Powell so wants to cut rates!

Powell so wants to cut rates!

Despite the sign the Fed had to take from the last three CPI report, Powell squeezed in a dovish tone to a hawkish message.

Important notice

True Insights is coming to an end, at least in the form of paid subscriptions. As many of you may know, I launched my investment fund earlier this year, the Blokland Smart Multi-Asset Fund. I must now choose to focus on the fund, the investments, and the overall strategy.

As of this message dated May 1, 2024, I will continue to write for True Insights for one more month until May 31, 2024. We will handle the discontinuation and any necessary refunds accordingly.

More information here.

Fed Statement

The official Fed statement contains two key elements. The first comes as no surprise:

“In recent months, there has been a lack of further progress toward the Committee’s 2 percent inflation objective.”

Thus,

“The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.”

However, to coat the forced hawkish statement with a dovish flavor:

“The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion.”

Following the previous FOMC, I wrote that the Fed likes its balance sheet BIG.

The Press Conference

Obviously, Powell’s focus was mainly on inflation, but he did not go beyond the expected remarks that there has been a lack of progress, which has not given the Fed more confidence.

What Powell was willing to share is that it’s appropriate to ‘take signal’ after three disappointing CPI reports. But of course, we already knew this.

Moreover, Powell was extremely clear regarding the likelihood of further rate hikes: unlikely. Although some market pundits predicted more rate hikes, they will not happen. The Fed is acutely aware that things start to break at a 5% interest rate.

The Fed must answer how long rates must remain restrictive to conquer inflation. Powell stated that it is taking longer for the Fed to gain the necessary confidence.

Furthermore, Powell managed to slip a sentence among all the inflation-related remarks in his introduction that reflects the intentions of the Fed. The Fed stands ready to act if an unexpected labor weakening occurs. Even though the progress on inflation is disappointing, Powell indicated that the Fed can now pay attention to both elements of its mandate. As I will show below, the US labor market is indeed weakening.

The takeaway

The Fed is definitely not going to raise rates again. It views the disappointing inflation figures as a signal that it needs to wait. However, as soon as the door opens even a slight crack, likely due to a weaker labor market, rates will go down. I continue to expect several rate cuts this year.

The Turn

Was Powell dovish enough to reverse the turn? I would certainly not rule it out.

But what caused the market turn? The chart below, in my opinion, is the best summary of the turn in macro sentiment. GDP growth fell to 1.6% annualized in the first quarter of this year. This starkly contrasts the previous two quarters, which saw growth rates of 4.9% and 3.4%, respectively.

And that’s just one of the two lines. After a period of deliberate deviations, the Core PCE deflator is now back as the Federal Reserve’s preferred measure of inflation, and it jumped to 3.7% in Q1. That’s almost double the previous two quarters and also higher than expected. This rate is also not particularly close to the Fed’s target.

Adding these two lines together results in what could be the beginning of stagflation: low growth with high inflation, the most daunting scenario for a central bank to be in. This also explains why markets have been so pressured.

