The Rally in Gold: Clear as Day

The Rally in Gold: Clear as Day

The rally in gold is driven to a large extent by the same, not changing, narrative, and that narrative is getting stronger!

Since the start of March, the price of gold has risen by 17%. While this is exceptional, it also coincided with Fed Governor Waller’s speech stating that he believes the Federal Reserve should buy more T-Bills. This would qualify as debt monetization as the US Treasury has flooded the bond market with short-term debt.

For perspective, the Magnificent 7 stocks, which continue to be the talk of the town, have not moved at all since March 01. While few investors doubt these seven magnificent companies will meet their lofty expectations, critics of the gold rally are tripping over each other to predict its end.

Opposition

Eventually, there will be a (temporary) end to the explosive rise in gold prices. And if you keep predicting it long enough, you’ll eventually be right. Yet, the arguments supporting these predictions are often paper-thin. Recently, the ‘opponents’ have become more vocal.

Let me be clear before I continue: if the holy grail for you as an investor is that an asset class must generate cash flows in order to invest in it, that’s fine. I’m not sure how far you’ll get in the long run when inflation may be closer to 3% instead of 2% and bond yields have collapsed to preserve debt sustainability, but at least it’s consistent. What’s strange is the argument that there’s a different narrative behind every gold price rally. I don’t think this is the case at all.

Obvious

In my view, it’s always the same story, just in more extreme forms. During every crisis, governments come through with ever larger fiscal stimuli that increasingly need to be ‘managed’ by central banks. This process has accelerated since the Great Financial Crisis in 2008/2009. Initially, yields had to decline low to prevent Lehman’s bankruptcy from leading to an implosion of the financial system. Then came Draghi, who had to keep the Eurozone together by maintaining low interest rates through massive bond buying. And since the excessive stimulus round following the outbreak of COVID, central bank balances have had to remain extremely large to push down yields when necessary and extend debt sustainability as long as possible.

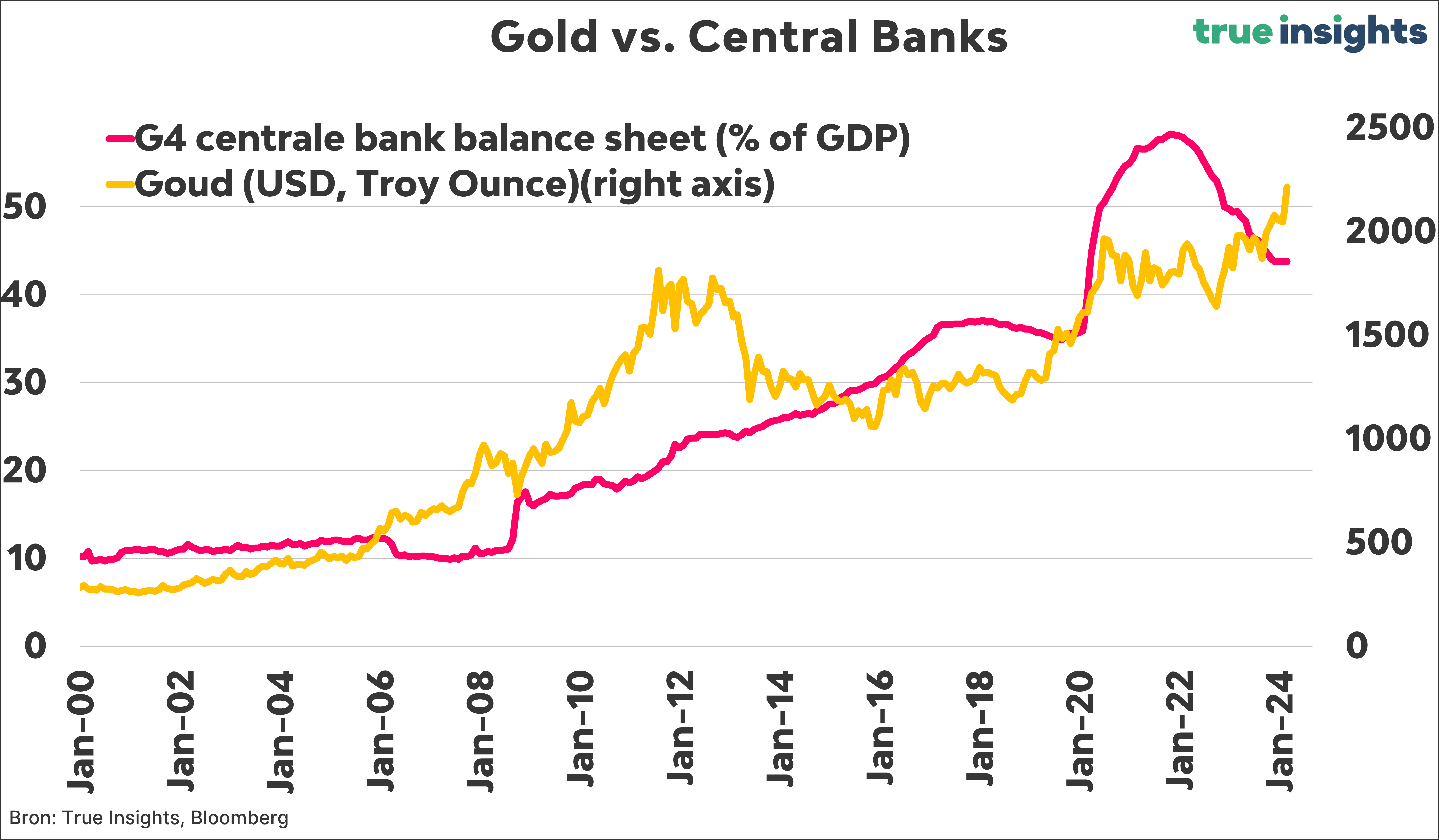

A few simple charts support this idea. Below are the gold price (right axis) and the G4 (Federal Reserve, ECB, Bank of England, and Bank of Japan) central bank balance sheet (left axis). No relationship is perfect, but to deny that there is some correlation here would be naive.

