Company Earnings: They will go, and expectations are far from excessive

Company Earnings: They will go, and expectations are far from excessive

The odds of an earnings recession have come down massively. But better, investor expectations are not too upbeat at all!

As highlighted in last Friday’s Weekly Market Monitor, an uptick in macroeconomic momentum is one of the reasons why equities seem reluctant to undergo a significant correction. A result of this is the improvement in the outlook on earnings. Three out of my four global earnings bellwethers confirm this trend.

Earnings Bellwethers

The four global earnings-per-share bellwethers are:

Singapore electronics exports

Global semiconductor sales

South Korean exports

Chinese producer prices

Singapore Electronics Exports

Singapore’s electronics exports have shown substantial improvement lately, indicating an increase in earnings (per-share) of about 8% for companies in the MSCI World Index.

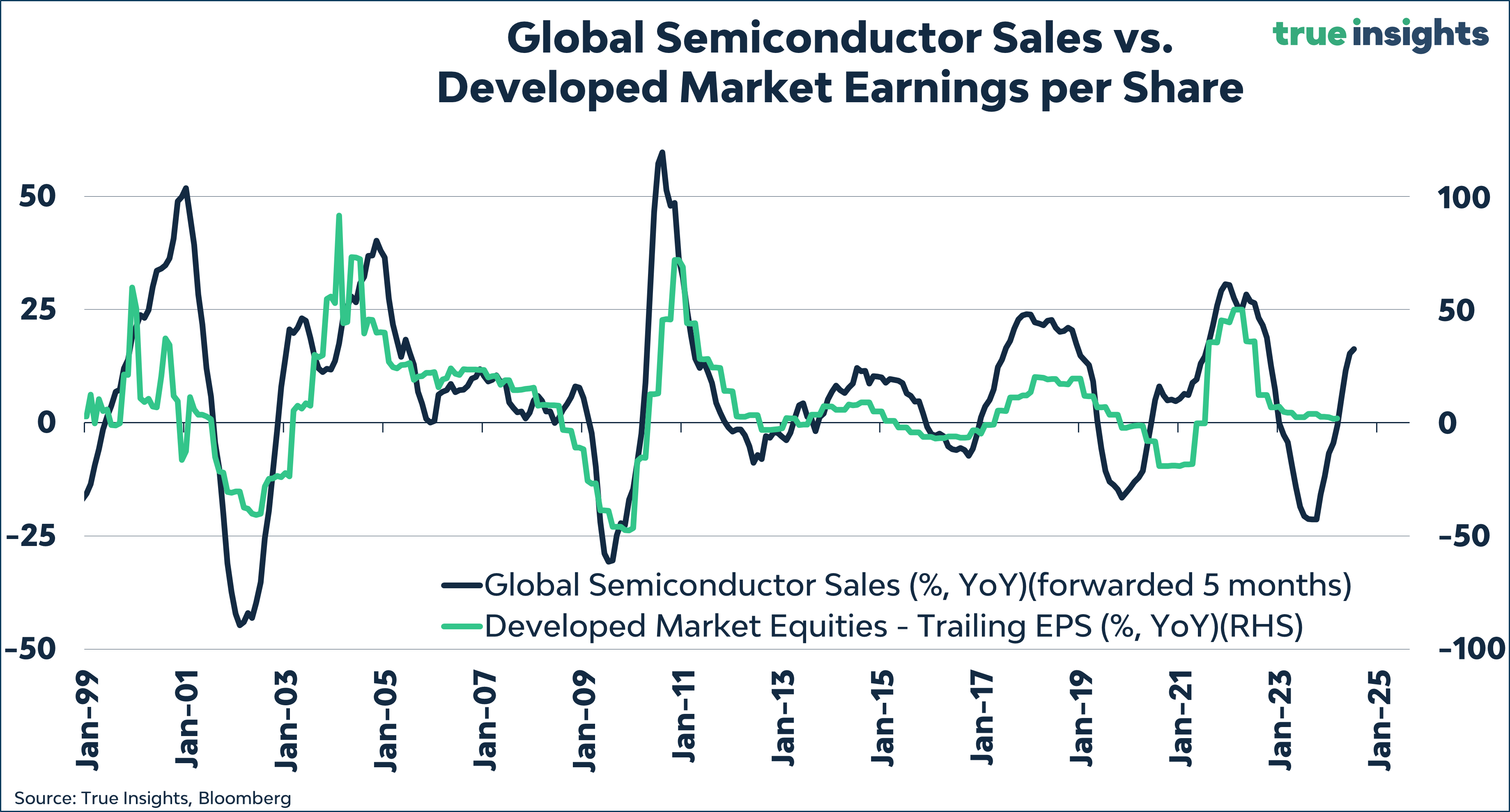

Global Semiconductor Sales

Semiconductor sales have surged by 16% compared to last year, signaling an earnings growth of over 30%!

