Running out of Runway

Running out of Runway

The odds that Powell can pull off another dovish act at the next FOMC press conference have dropped significantly following the March inflation report.

During the last couple of FOMC press conferences, Fed Chairman Powell fully embraced his role as a central bank dove. Despite disappointing inflation figures, “Jay” maintained expectations of three rate cuts this year. However, after the March CPI data, it’s highly doubtful that Powell can repeat his dovish act on May 1st at the next press conference.

US headline inflation rose to 3.5% in March, exceeding expectations. Core inflation remained at 3.8%, against expectations of a slight decline to 3.7%.

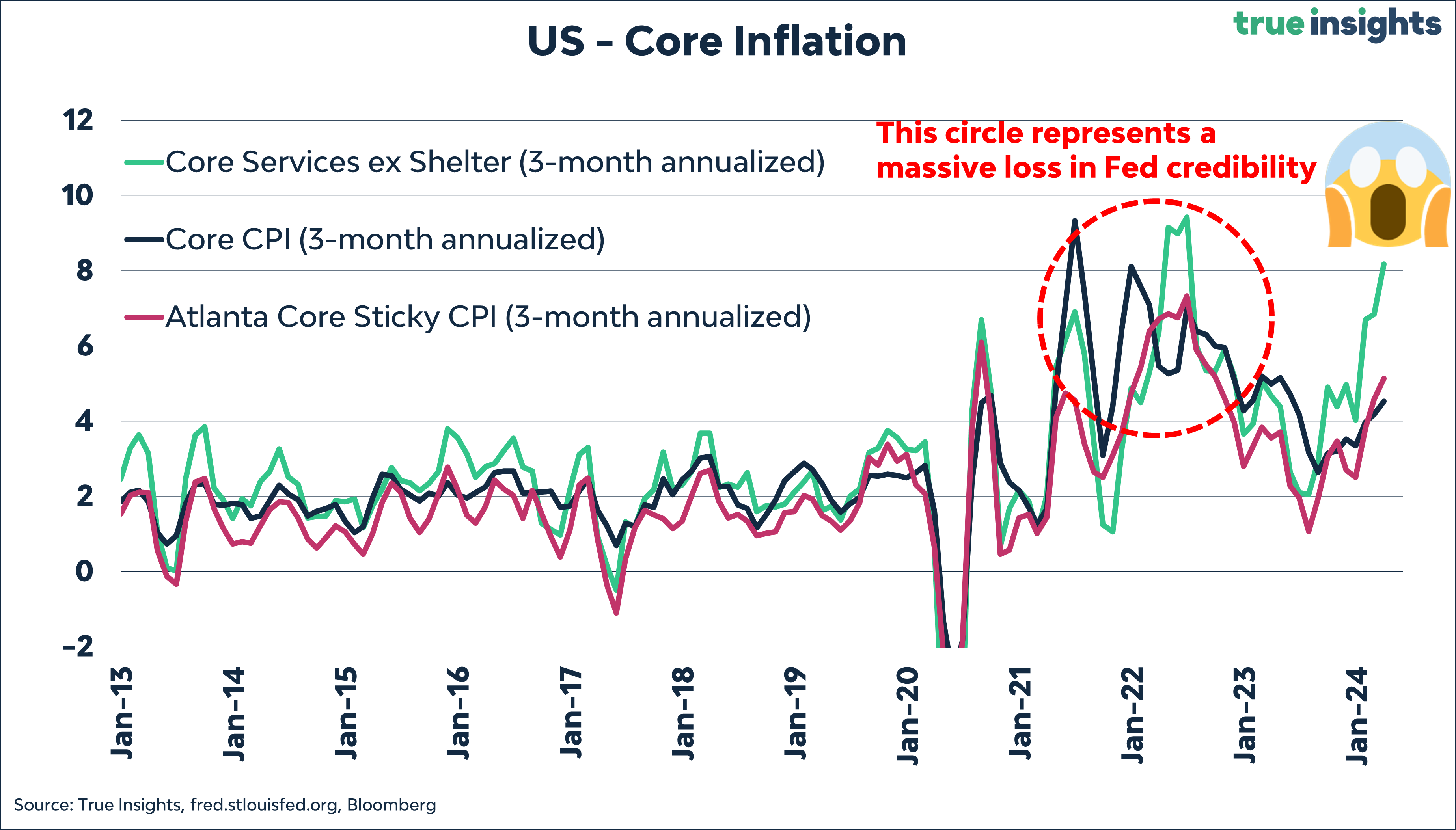

But forget these numbers quickly; what’s really important is the chart below. The so-called SuperCore inflation, the Services CPI excluding Shelter, rose by a startling 8.2% on a 3-month annualized basis. Yes, you read that right, over 8%. Now, we rarely hear Powell talk about this small part of the total inflation basket, especially not the 3-month annualized figure, but it seems particularly challenging not to mention it at all on May 1st. The heavy focus on the Services CPI excluding Shelter during 2022 ultimately convinced stock markets that the Fed would continue raising rates longer, resulting in falling stock prices.

