The Weekly Market Monitor – Is that Stagflation? And What is China’s Impossible Choice?

The Weekly Market Monitor – Is that Stagflation? And What is China’s Impossible Choice?

Lower growth and higher inflation are not what markets want to see currently as Fed rate cuts get pushed out further. Meanwhile, China faces a daunting task: What to save?

First Things First – Watch that Stagflation Combo

For quarters on end, the US economy defied gravity. But not in Q1 anymore. In fact, a troublesome combination emerged: lower-than-expected growth paired with higher-than-expected inflation.

The US GDP grew at just 1.6% annualized in the first quarter, significantly less than the expected 2.5%. In contrast, the Core PCE Price Index shot up to 3.7%, against an expected 3.4%, and compared to 2.0% the previous quarter. Although the rise in inflation was not unexpected, the combination of growth and inflation evokes a troubling thought: stagflation.

MACRO

Employment – Still a Way to a Recession

With the latest US GDP figures, the ‘no landing’ proponents can head back to the drawing board. But what about the chances of a recession?

The US Global PMI data disappointed. The Services & Composite PMI unexpectedly fell back to 50.9, while the Manufacturing PMI dropped below 50.

However, the most critical figure was the Composite Employment Index. More companies indicated they had not filled open positions, causing the index to drop to its lowest level since late 2009 if COVID is excluded. The accompanying graph from Shane Oliver of AMP shows the Composite Employment Index in several regions, with the US clearly the outlier.

While one swallow does not make a turn in the labor market, with the ISM Manufacturing and Services Employment indices in March under 50 and US small companies rapidly scaling back their hiring plans, a broader weakening of the labor market may be on the horizon.

From a historical perspective, it would not be strange if unemployment began to rise from now on.

On the other side of the Atlantic, there are signs that the labor market’s exuberance is ending, too. Unemployment in Sweden has steadily risen over the past months, and typically, this is followed by a similar rise in the unemployment rate across the Eurozone.

Which one is it?

The problem with a stagflation-like combination of economic growth and inflation is that the Federal Reserve must choose. Either growth weighs heaviest and convinces the Fed to cut rates or inflation wins, and the Fed is stuck despite declining growth. After a series of disappointing inflation figures and comments from Chairman Powell that the central bank is no longer in a hurry to cut rates, the balance has shifted towards inflation. After the GDP figures, only 1.4 rate cuts for this year are priced in.

A Bit More Budget

Is there no help at all? There is; the US government. The IMF graph below shows that the budget deficit typically comes out 0.3% larger than expected in election years.

For clarity, the US is already heading for another budget deficit of over 6% of GDP.

Hence, the search for even a hint of fiscal discipline continues. Biden has proposed, among other things, that the highest tax rate for capital gains could effectively reach 44.6% (a combination of capital gains tax of 39.6% and income tax effects).

Apart from whether this measure passes, it sounds more substantial than it is. In the 2025 budget, which runs through 2034, a total of USD 289 billion in revenues from the tax reform of capital income is expected. This compares to a current run rate of more than USD 1 trillion in interest expenses annually.

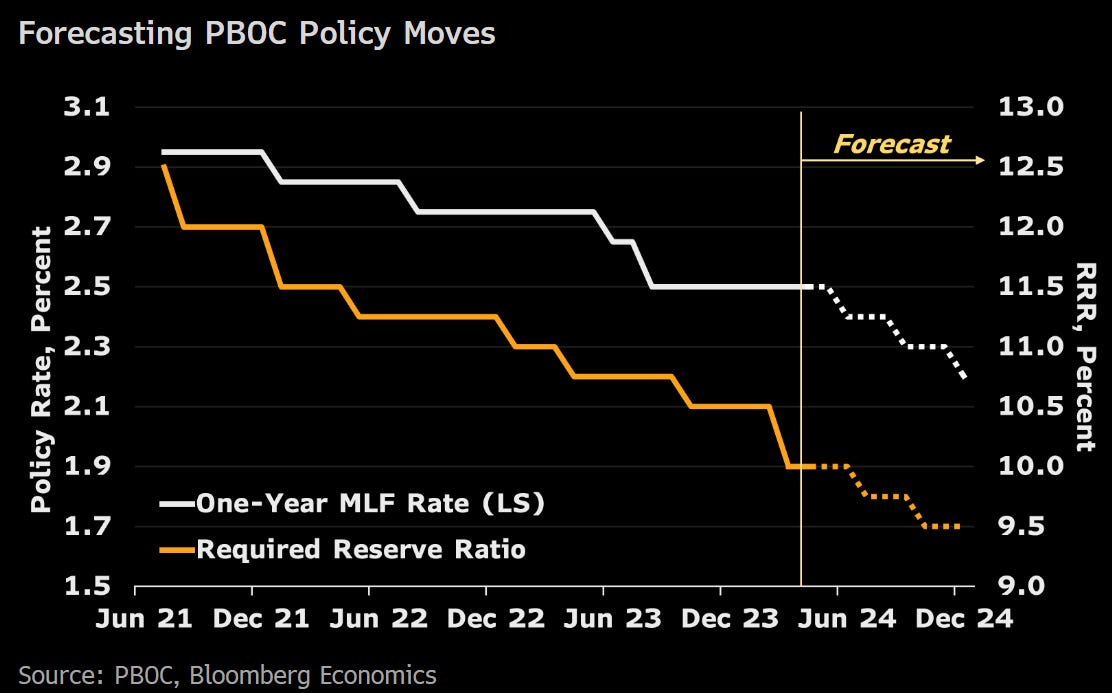

China & Yuan

It is not easy being a Chinese policymaker these days. The economy desperately needs further rate cuts, but the rest of the world does not allow them. This week, the Chinese central bank decided not to cut rates to limit further pressure on the Chinese currency. Meanwhile, South Korea’s and Japan’s competitive position continues to improve noticeably.

