The Weekly Market Monitor – Powell & The Market May Soon Get What They Want!

The Weekly Market Monitor – Powell & The Market May Soon Get What They Want!

While he may not have enough confidence to cut rates, Powell has boosted sentiment and markets yet again!

First Things First – True Insights Will Come to an End

As I announced earlier this week, True Insights will be coming to an end. While I still derive satisfaction from helping investors interpret the markets and make investment decisions, I must make a choice. With the Blokland Smart Multi-Asset Fund, I believe I have created a unique investment solution that bridges two vastly different worlds: the traditional investment realm with its outdated 60-40 thinking and the alternative investments angle, which attracts investors bracing for the end of the world. Reality lies somewhere in between, and I expect this fund to significantly contribute to future-proof portfolios.

Don’t worry—I’m not going away. In fact, expect more useful content that will be available to everyone. You can find more about my decision and the process going forward here.

VALUATION

Earnings

S&P 500

At the time of writing, about 400 S&P 500 companies have reported their earnings, and a clear pattern emerges. Companies are beating on earnings but declining in price. This is primarily due to the negative macro momentum currently dominating market sentiment. However, the underlying profit development is solid, raising fewer questions about valuations. Fed Chairman Powell did his part to release pressure as well.

Stoxx 600

The dispersion across main sectors is wider for European stocks, but the overall picture is reasonably similar to that of the S&P 500 Index.

Shanghai Composite

The same cannot be said for China. Here, we see the opposite trend – negative earnings surprises combined with positive price changes – suggesting that the market bottom may be behind us. The Shanghai Composite Index is 15% higher than its February low but also 15% lower than its September 2021 peak.

Earnings Expectations – Back to Reality

Based on my four global earnings indicators—global Semiconductor Sales, Singapore Electronics Exports, South Korean Exports, and Chinese producer prices—earnings per share should grow by about 6% (measured year-on-year) in the coming months. This is not far from the long-term average and provides stocks with the opportunity to grow into their valuations.

