March FOMC meeting conclusion: Powell likes his balance sheet ‘BIG!

March FOMC meeting conclusion: Powell likes his balance sheet ‘BIG!

Even though the new Federal Reserve 'Dot Plot' looks marginally hawkish, Powell's strong emphasis on ample liquidity made markets cheer!

What the Fed communicated:

The Federal Reserve kept the Federal Funds Rate unchanged as expected, between 5.25% and 5.50%. The crucial takeaway is that the interest rate remains highly restrictive. Assuming a neutral rate of 2.50% – which, in my view, is too high – the rate would need to drop by about three percentage points to avoid choking the economy. While this may not happen immediately, it underscores the magnitude of room the Fed has to lower rates while still claiming they are restrictive in light of lingering inflation risks.

In the new dot plot, the median expectation for 2024 from FOMC members remained unchanged. In other words, three rate cuts are anticipated. This leans somewhat dovish, as some Fed watchers had anticipated a slight upward shift following disappointing CPI and PPI figures.

Expectations for the Fed Funds Rate in 2025 and 2026 did increase by a quarter point. However, attaching too much significance to this is cautioned against. Predicting monetary policy more than a year ahead is particularly challenging, even for the FOMC members. Interestingly, the median forecast for 2026 still surpasses the long-term projection, indicating persistent inflation risks and the absence of any economic setbacks, which seems somewhat optimistic.

The Federal Reserve remains very keen on lowering rates to accommodate a soft landing, or perhaps no landing at all. This sentiment is evident in the official statement: “The committee judges that the risks to achieving its employment and inflation goals are moving into better balance.”

Forecasts: The Fed raised its GDP forecasts for all years from 2024 to 2026. Core PCE for 2024 increased by 0.2% to 2.6% but remained unchanged for 2025 and 2026. The Fed will likely consider anything below three percent sufficient grounds for substantial rate cuts.

A caveat to the previous point: although the 2024 expectation for Core PCE increased by ‘only’ 0.2%, the vast majority of FOMC members shifted to the right in the graph below.

What Powell said:

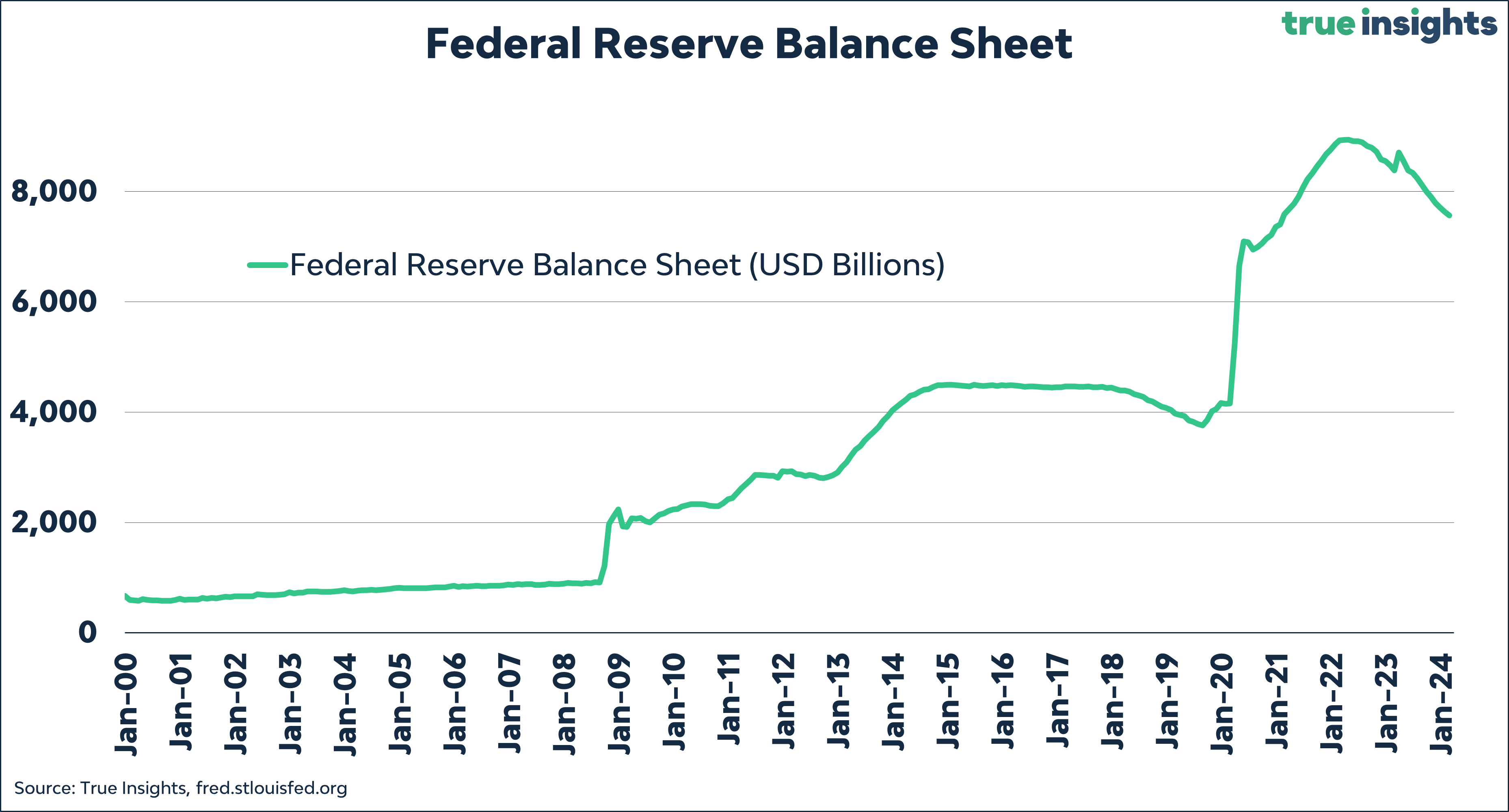

Many questions came in on the balance sheet, with Powell stating that no additional decision on the size had been made. Slowing down the reduction of the balance sheet is imminent, though. Powell is wary of facing a short-reserves situation again and aims to transition from abundant liquidity to ample liquidity.