Does China prioritize its economy and keep control, or does Powell call the shots and China must wait?

Declining loan growth is one of the symptoms revealing that China is unable to move into full stimulus mode. In addition, even though credit rating agencies have lost some credibility over the years, the downgrades from Moody’s and Fitch are at least indicative of China’s dire debt environment.

The conclusion is that to make life easier for China, it needs the Federal Reserve. When Powell allows room for pricing in rate cuts again, some pressure will be alleviated.

China & Gold

Meanwhile, evidence keeps coming in that China is the driving force behind the recent gold rally. If your main source of wealth, housing, keeps declining in value while your currency depreciates and interest rates are extremely low, you look for alternatives.

Gold trading on the Shanghai Futures Exchange has gone through the roof. While paper and physical trading are two different things, arbitrage ensures efficient price formation. The big question remains: how many of the newly opened gold positions will be closed when the Chinese housing market turns?

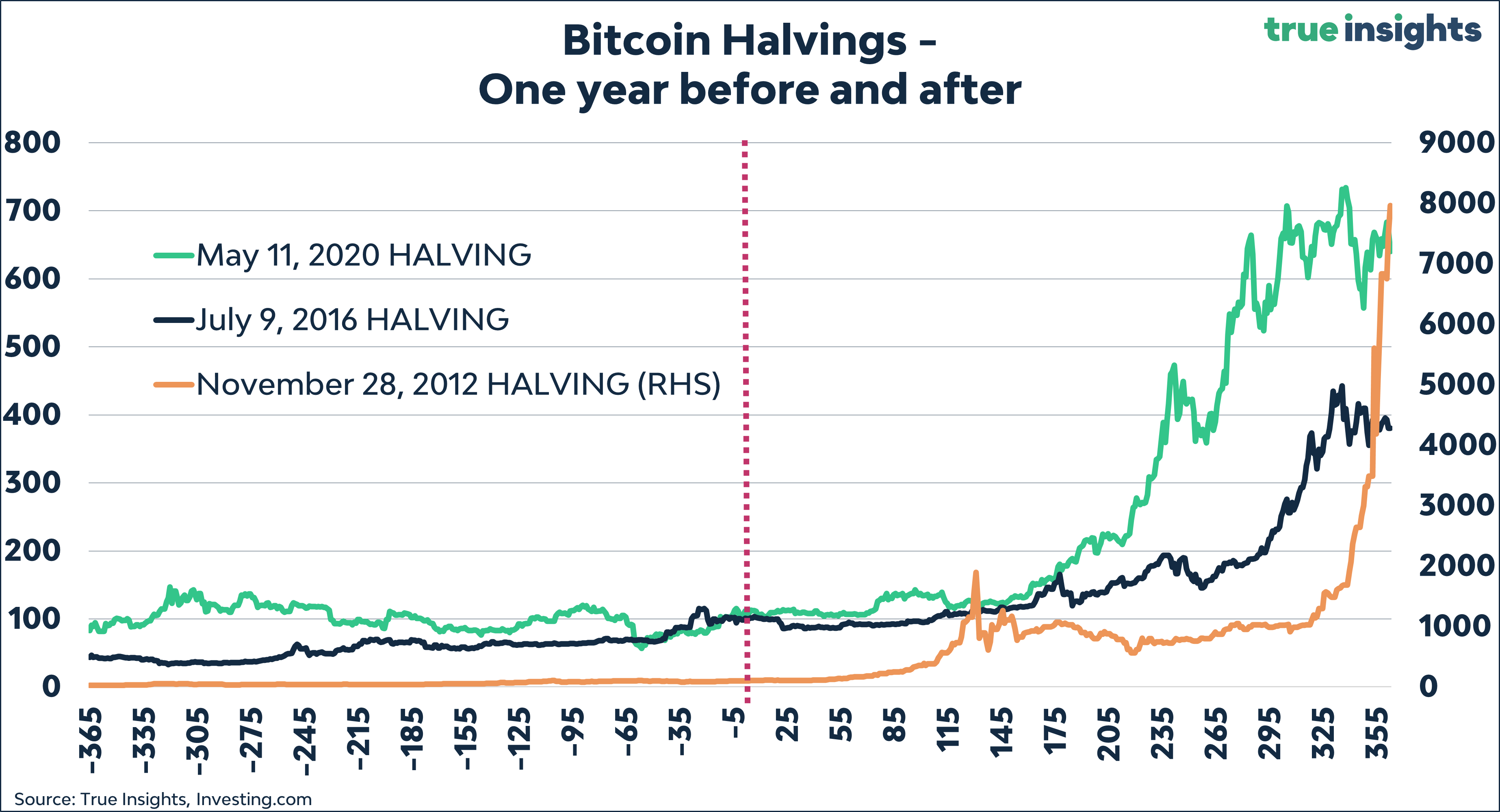

Bitcoin and the Halving

We are past the halving. Where does that leave Bitcoin? I can’t tell. I am often asked this question, but with a sample size of three, there’s not much to conclude. The previous three halvings took a while before the Bitcoin rally took off, but Bitcoin hadn’t made a new high before the halving. This time is, by definition, different.