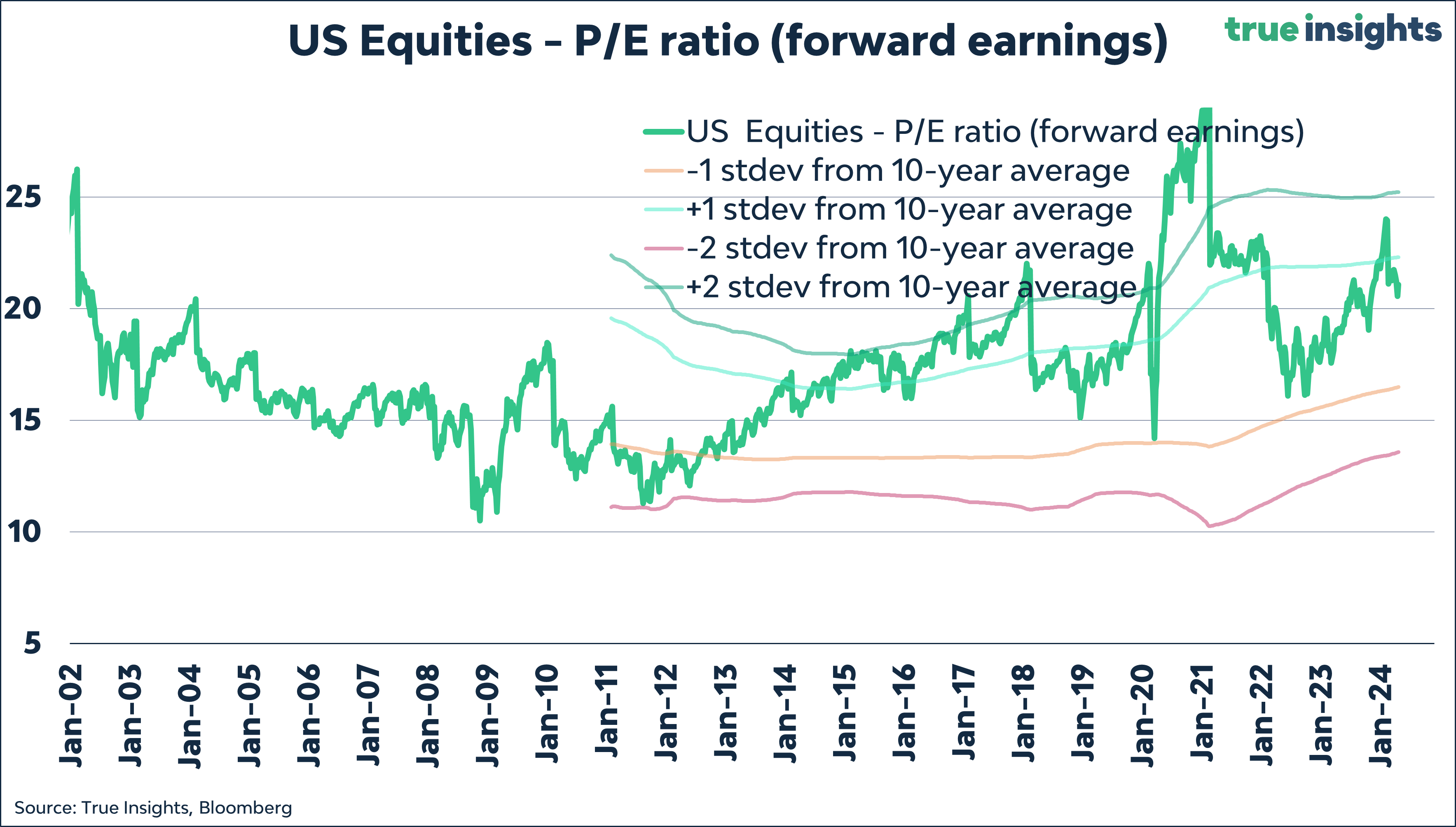

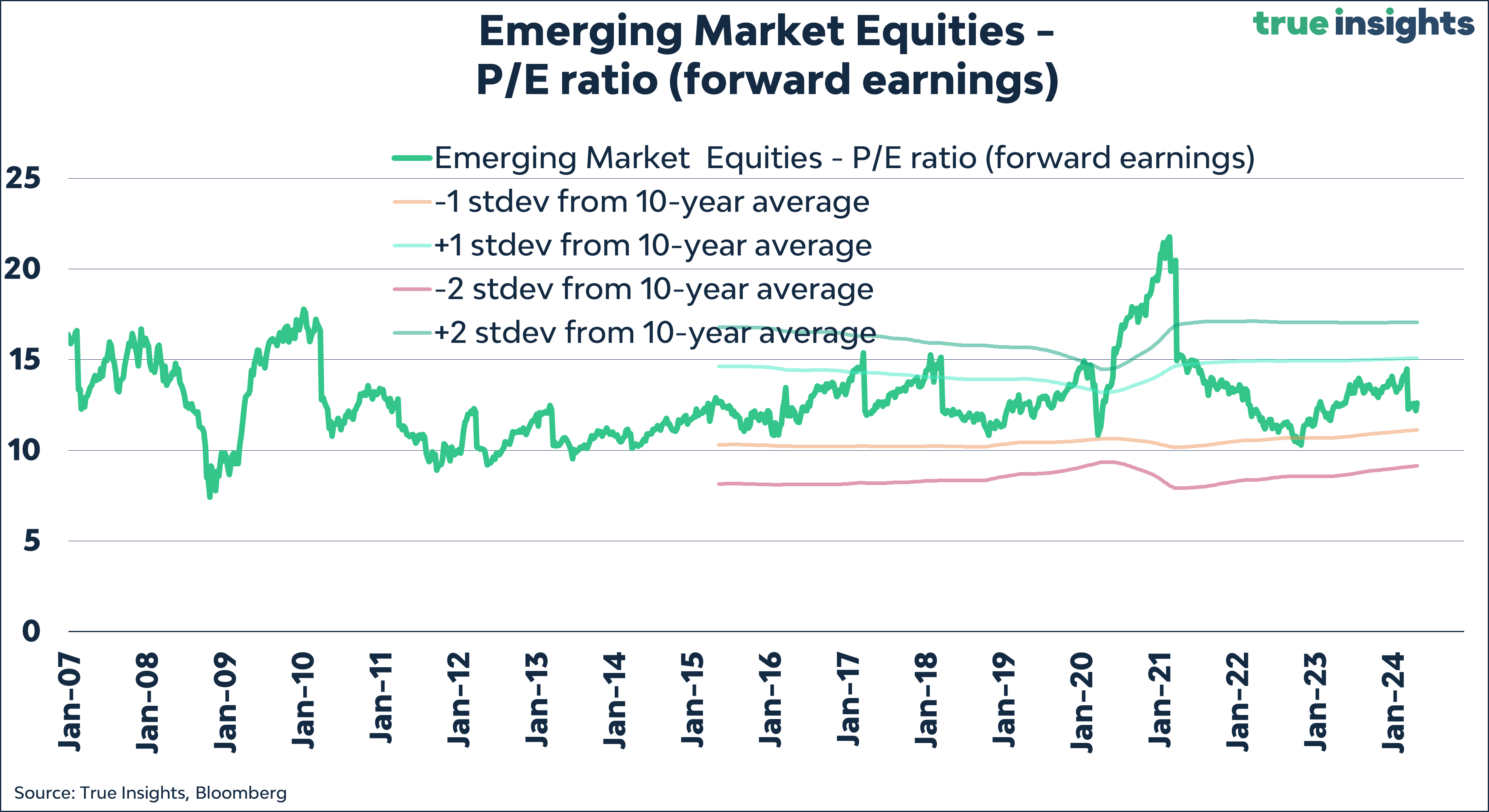

Equity Valuation – Not That Stretched

Although stocks are certainly not cheap, calling them expensive would also be inaccurate. As the chart below shows, the current forward P/E of the MSCI World Index sits neatly within one standard deviation bandwidth.

And while US stocks are expensive from an absolute perspective, they, too, fall neatly within one standard deviation bandwidth.

The same holds true for emerging markets, although the forward P/E ratio is at the lower end of the range. Despite the significant underperformance of the asset class, they are still not particularly cheap.

Got Yield?

Before you rush to buy more stocks, a caveat is that the above concerns only stand-alone valuations. When yields are considered, the picture looks very different. Why buy stocks when you can currently get 5% interest or short-term US Treasuries?

Finding a Bottom

Conclusion on earnings: While macro developments generally dominate earnings development, recent figures indicate that earnings should help limit the drawdown should the negative macro momentum continue.

Scarcity is in Equity, Not Debt

Finally, one more point regarding valuation. Companies continue to buy back their shares on a large scale, with Apple even setting a new buyback record. Another USD 110 billion of Apple shares will disappear. Meanwhile, this week, more billions of debt are being added. Equity capital is becoming increasingly scarce compared to debt capital, which will be reflected in the valuation between the two.