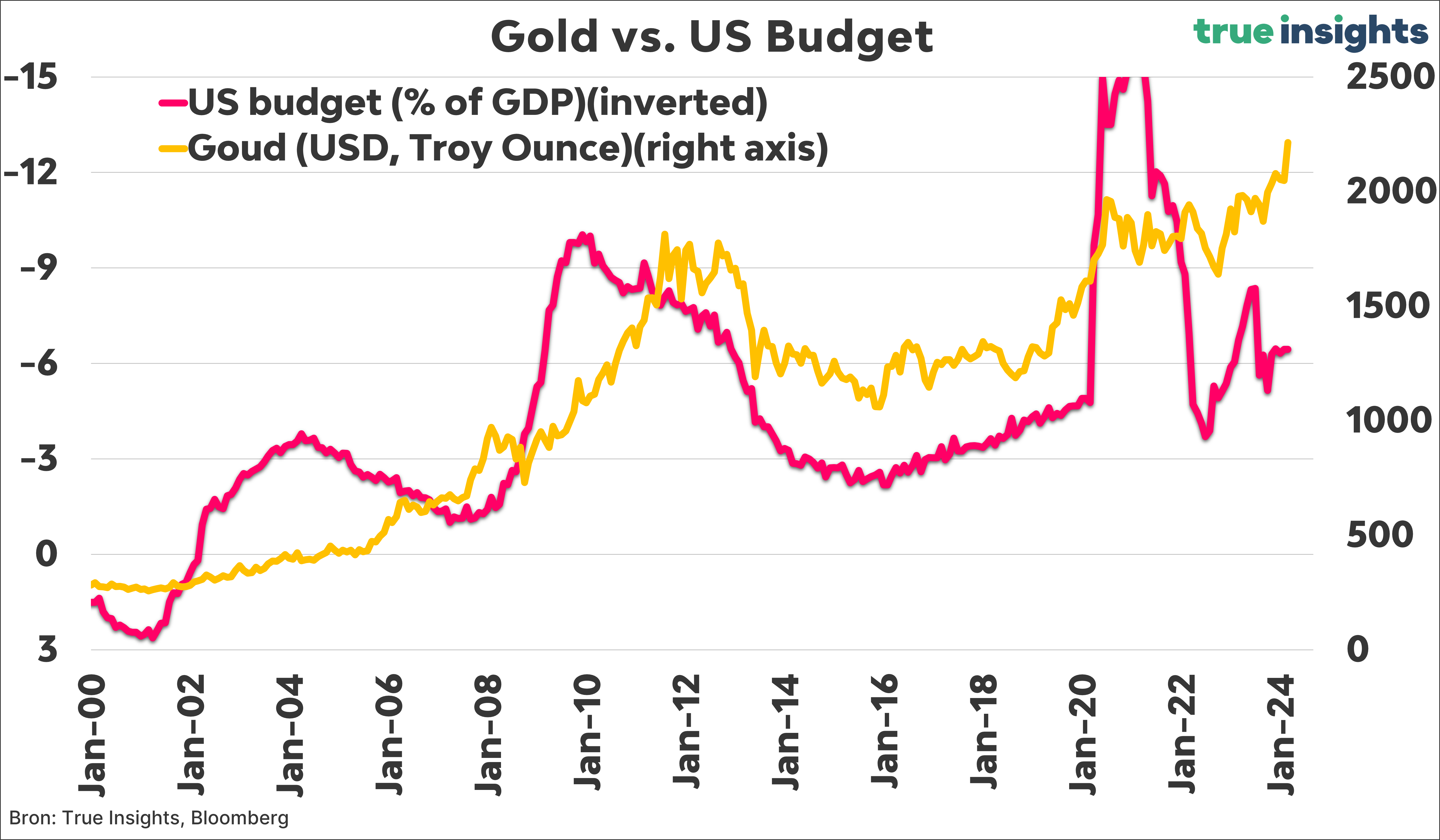

The next chart shows the ever-expanding US budget deficit (left axis inverted) and, again, the gold price on the right axis. Coincidence? I think not.

Expect More

Things go beyond the strong indications of a link between central bank balances, debt, and gold. The Federal Reserve, through Chairman Powell, has already indicated that even though inflation is not where it needs to be, it is (almost) time to scale back Quantitative Tightening. The ECB has the next purchase program, the Transmission Protection Instrument, with even more ‘flexibility’ in place even before the next crisis. In addition, the ECB has indicated that structurally more liquidity, i.e., a larger central bank balance, is necessary to facilitate the changing financial sector.

Does this all not sound like the same overarching narrative to you?