Bitcoin and Privacy

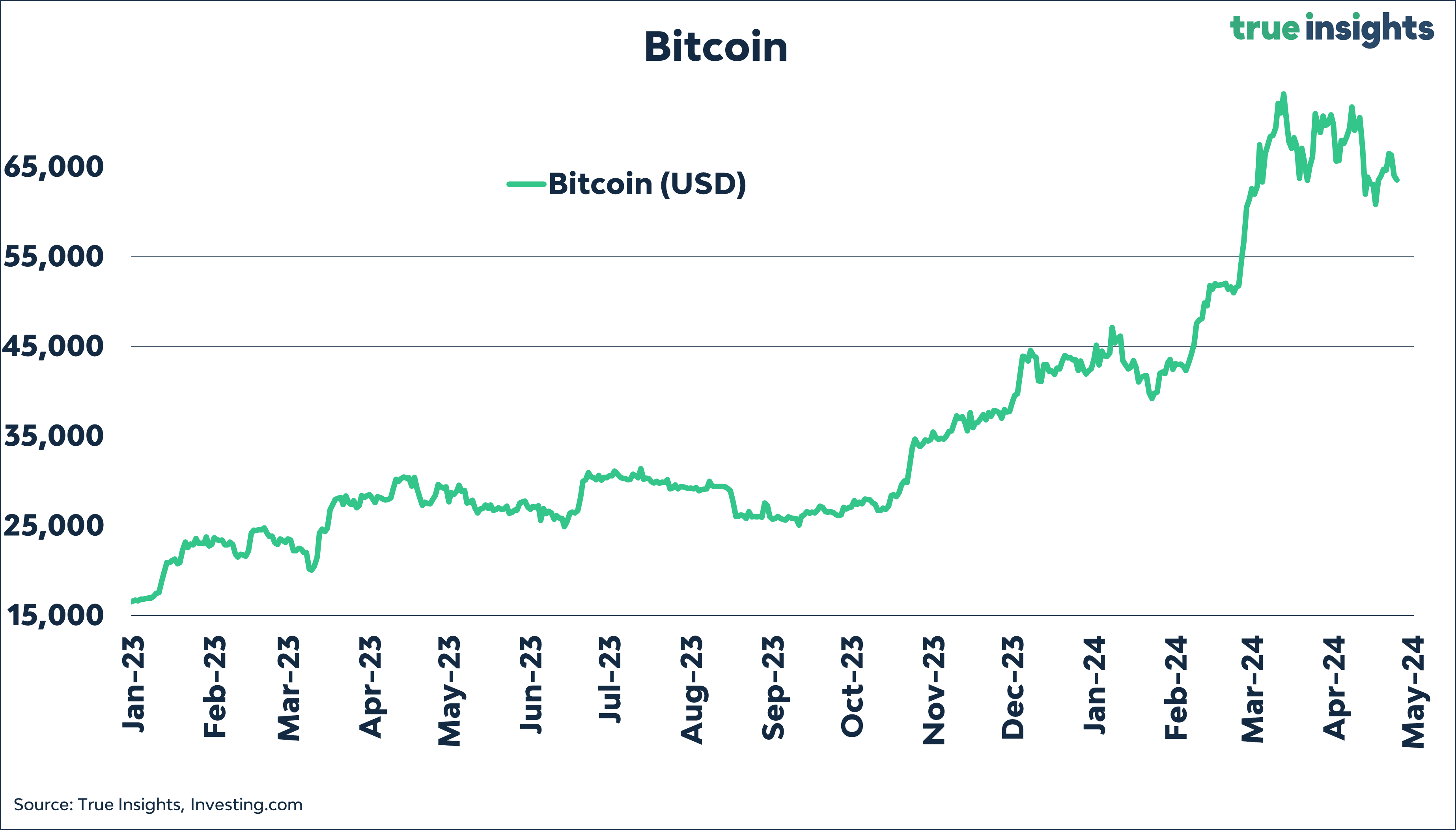

Samourai Wallet, a Bitcoin privacy service, has been shut down, and its founders arrested. The news made headlines across the Bitcoin community the other day and accelerated Bitcoin’s stock-market-driven decline.

Why am I focusing on such a specific point? Because it is an example of one of the bigger risks around Bitcoin. While the government oversees your privacy, the truth is more nuanced. When it comes to big tech companies’ power, the government is pushing hard for privacy rights. However, when it comes to conducting anonymous financial transactions, the matter is very different. They directly affect the sovereignty of a state and its (fiat) currency.

The likelihood that more initiatives like Samourai Wallet will be banned remains significant, even if no crime is involved. This is something to consider in terms of Bitcoin exposure.

Bitcoin & Yellen

‘Priceless for USD 1 million.’