MACRO

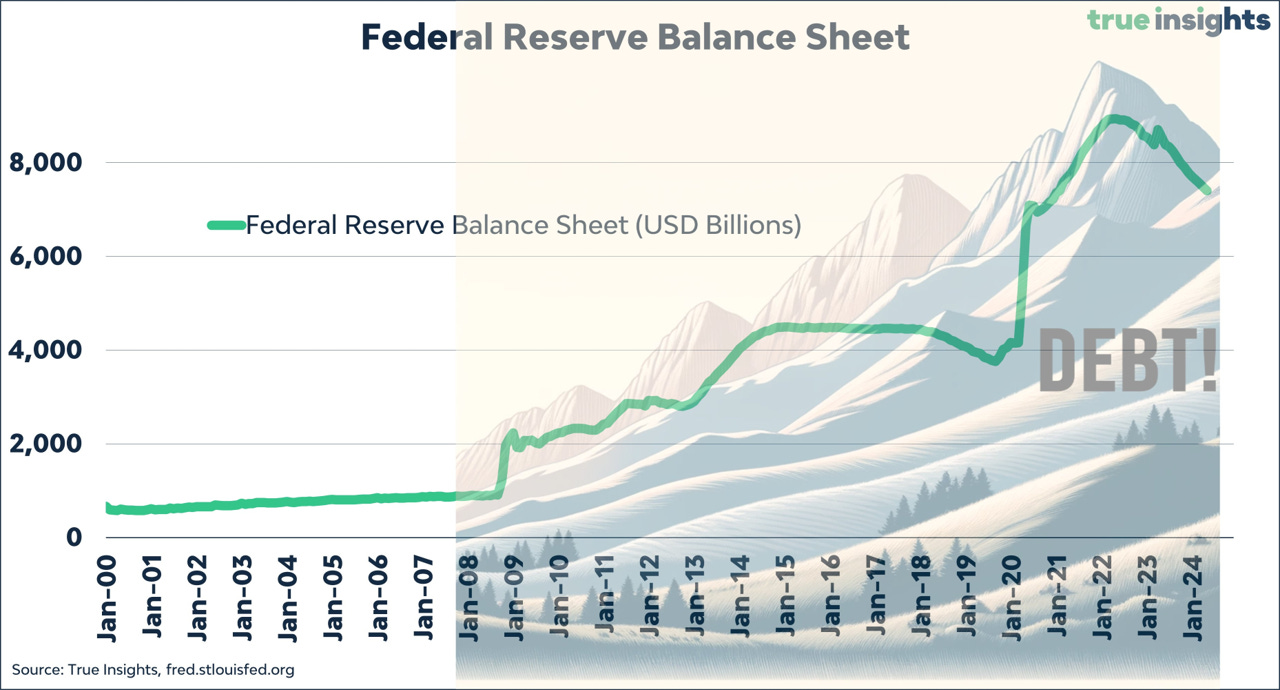

How Do You Like Your Balance Sheet? Big, Please!

I’ve talked at length this week, but the Fed’s decision to reduce Quantitative Tightening at this stage says a lot about its intentions. Starting from June, the Federal Reserve will reduce its monthly sales of government bonds from USD 60 billion to USD 25 billion—less than half the current amount.

Leverage

Before I get to the key point, there is a rationale for why central bank balances can justifiably be larger than before the Great Financial Crisis. With subprime mortgages, leverage also contributed to the financial system’s near collapse. Bad loans with high credit ratings were excessively stacked and, coupled with a lack of quality assets on the bank balances, created a spill-over effect that quickly evaporated bank equity capital.

One of the outcomes of the Great Financial Crisis was that banks and financial institutions were required to maintain much larger capital buffers, often in the form of government bonds. The forced reduction in leverage made liquidity issues more likely, as everyone needed to seek out high-quality assets that could serve as buffers. Central banks need a larger balance sheet to better manage this liquidity risk.

Convenience

There is, of course, another convenient aspect to large central bank balances. They grant monetary policymakers much more firepower to push interest rates down when the economy is struggling, or a new crisis emerges. Who benefits the most from increased liquidity? Risky investments like stocks, high-yield bonds, Bitcoin, etc. Markets always want liquidity, and Powell just gave them some more.

International Issue

The need for larger balance sheets is not limited to the United States. One could argue that because the US is a combination of a world power, possesses the deepest and most liquid Treasury market, and issues the world’s reserve currency, other central banks feel even greater pressure to engage in extreme monetary policies.

The European Central Bank (ECB) might come to mind first, but China, with its massive debt load and declining potential growth, will do exactly the same. Interest rates, on average, need to remain low.

