Japan removes negative interest rate policy – The end of an era and long yen?

Japan removes negative interest rate policy – The end of an era and long yen?

Zooming out quickly reveals that Japan has not entered a new monetary policy regime. Yet, neither does the Federal Reserve.

To cut to the chase, my answers to the questions in the title are ‘no’ and ‘no.’ Let me nuance this a little. Technically, one could argue that it marks the end of an era. After a mind-boggling eight-year period, negative interest rate policies by central banks have finally ceased.

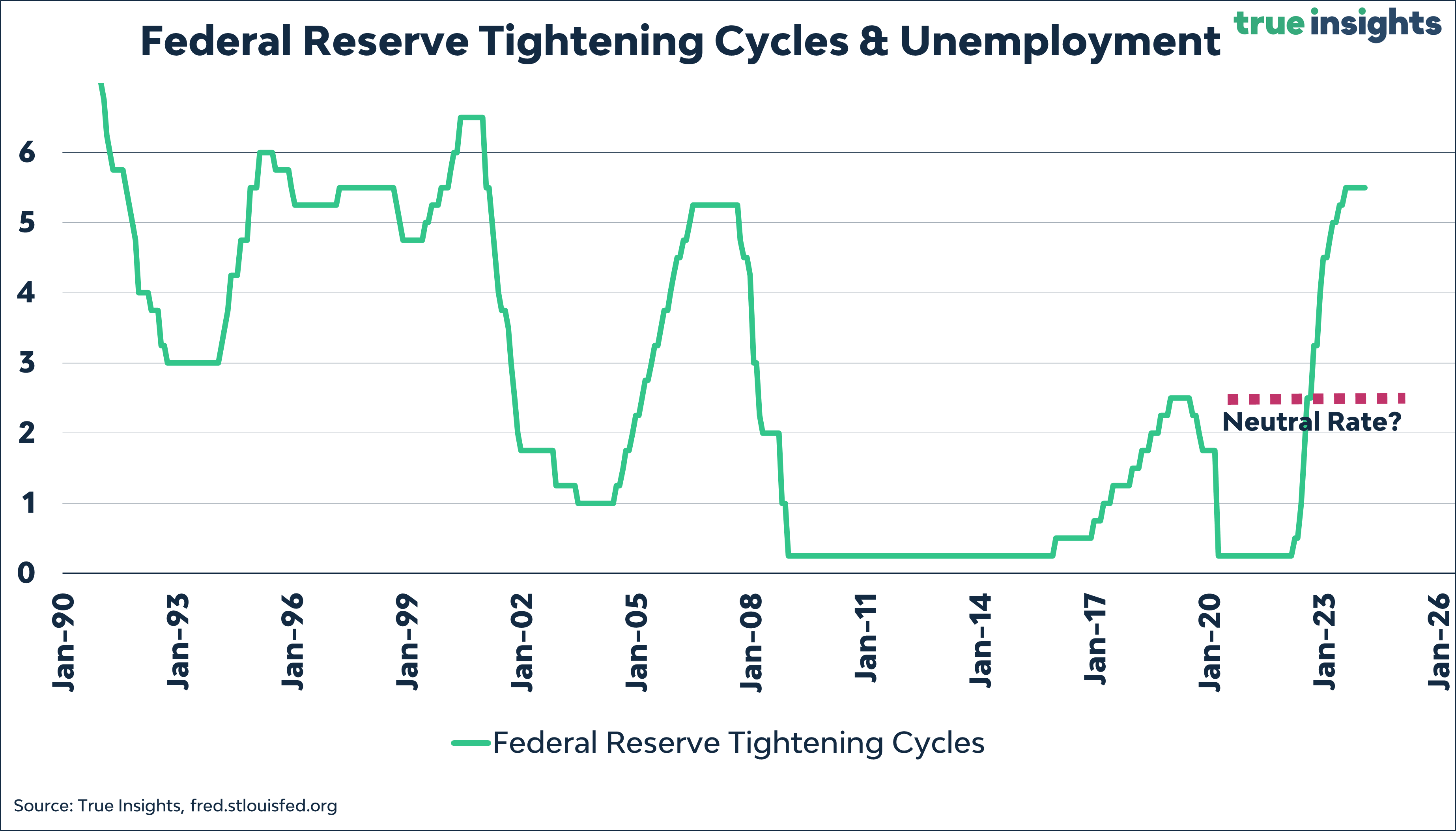

But zooming out, the conclusion is not justifiable that we are entering a different central bank regime, especially from the perspective of the Bank of Japan. The graph below from Trading Economics (the red arrow and text are mine) clearly illustrates Japan’s 25-year stint in the same regime: ultra-low policy rates, with the recent addition of negative rates.

A series of rate hikes?

Bank of Japan Governor Ueda provided little guidance on potential further rate hikes. All Ueda divulged was that the terminal rate would depend on the neutral rate.

But what exactly is that neutral rate? Well, I suspect zero percent, which is precisely where the policy rate stands now. The graph below depicts Japan’s potential GDP growth, as estimated by Bloomberg. Draw a line through it, and potential GDP growth will likely dip below zero sometime this decade.

Lowflation

And inflation? Due to the absence of economic growth, it’s impossible for the Bank of Japan to achieve its 2% inflation target over an extended period. Again, zooming out helps. How does a country with potential growth two percentage points higher than Japan, the United States, have a similar inflation target? Who decided that 1) inflation is a good thing and 2) exactly 2% inflation is the holy grail for every major economy?

If we look back over the past 25 years, average inflation in Japan equals 0.3%. That’s practically zero. Incidentally, the 2014 inflation spike is almost entirely attributed to a VAT increase, not underlying inflationary pressure.