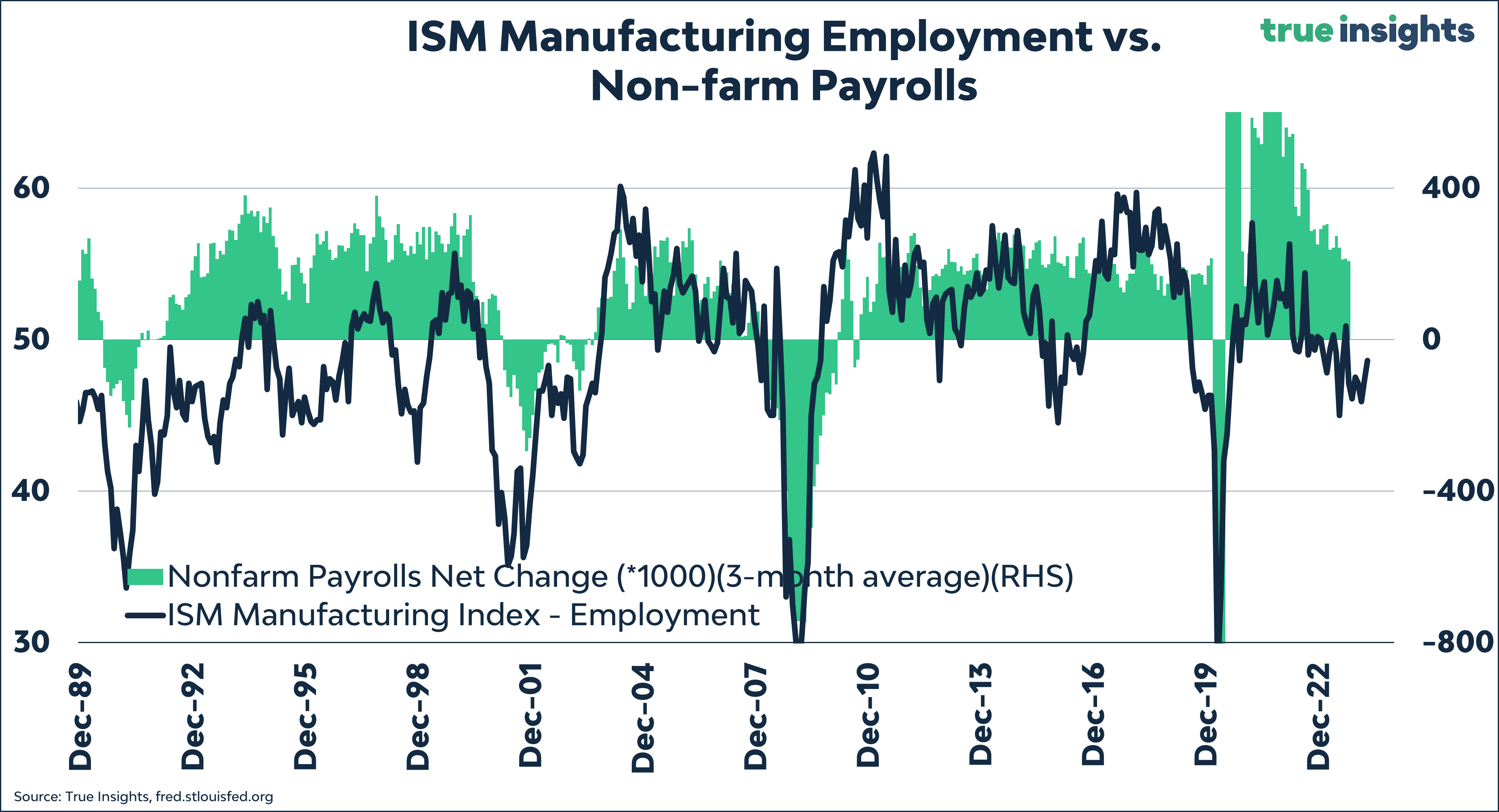

On Wednesday, we received even more stagflation-like data. After the first reading above 50 in 17 months, the ISM Manufacturing Index fell back below that level. The index also came in lower than expected. Meanwhile, the ISM Manufacturing Employment Index remained below the 50 mark for the seventh consecutive month. And job openings fell more sharply than expected.

Against the backdrop of mediocre growth-related figures stood yet another disappointing inflation figure. The ISM Prices Paid Index shot up in April to above 60. It’s almost two years since that was last the case.

In short, declining growth with rising price momentum. Everything a central bank does not want. And with the highest inflation figures in more than 40 years still fresh in memory, the Federal Reserve is being pushed into a corner it does not want to be in. Incidentally, Powell sees neither the stag nor the flation.

