Is the yuan ripe for devaluation?

Is the yuan ripe for devaluation?

Many await a Chinese currency depreciation, but with foreign investment and capital markets collapsing, things are complicated.

China finds itself caught in a vortex between Scylla and Charybdis. It is stuck in an endless real estate recession while investment in the country dwindles. Additionally, Federal Reserve Chairman Powell has made life harder for Chinese policymakers. Should devaluation of the Chinese currency occur, it would be wise to buckle up beyond China’s borders as well.

Lower interest rates:

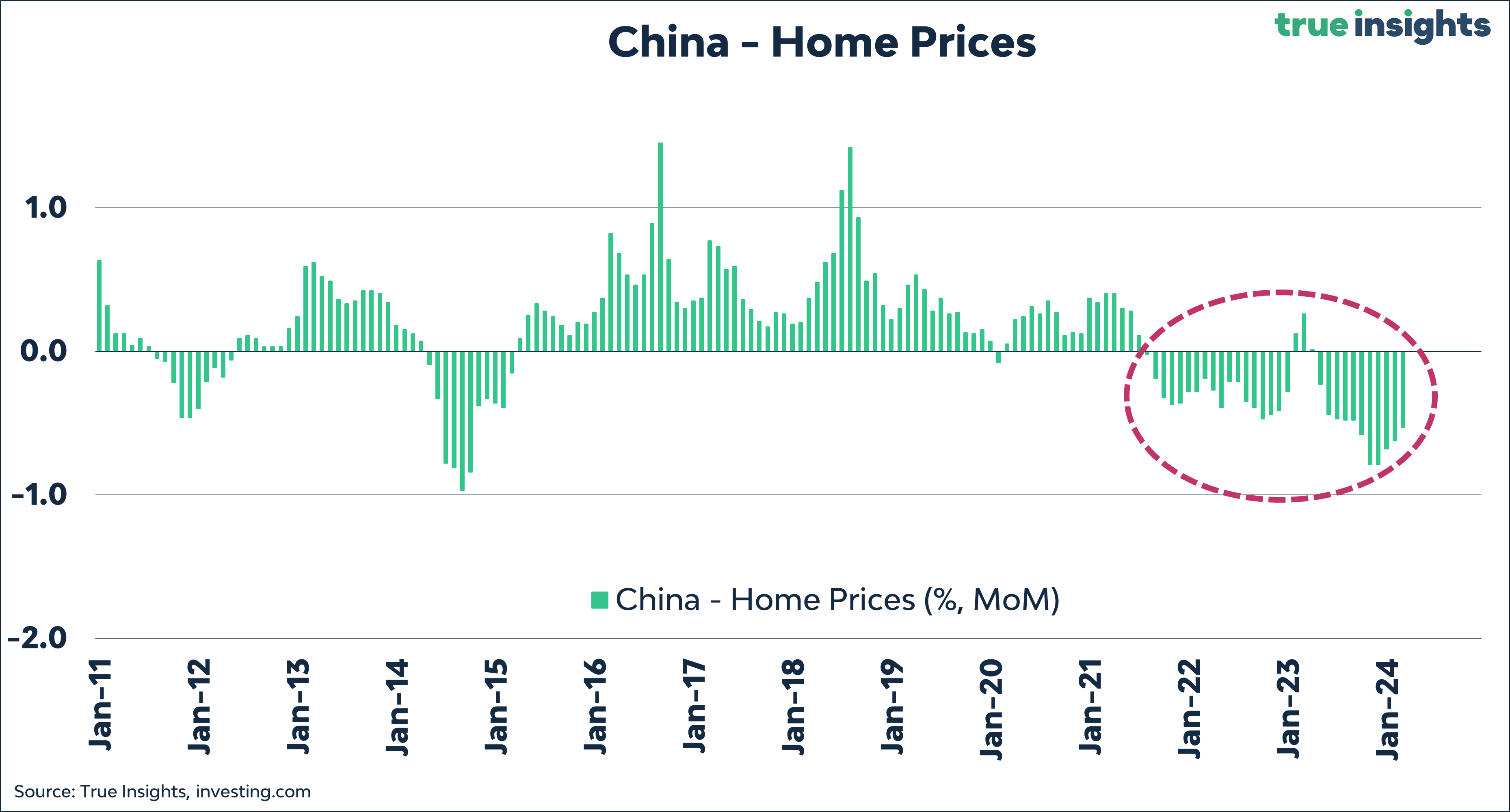

Chinese housing prices have fallen in 29 of the last 32 months, which is substantial, to say the least. The Chinese real estate recession is causing numerous issues. Chinese prosperity is declining since real estate was the prime investment choice of Chinese households. As a result, the Chinese have turned to buying gold. In addition, the gold-buying of the Chinese central bank may actually be a sign of things to come.