SENTIMENT

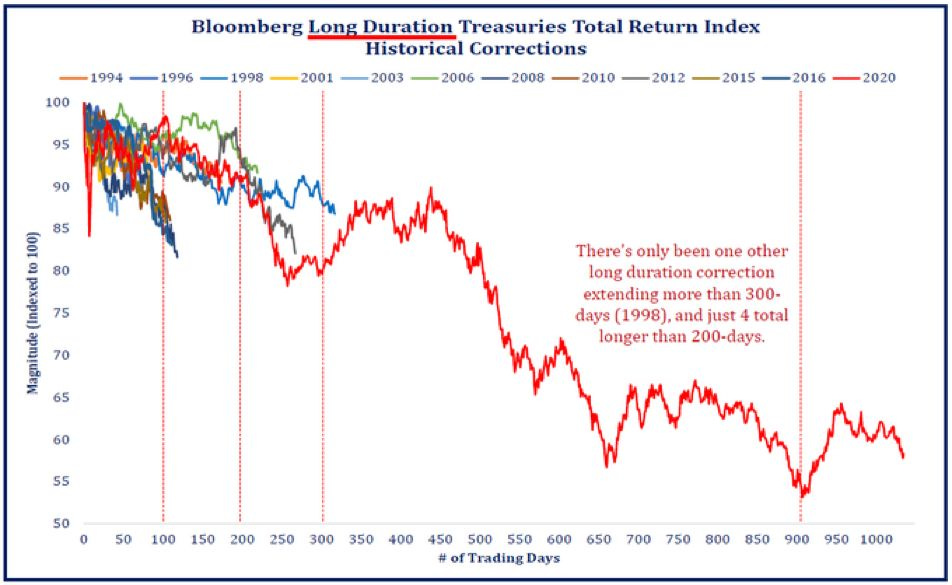

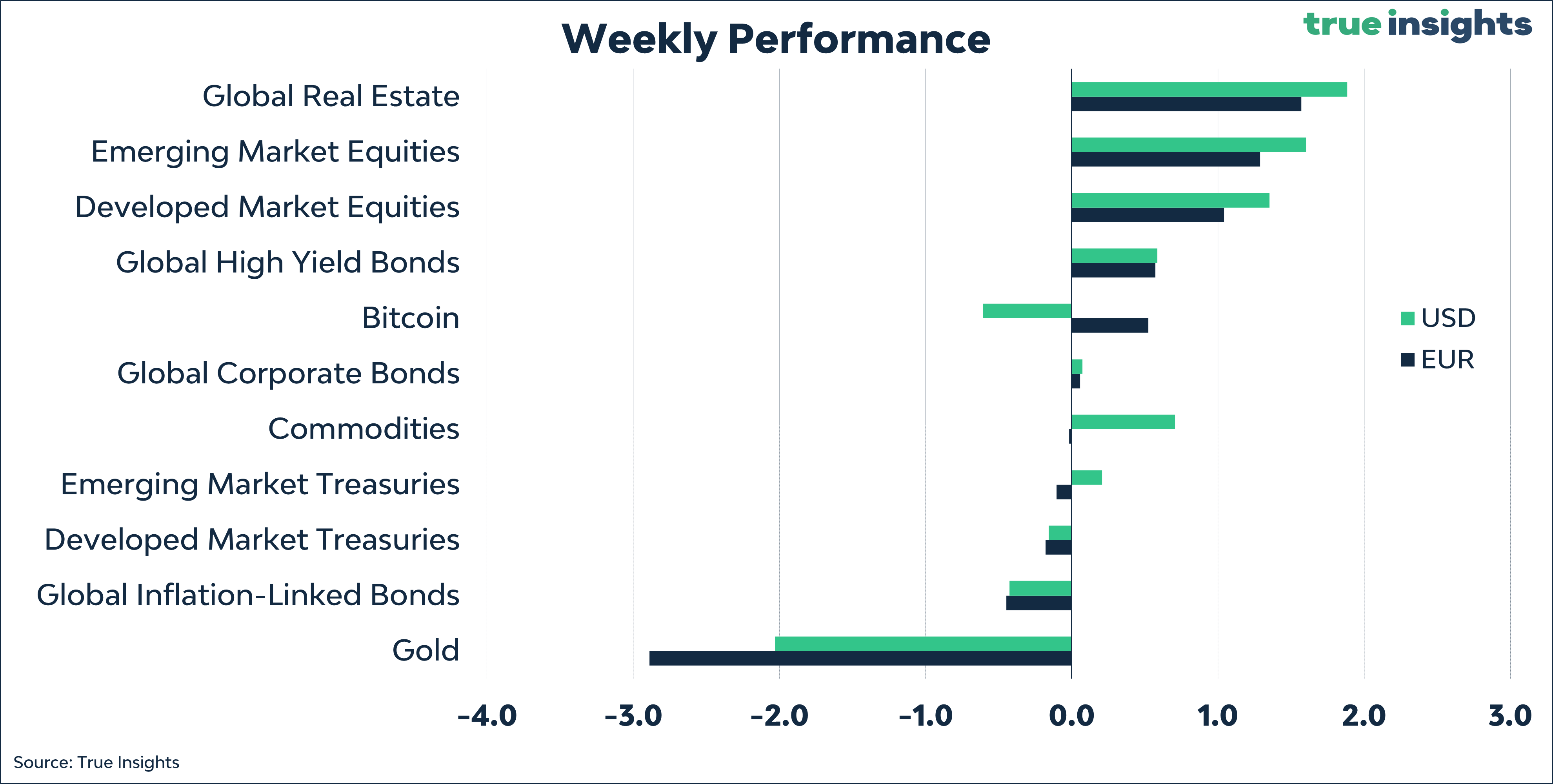

The Joy of Owning Bonds

This is by far the longest and deepest bond bear market.