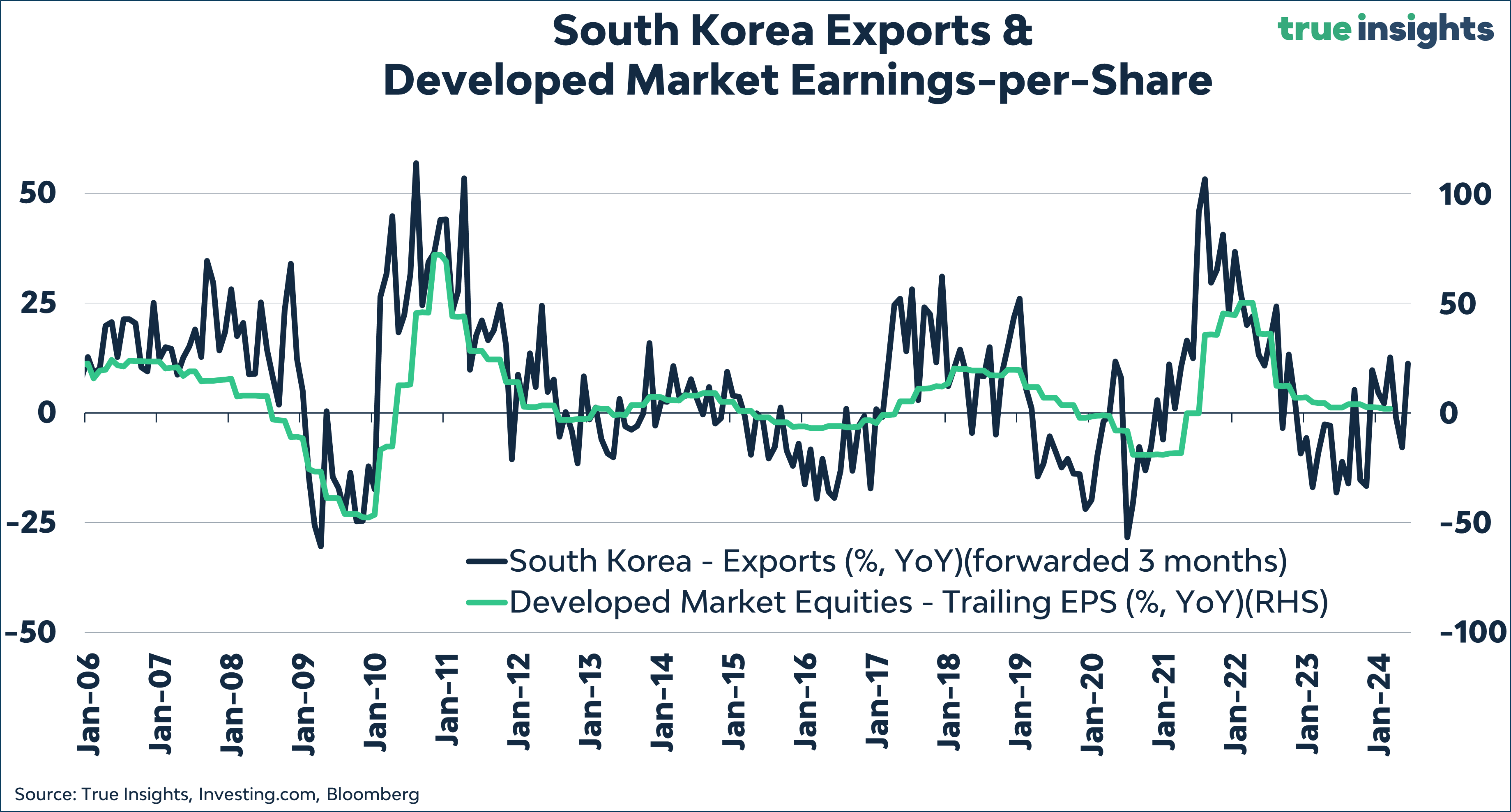

South Korean Exports

As the chart demonstrates, the trajectory of this earnings indicator tends to be more volatile than the previous two. Nonetheless, the trend appears upward, and based on the latest figures, the MSCI World Index’s earnings per share should increase by about 12%.

Chinese Producer Prices

It’s no surprise that the China-based indicator looks less promising. The Chinese economy has been under pressure for about two years due to the ongoing real estate crisis. Hence, there is a local impact on producer prices, especially since the issues are concentrated in a capital—and resource-intensive sector. According to this earnings bellwether, earnings would need to decrease by 20%.

9% Growth

The interesting aspect of these four bellwether earnings indicators is that they all hold up in a simple regression with the MSCI World Index’s earnings-per-share as the dependent variable. This is also why I aggregate them into an overarching global earnings bellwether.

From the above chart, earnings are expected to be about 9% higher in a few months than they were a year ago. Hence, an earnings recession seems quite unlikely.