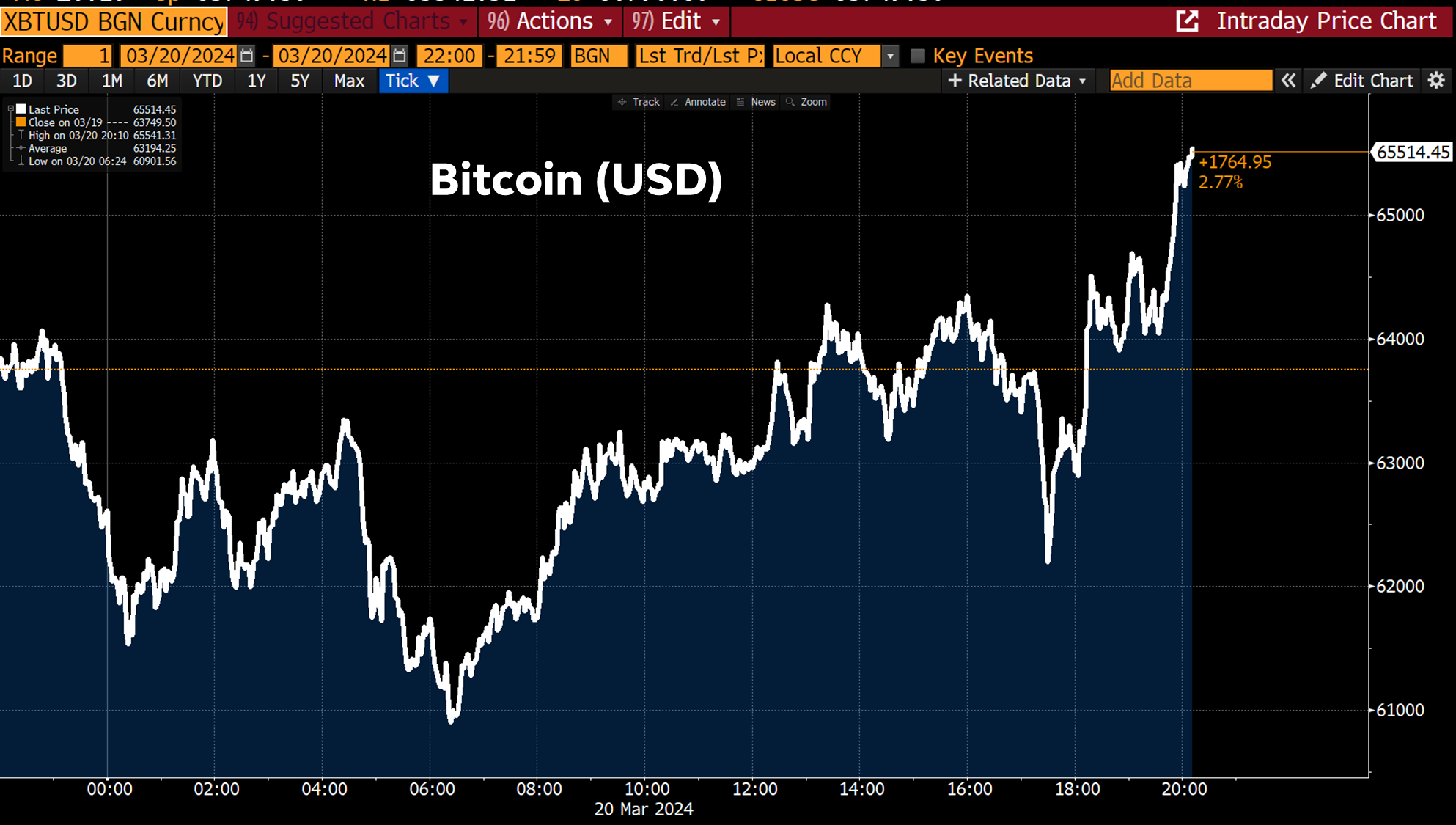

This is music to the ears of stocks, gold, and Bitcoin!

While I truly believe that Powell believes a slowing of balance sheet compression does not imply a higher terminal level, the likelihood of that exactly that outcome is quite high. The Fed increasingly requires flexibility and liquidity to achieve its goals, and Powell made abundantly clear he likes his balance sheet ‘big.’