And what many investors forget is that this came with higher volatility and fewer diversification benefits.

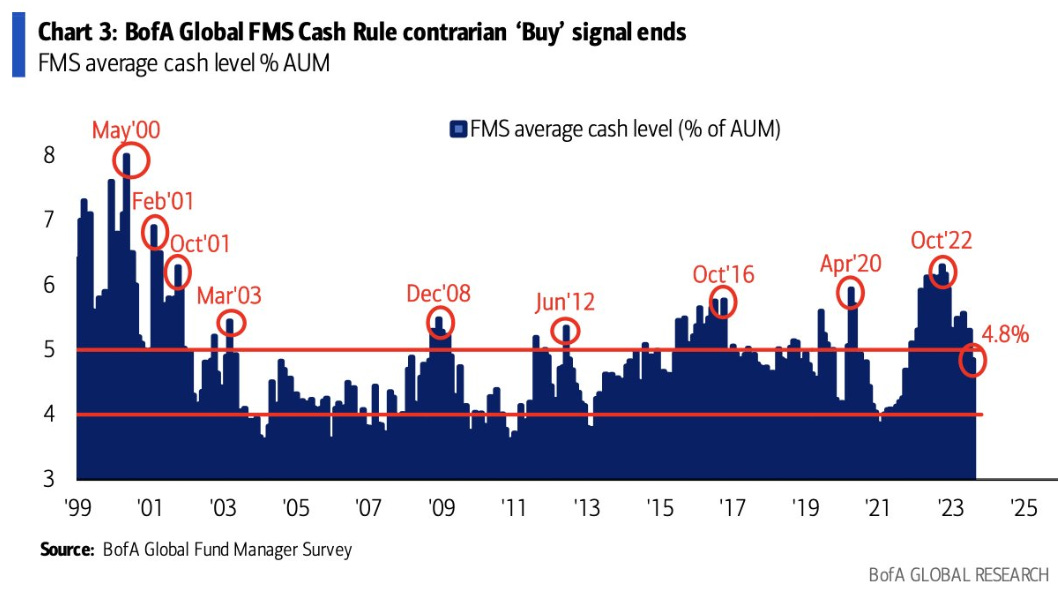

Bye ‘Buy’

Cash positions of global fund managers no longer signal a buying opportunity.

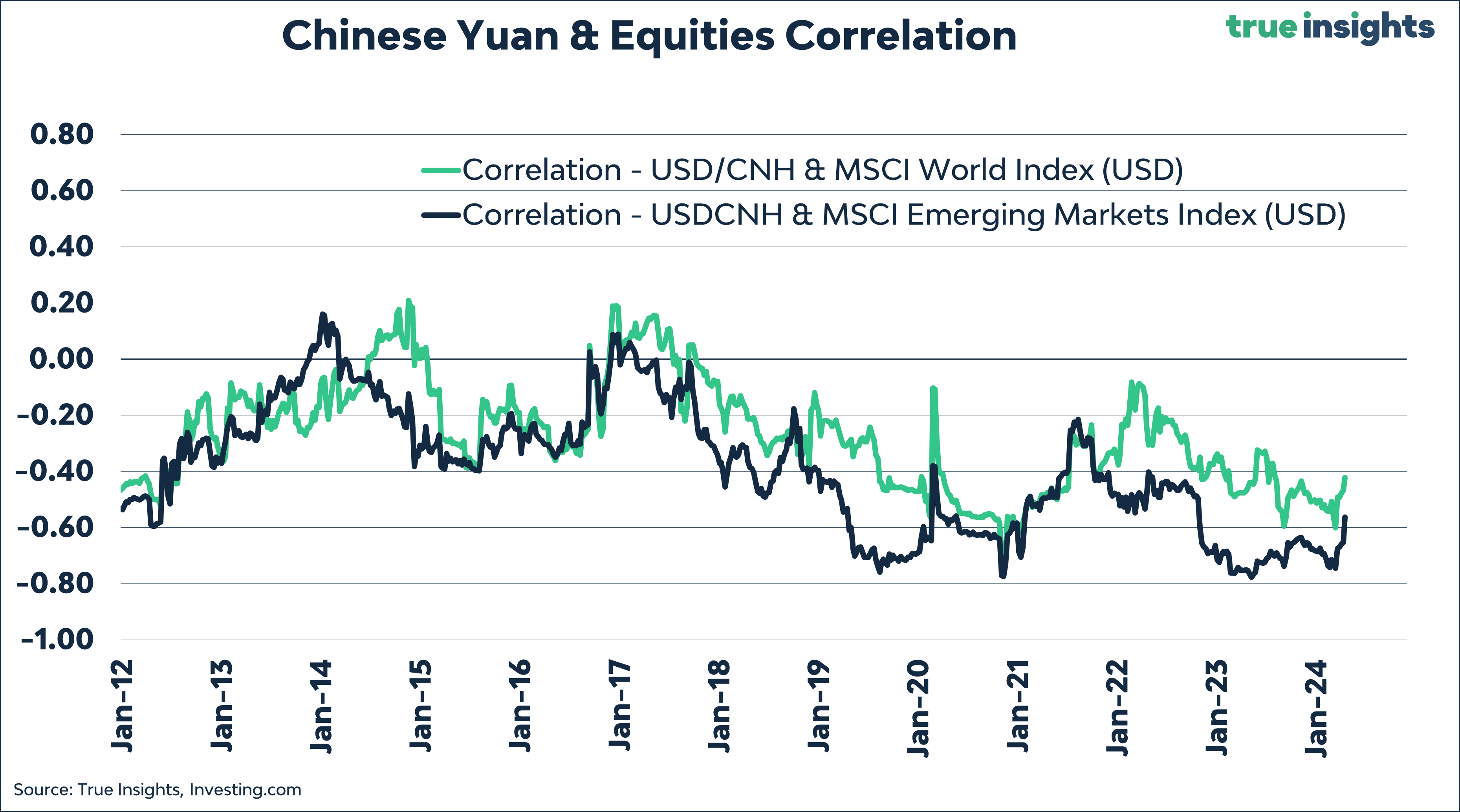

Yuan-ish

A Yuan depreciation is bad news for stocks. Those two do not go well together.

