The 5% Rule!

The 5% Rule!

Things start to break when interest rates hit 5%, mostly because of central bank or political actions. We are back at 5%!

As of this writing, the “mother of all equity indices,” the S&P 500 Index, is down more than 5% from its early April peak. This decline is partly driven by rising tensions in the Middle East, where different factions are exchanging fire without sparking a regional war. Naturally, this is hardly cause for cheer. But there is another significant reason why stock prices are under some pressure: interest rates are approaching 5%, entering what many consider a danger zone.

Oops!

After three disappointing inflation reports, markets have lost hope for three rate cuts. Add to this another round of strong job growth figures, better-than-expected retail sales, and predictions of interest rates soaring above 6% are flying left and right.

In financial markets, one should never rule anything out. Who would have thought nearly four years ago that oil prices would close at nearly negative $38 USD? Certainly not me. But a six percent interest rate inevitably means a recession. We’ve recently seen several instances that more than suggest that at 5%, things start to creak and groan on all sides.

In March last year, the U.S. 2-year Treasury yield rose above 5% for the first time since 2007. The immediate outcome was a regional banking crisis, with only five banks failing. However, they collectively held the largest amount of assets (over USD 500 billion) associated with those failures.

Mistake, thanks!

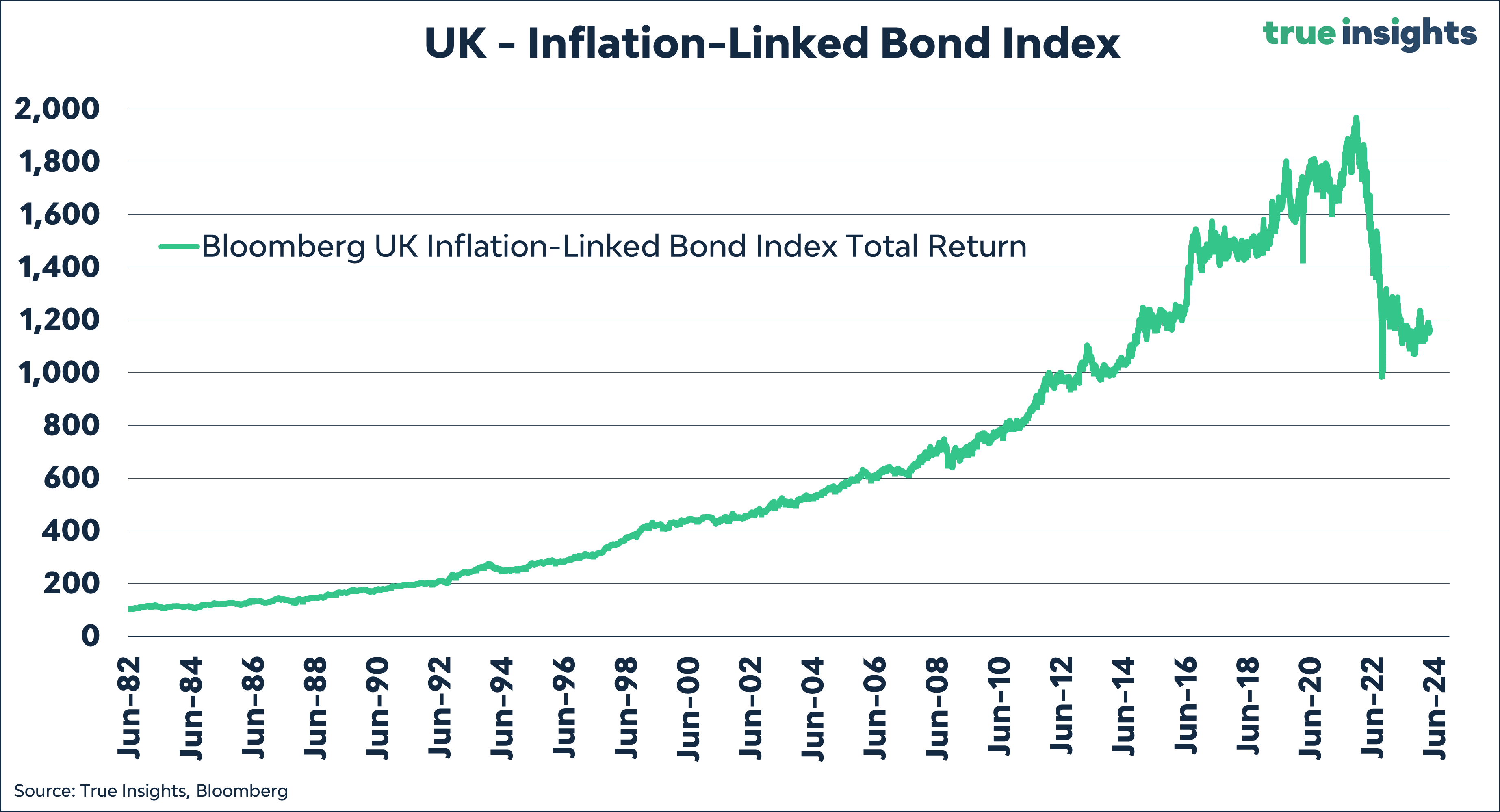

In September 2022, then-Prime Minister Liz Truss and her finance minister introduced the ‘brilliant’ plan

to announce a tax cut (for the wealthy, by the way) without any compensatory cuts elsewhere in the budget. This unfunded tax cut led to a spike in the 2-year UK government bond yield to nearly 5%. Ultimately, the Bank of England had to step in to compensate for the government’s amateurism. With several substantial purchasing programs, as central banks now do when interest rates are too high, the spike in rates was halted. But by then, the British pension and insurance sectors were already struggling to cope with the rapid rise in rates.

And then, of course, there’s Italy, where interest rates have been artificially low for years due to ECB interventions. It’s no coincidence that the Italian 10-year yield rose to 4.98% last October, the highest level since 2012 when Italy narrowly escaped a forced exit from the Eurozone.

Give it time

One factor that might allow economies to eventually handle a 5% interest rate is time. Time gives all parties a chance to adapt to the new circumstances. However, with towering debt ratios, there’s a significant risk that some will falter. A common mistake, in my opinion, is pointing out that, for example, the United States now pays as much interest as a percentage of GDP as it did in the 1990s. While true, less was spent back then on healthcare, social services, and other mandatory government expenditures. Moreover, the behavior of central banks since the Great Financial Crisis suggests they prefer not to wait for the risks of bankruptcies and potential systemic risk. And as often, the solution lies in lower rates.