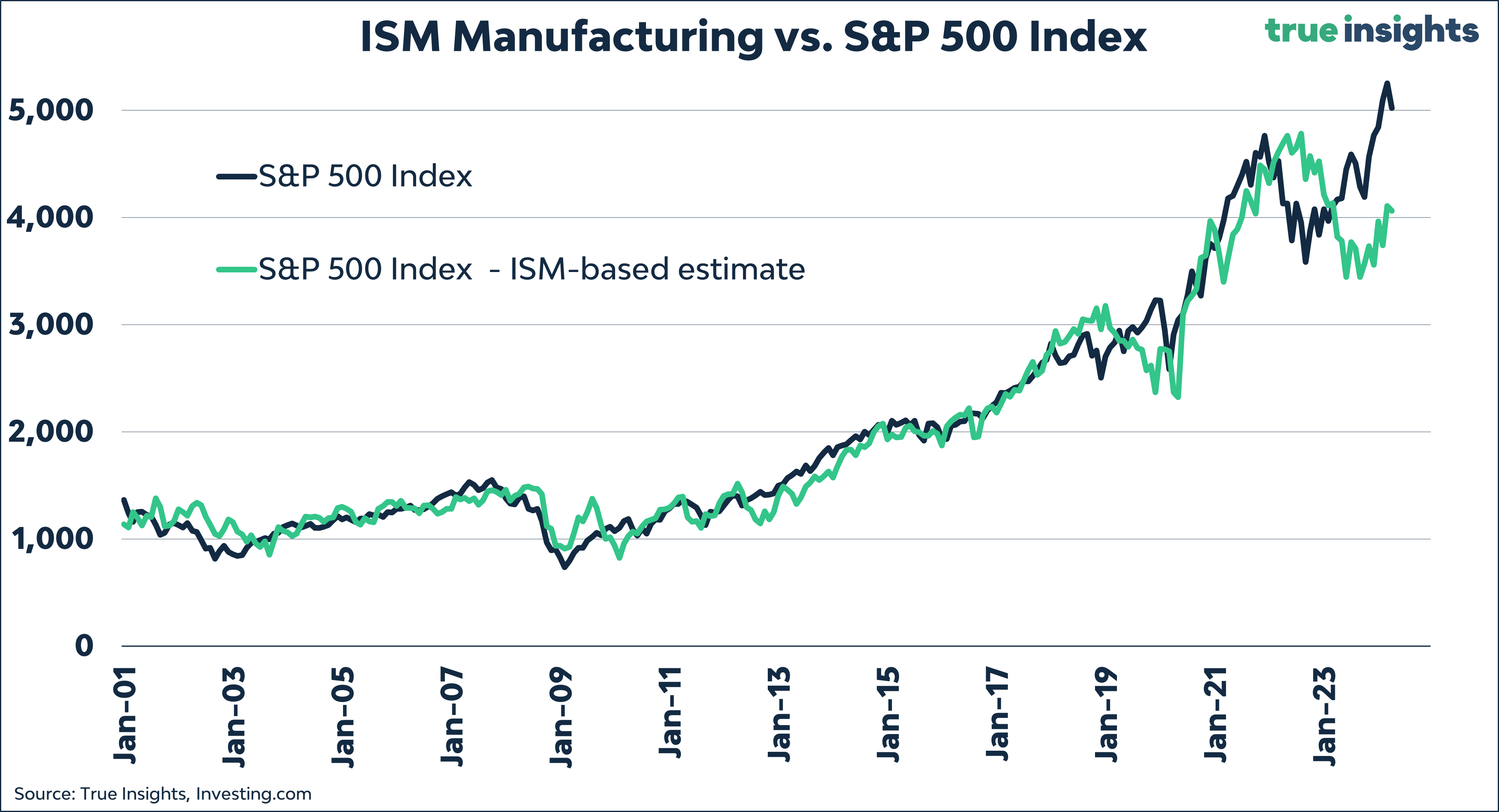

Finally, although the gap has narrowed slightly due to a mini-correction in stocks, the gap with the S&P 500 Index model value based on the ISM Manufacturing Index and the actual index stands at a tidy 1000 points or about 20%.