The result of the March CPI figures:

2-year US Treasury yield back at 5%, the highest level since November

10-year US Treasury yield at 4.56%, the highest level since November

US Dollar Index > 105, the highest level since November

Markets are now pricing in just 1.6 rate cuts for this year

How many rate cuts?

So, how many rate cuts are we looking at now? I’m sticking to three steps of 0.25% or more. Why?

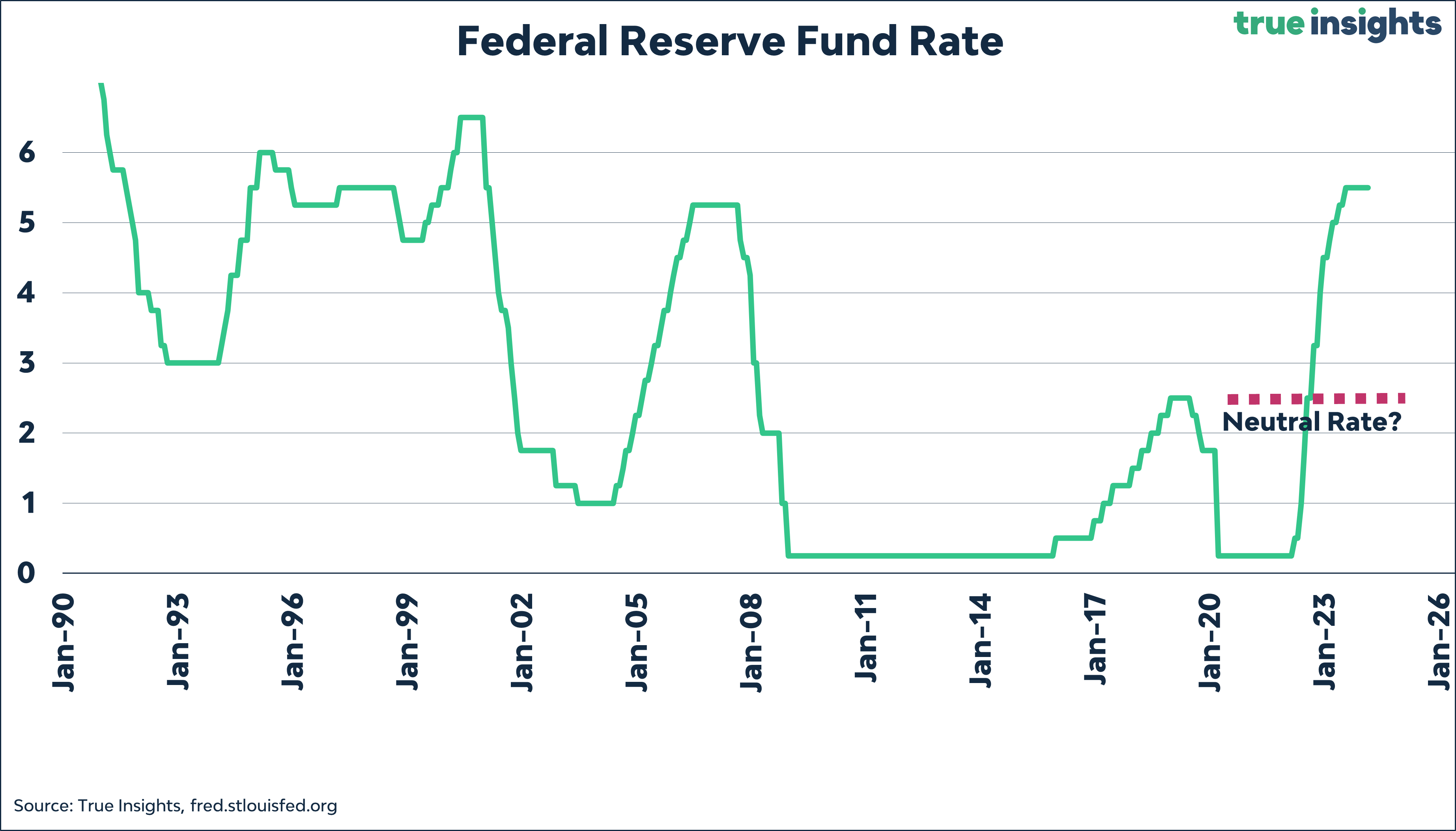

Even though economists are now talking up the neutral rate after years of revising it down, I assume that with each significant rise in public or total debt, the neutral rate falls. Excessive fiscal stimulus during times of positive GDP growth masks this.