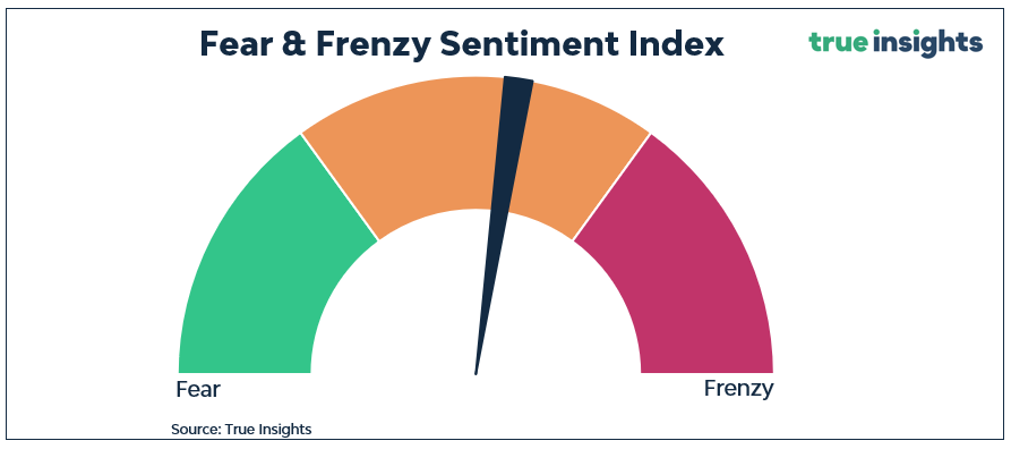

Fear & Frenzy

My Fear & Frenzy Sentiment Index has moved well away from Frenzy, yet is nowhere near Fear.