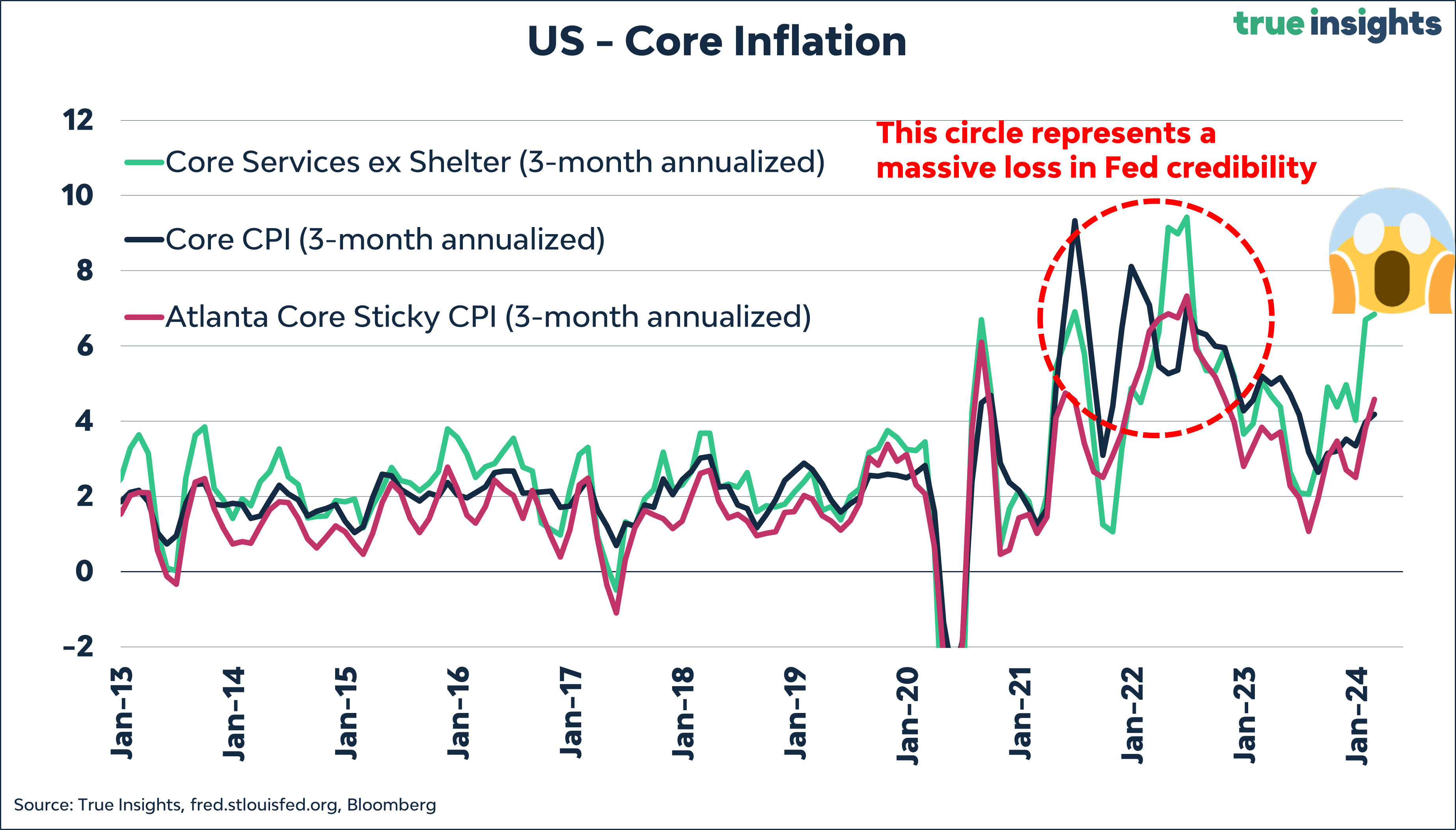

Powell provided nuance to recent high inflation numbers several times. January’s figures were primarily due to seasonal effects, and a Core PCE of less than 0.3% month-on-month isn’t terribly high in Powell’s view.

Powell sought to reassure that inflation is coming under control. The necessary confidence that inflation will gradually move towards 2% hasn’t increased, but Powell emphasized current developments likely confirm the anticipated ‘bumpy ride.’

On the increase of the median dots for 2025 and 2026, Powell doesn’t believe interest rates will return to zero quickly, thus shifting the whole Fed funds curve upward slightly. I have two considerations: Powell admitted that the uncertainty around this assumption is high. Second, higher inflation should be factored in, making real bond returns unattractive.

Even if hiring remains strong and the labor market robust, that’s not a reason to refrain from rate cuts.

We are a long, long way from a Central Bank Digital Currency.

What to make of this:

What can we glean from this? Not all that much. The Fed divulged little and kept things open, predominantly riven by recent inflation figures. Powell also indicated that no decisions were made on any future meetings.