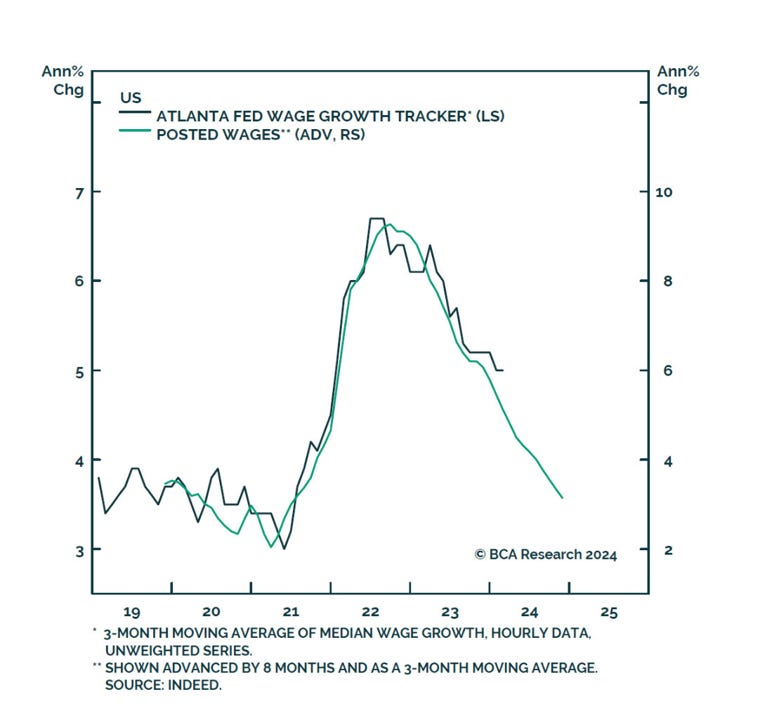

Wage pressures are easing, unlike in 2021-2022.

Excess savings have been depleted, making it unlikely that spending will remain as strong as in the last couple of years. Also, wage growth is moderating.

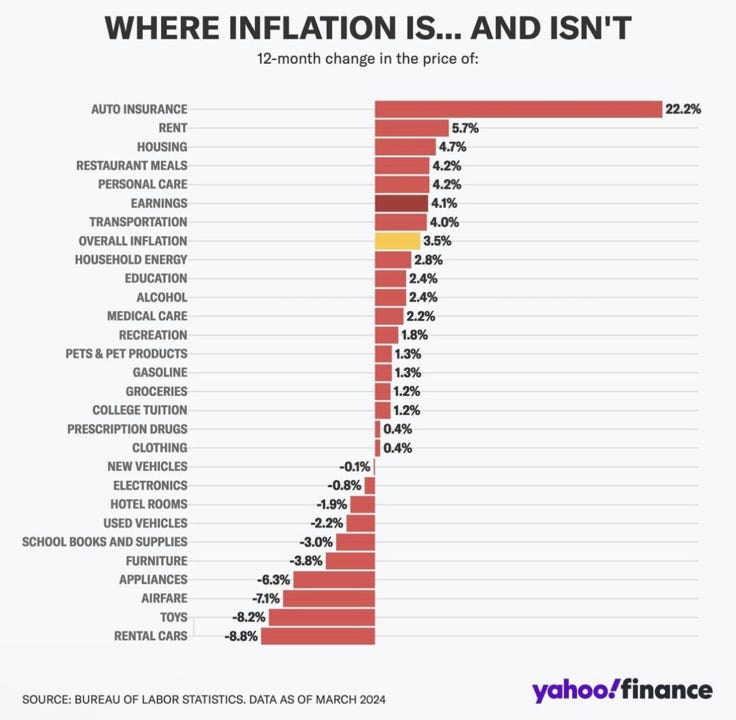

Big-ticket spending items are rising in price the most, which further increases the chances of reduced spending growth.

Not much use to you now

The Federal Reserve can easily cut rates by two times 50 basis points, but the takeaway is that this likely will not happen until later this year. This is an issue with markets having anticipated a relatively quick start to rate cuts.

On the other hand, the outlook for earnings has improved, as described in the previous Insight.

Together, this could result in consolidation before a new direction is chosen.