VALUATION

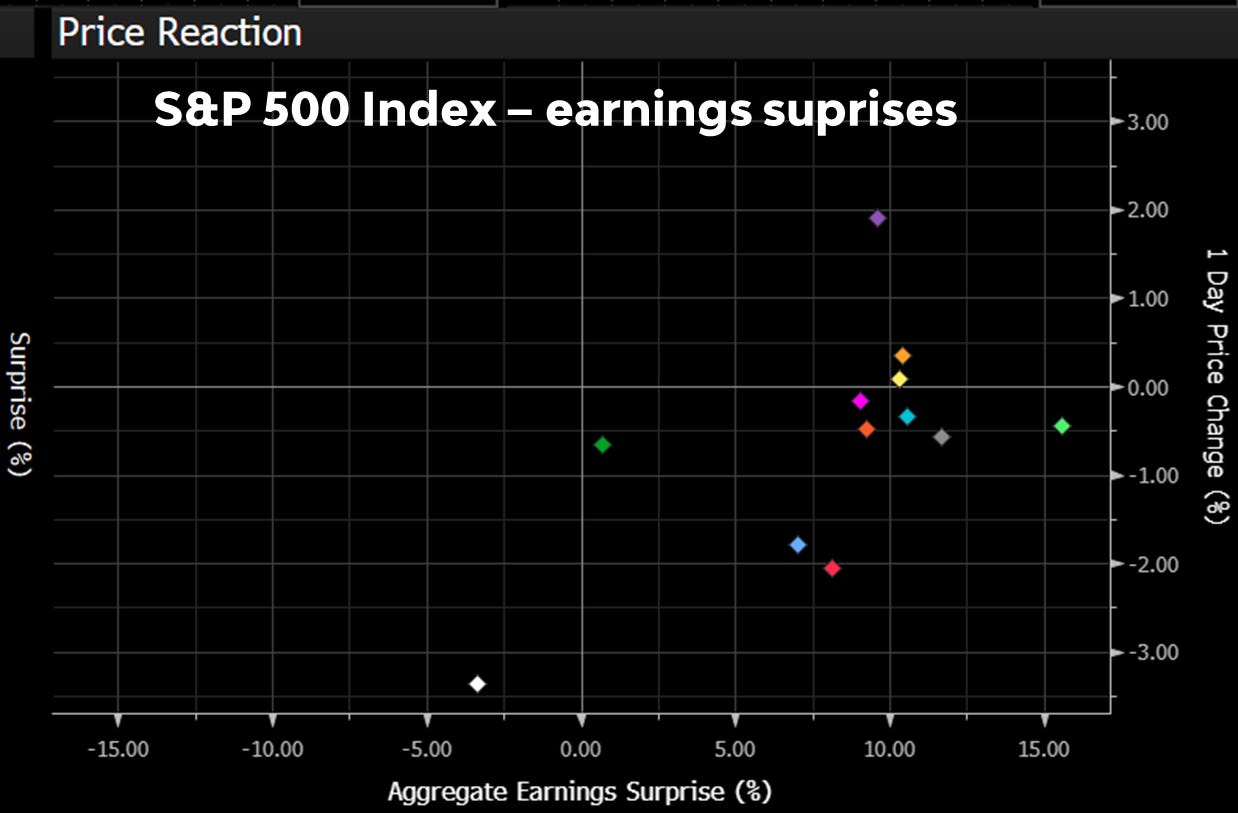

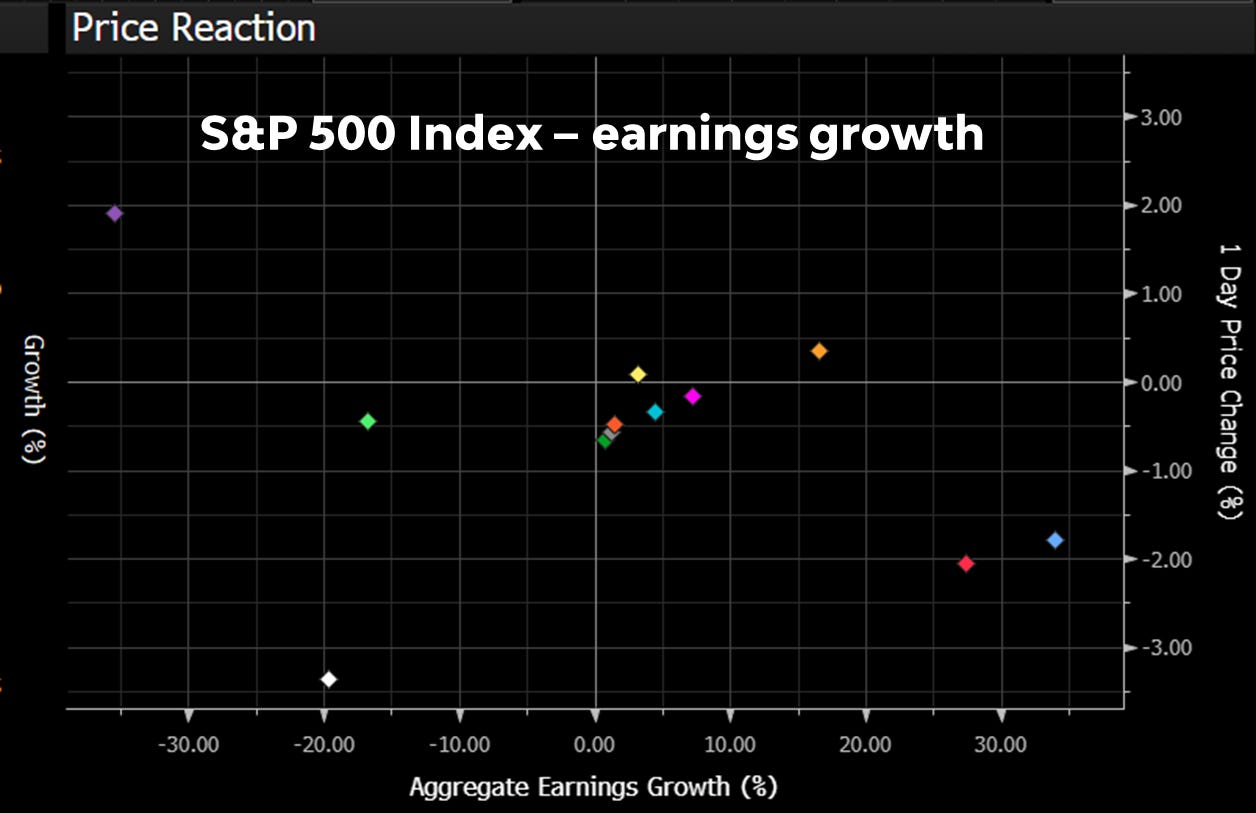

Earnings

Both earnings surprises,

and earnings growth does not look bad after about 200 S&P 500 companies have reported.

Earnings revisions for Developed Markets are positive

While not being the case for Emerging Markets.

CEO confidence, closely correlated to the outlook for earnings, is rising.