Connecting the Dots

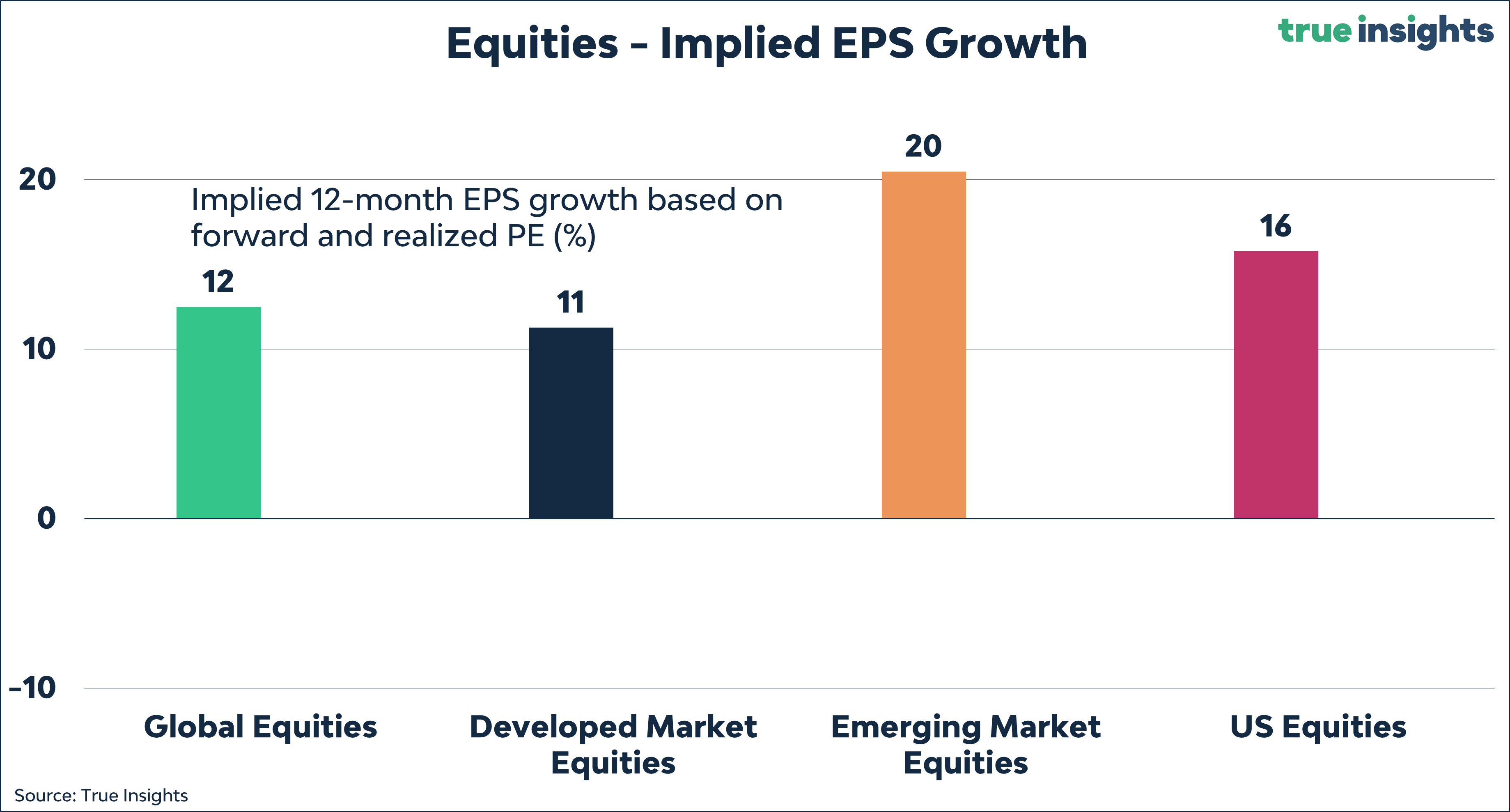

Merely having a (good) estimate of earnings growth is only half the story. Mainstream and social media are flooding investors with reports on the excessive valuation of stocks. And that a sharp correction after a rally of more than 20% is inevitable.

But in reality, expectations are far from stretched. Investors are expecting 11% earnings growth for the MSCI World Index. Although this pertains to a rolling window of 12 months, a bit of calculation reveals that this is in no way exuberant. If earnings have risen 9% year-on-year by July – like the bellwether earnings indicator suggests – only an additional 2.9% earnings growth is needed in the remaining eight months to reach 11% EPS growth twelve months from now. 2.9% in eight months is hardly exaggerated.

In emerging markets and the US, the expected earnings growth is higher. This includes large tech companies in the US that have regained their earnings superiority. For emerging markets, that 20% comes from a particularly low base. Compared to a year ago, earnings are now 14% lower.

In other words, earnings development does not hinder further rises in the stock markets.