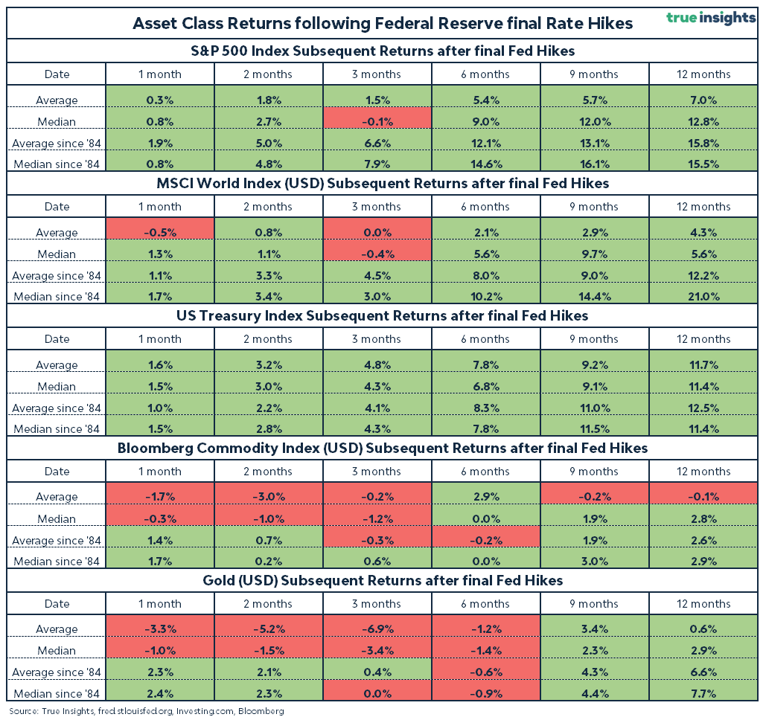

A bit of history

Historically, the end of a major tightening cycle is good news for stocks and Treasuries, particularly in the initial months after the final hike. The opposite is true for gold and commodities. We are now eight months past the last rate hike, and from a historical perspective, it’s no surprise that most things look ‘green.’ HOWEVER, notably, equity markets have surged much faster than the historical average.

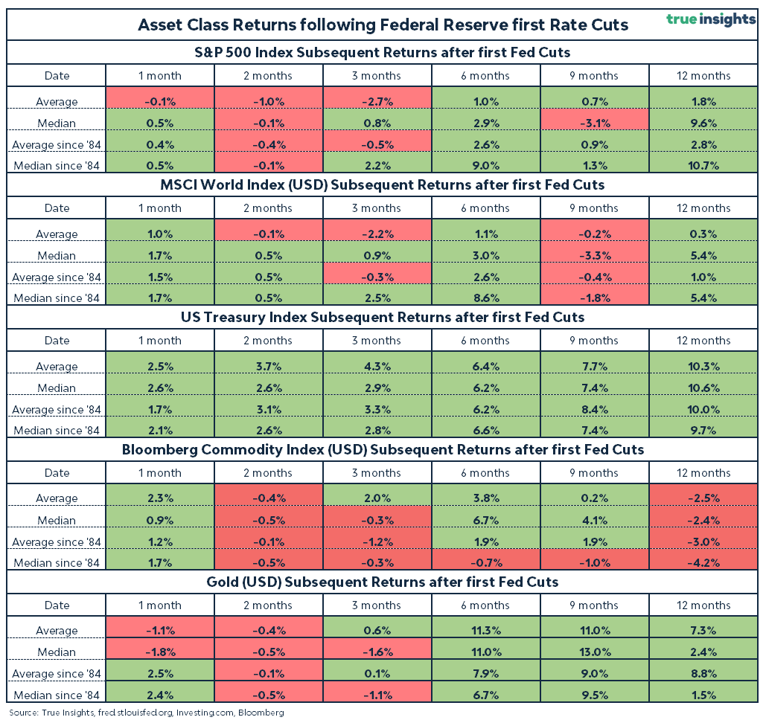

Historically, the onset of rate cuts is less favorable for stocks, especially in the first few months following the initial cut. However, the picture is less negative than often portrayed in the media. Given the tone of the statement and Powell’s presser, stay with equities until the fat lady sings.

Gold struggles initially when rate cuts occur, but then skyrockets after a few months. You want to hold on to your overweight position in gold, especially since Powell expressed his love for an elevated balance sheet. Finally, somewhere during the rate-cutting cycle, Treasuries will have another small window to shine.