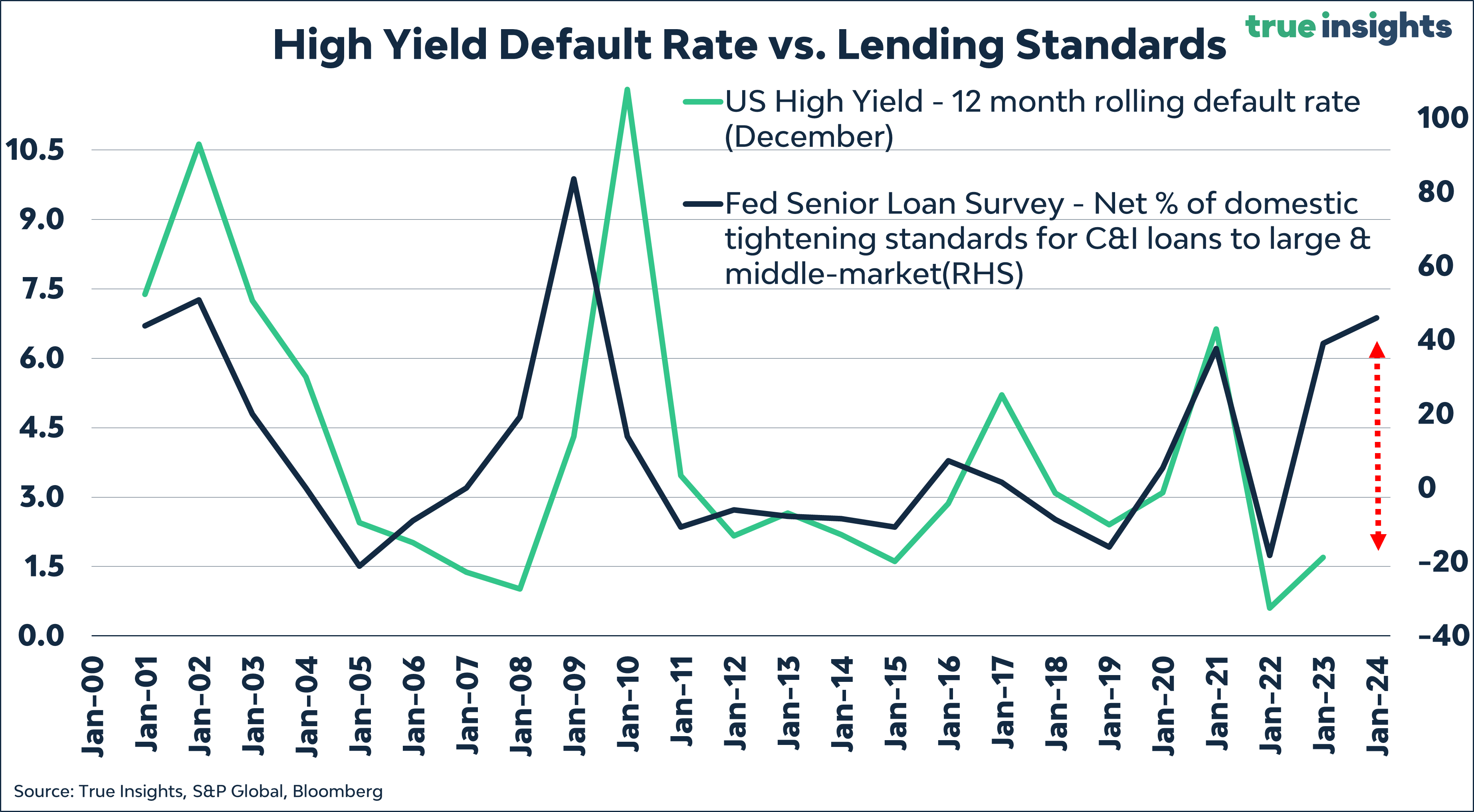

Whenever a credit crunch occurs, a cycle of defaults usually accompanies it. As shown in the chart below, rising defaults have always coincided with stricter lending standards. Based on the historical relationship between changes in lending standards and defaults, the US high yield default rate will likely quadruple this year, surpassing 7% compared to last year’s 1.7%.

Deutsche Bank recently issued a warning stating that a wave of defaults is imminent. Their forecast predicts that by the end of 2024, the US high-yield default rate will peak at 9. In Europe, the speculative-default rate is expected to rise, albeit at a more moderate pace, reaching 5.8%.

Yet, high yield bond spreads refuse to reflect even the slightest possibility of this scenario. In fact, both US and global high yield bond spreads have decreased in recent weeks. Consequently, we remain underweight Global High Yield Bonds.