Local Government Financing Vehicles (LGFVs), burdened with hefty debts, no longer sell land for construction, losing their main source of income. And real estate developers are teetering on the brink of collapse. Fortunately, there is always the same panacea that numbs all (debt-related) troubles: lower interest rates. And that is exactly what nearly every economist is anticipating. However, the Chinese central bank decided not to cut interest rates the other day.

Issues:

Why not? Because there are numerous reasons to expect that even lower interest rates (the 10-year rate in China is at 2.25%) will cause even greater problems. First, these lower rates lead to further debt accumulation, kicking real estate and LGFV issues down the road. However, after Moody’s, Fitch recently reprimanded China for excessive and rapid debt accumulation by lowering the outlook for Chinese debt. Second, lower interest rates put additional pressure on the Chinese currency, which Chinese policymakers can ill afford, especially as interest in investing in ‘the Middle Kingdom’ has significantly declined. Foreign Direct Investment shows only one trend: downward.

Powell Pivot:

Moreover, the pressure on the Chinese currency has already intensified due to significant US inflation setbacks, which have forced the Federal Reserve to put their plans to quickly lower interest rates on ice.

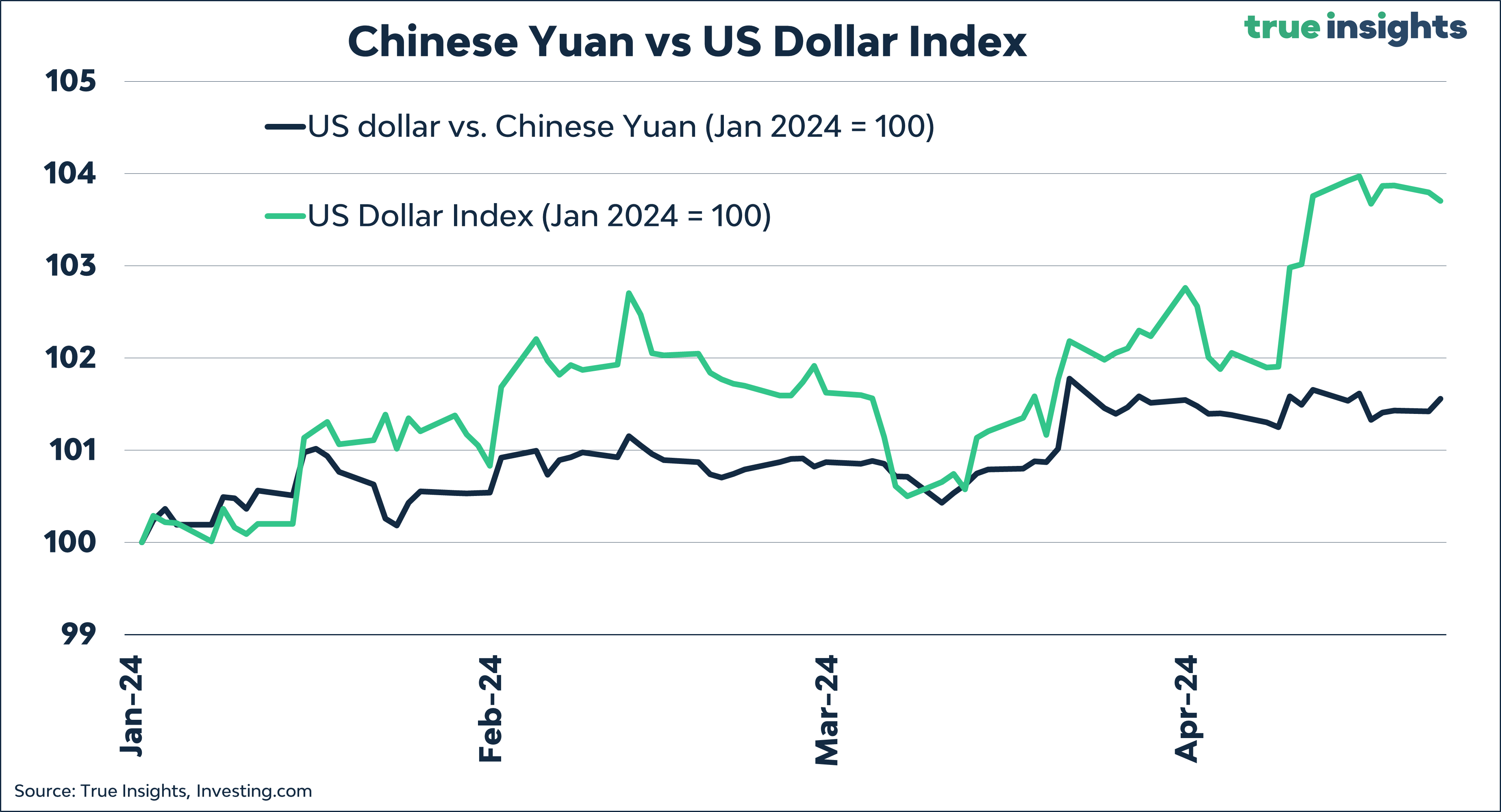

The figure below illustrates the development of the US Dollar Index compared to the US dollar versus the CNY. While the Powell pivot caused the dollar to soar, its appreciation relative to the Chinese yuan remains suspiciously limited.