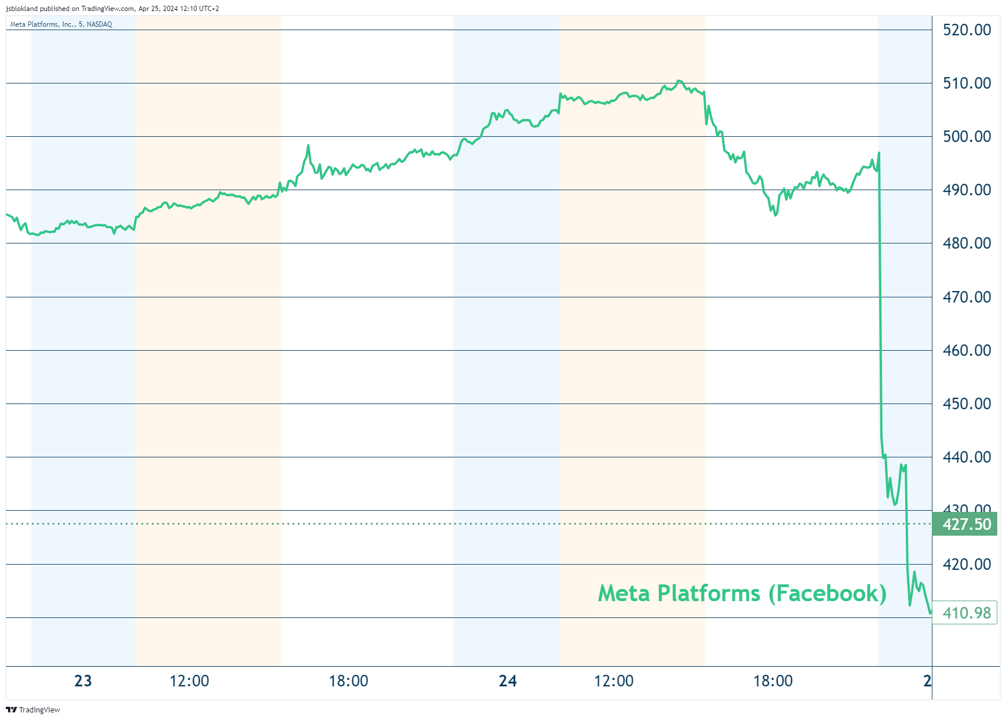

However, earnings reports of the famous headliners (TESLA, META) are mixed so far. META’s meager forecast once again shows just how extrapolated expectations can get.

Overall, geopolitical and central bank shenanigans have overshadowed the earnings season so far.

ENJOY YOUR WEEKEND!

JEROEN

MARKETS

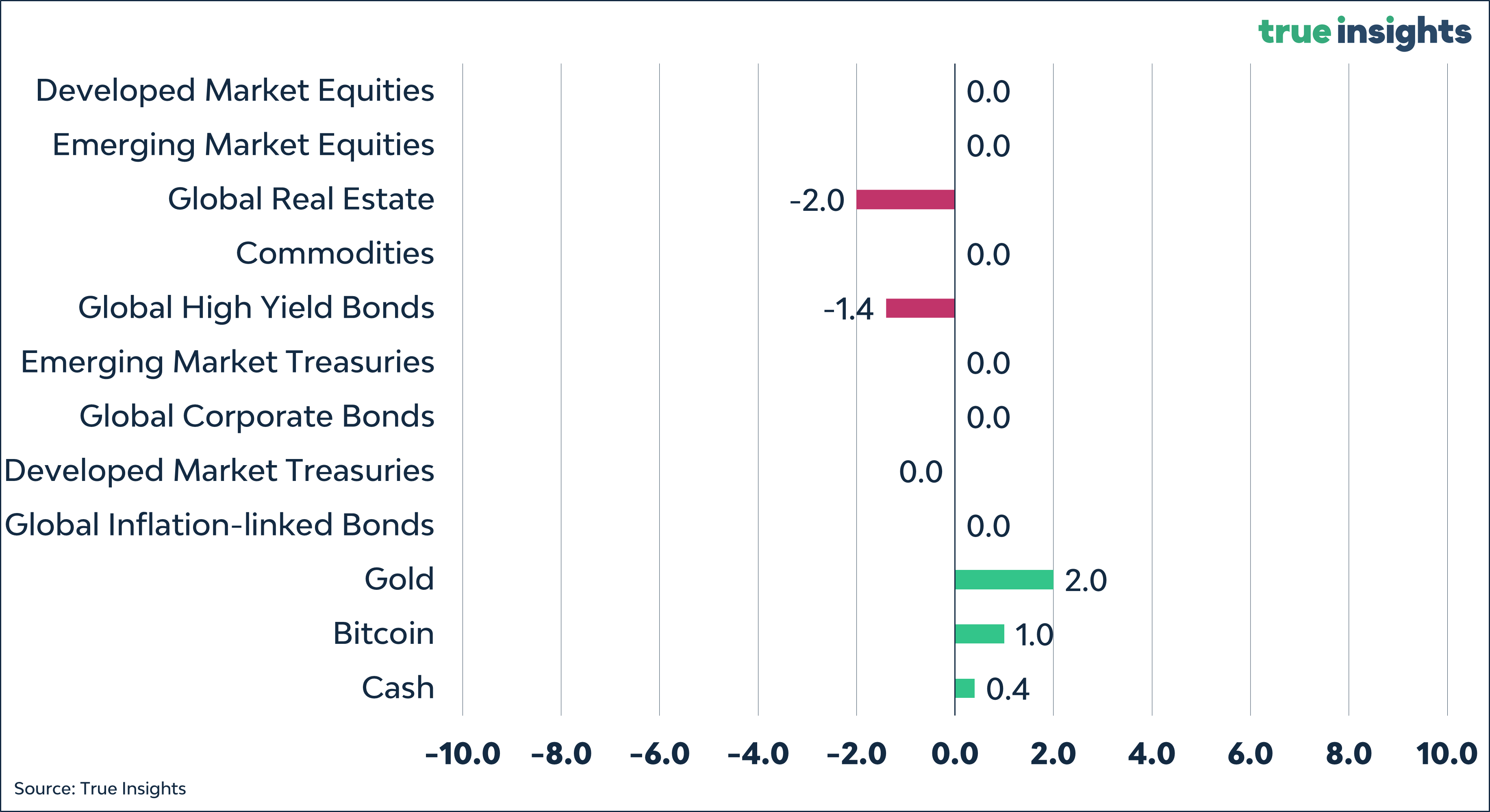

Active Weights

Balanced Portfolio