Quantitative Tightening

I’ll let the chart do the talking here. The Bank of Japan holds nearly half of all outstanding Japanese government debt. Ueda during the Bank of Japan press conference: ‘No specific idea on what to do with balance sheet now.’ I rest my case!

That debt chart again

Finally, one of my favorite debt charts. Japan has by far the largest debt pile of all major economies. And that simply means interest rates MUST remain low. Below is my signature chart showing the relationship between total debt-to-GDP on the x-axis and the 10-year yield on the y-axis. Paradoxically, the dovish rate hike by the Bank of Japan has led to increased significance, as the 10-year rate fell after the decision.

Trading the yen?

Even though negative interest rates are now officially gone, the Bank of Japan remains an outlier in monetary policy. So, there’s no reason to go long the yen now, especially with the Fed’s rate decision still pending.

As the above graph shows, yen traders have been wrongfooted again. Going long on the yen has been an overwhelming pain trade in recent years.

Naturally, this raises the question of whether you should short the yen instead. Had the Bank of Japan done nothing, I would have said yes. But what’s happening on the other side of the Pacific also matters. And while the official Fed statement must sound somewhat hawkish after the latest inflation figures, I expect Powell to strike a dovish tone whenever possible.

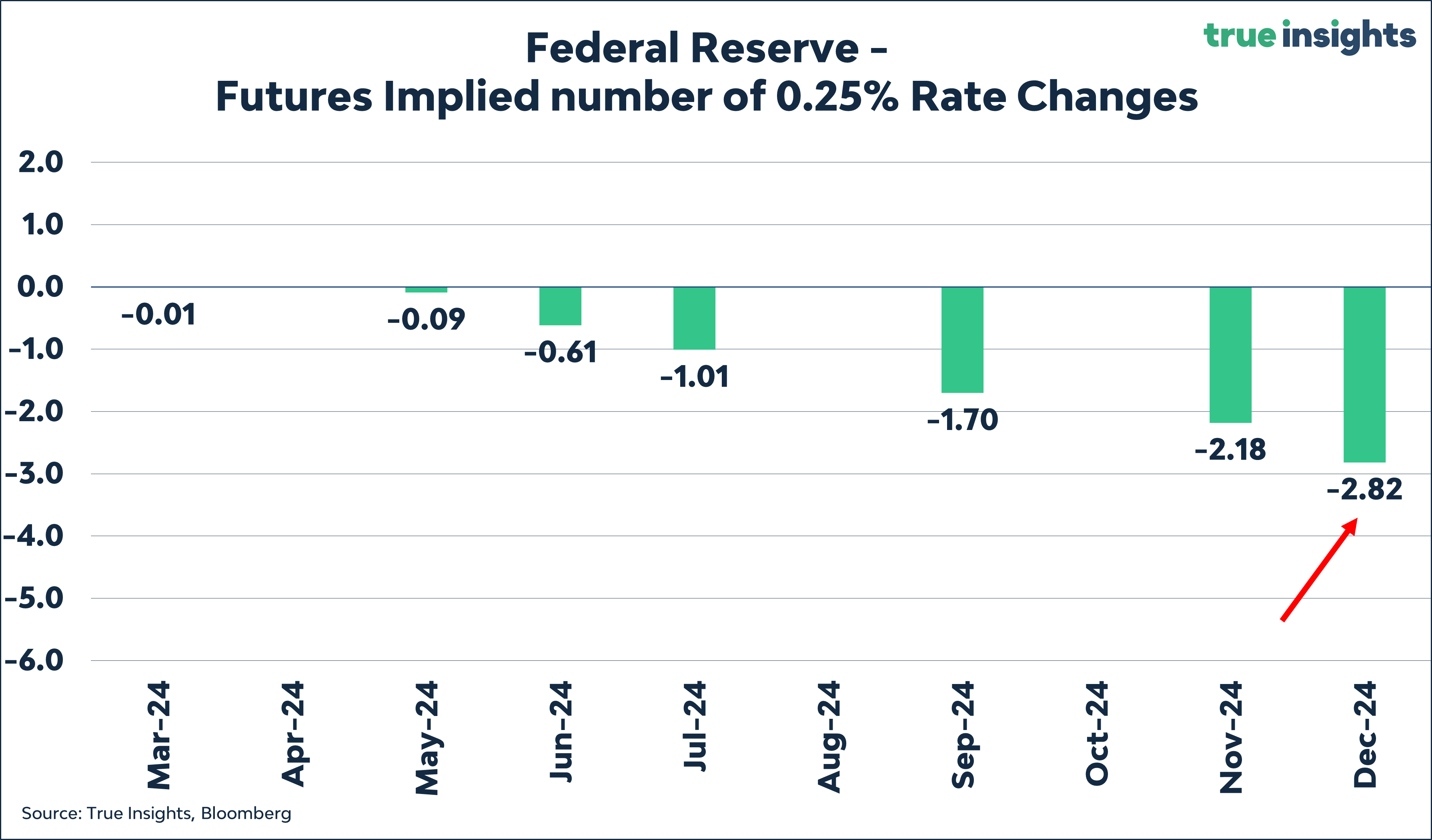

Markets are expecting only 2.8 rate cuts this year. The Fed had previously anticipated three, but there’s a decent chance the median forecast in the Dot Plot will likely inch up.

However, Powell has repeatedly indicated that rates are unusually restrictive. And that the gap to the neutral rate, which neither strangles nor stimulates the economy, is large. The equilibrium rate is assumed to be around 2.5%, but I believe it’s even lower. The distance from the current 5.25% to the neutral rate is huge and gives the Fed ample room to cut rates. The Fed will relent once American consumers start spending less or once the labor market further weakens. Going short yen isn’t the most obvious position in such a scenario. I’d lean towards further scaling up gold, for example.