Fasten your seatbelts:

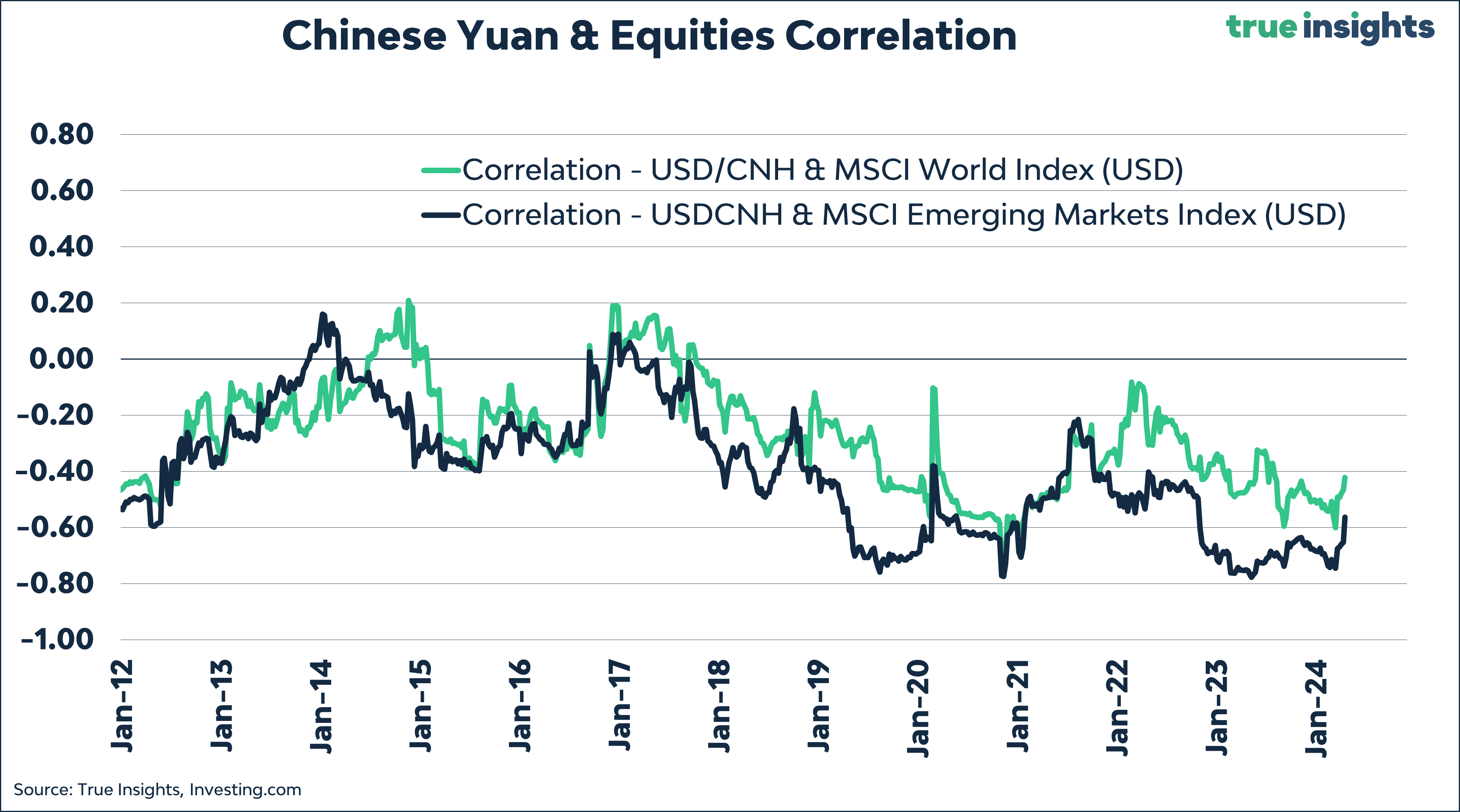

Regarding the anticipation of a devaluation of the Chinese currency: ‘be careful what you wish for.’ A devaluation would shock many economies in the region that have their currencies directly or indirectly pegged to the yuan. It would also create a jolt in the relative competitive positions of China, Japan, and South Korea. Commodities would become significantly more expensive, further pressing on Chinese growth. Thus, such devaluation would cause a ripple effect felt worldwide.

While many make these claims without foundation, I want to point out the chart below. It shows the negative correlation between the dollar/CNY exchange rate and the MSCI World and Emerging Markets Index. A weakening of the Chinese currency typically coincides with lower stock prices.

And China? It must choose between a quicker recovery in the real estate sector and domestic economy or preserving its attractiveness as an international investment destination. That’s a tough call to make.