Two Parts of the Mandate

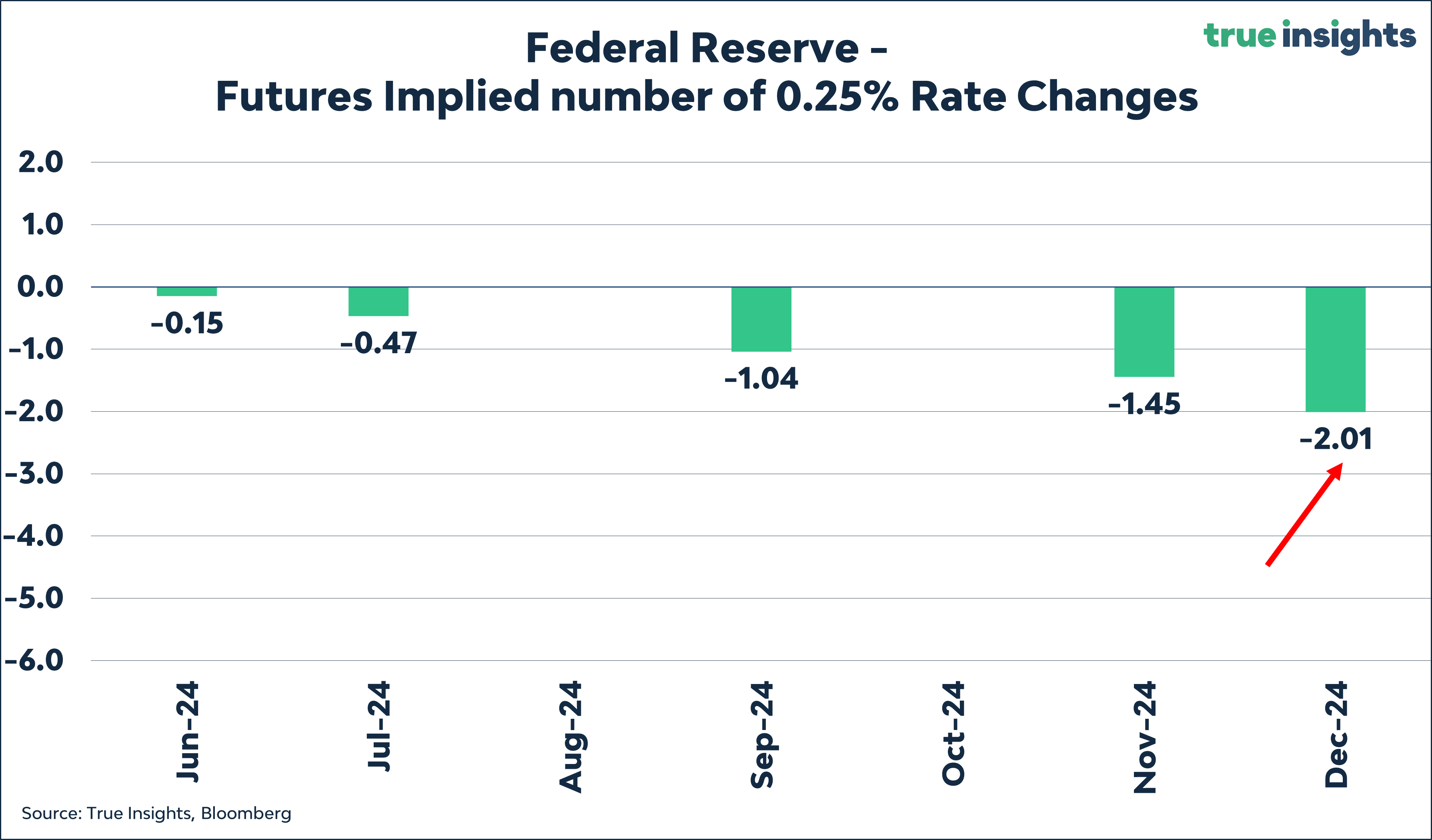

Powell requires weakness on the other side of his mandate, employment, to open the door to interest rate cuts this year. He was served well, much to the satisfaction of all risky assets.

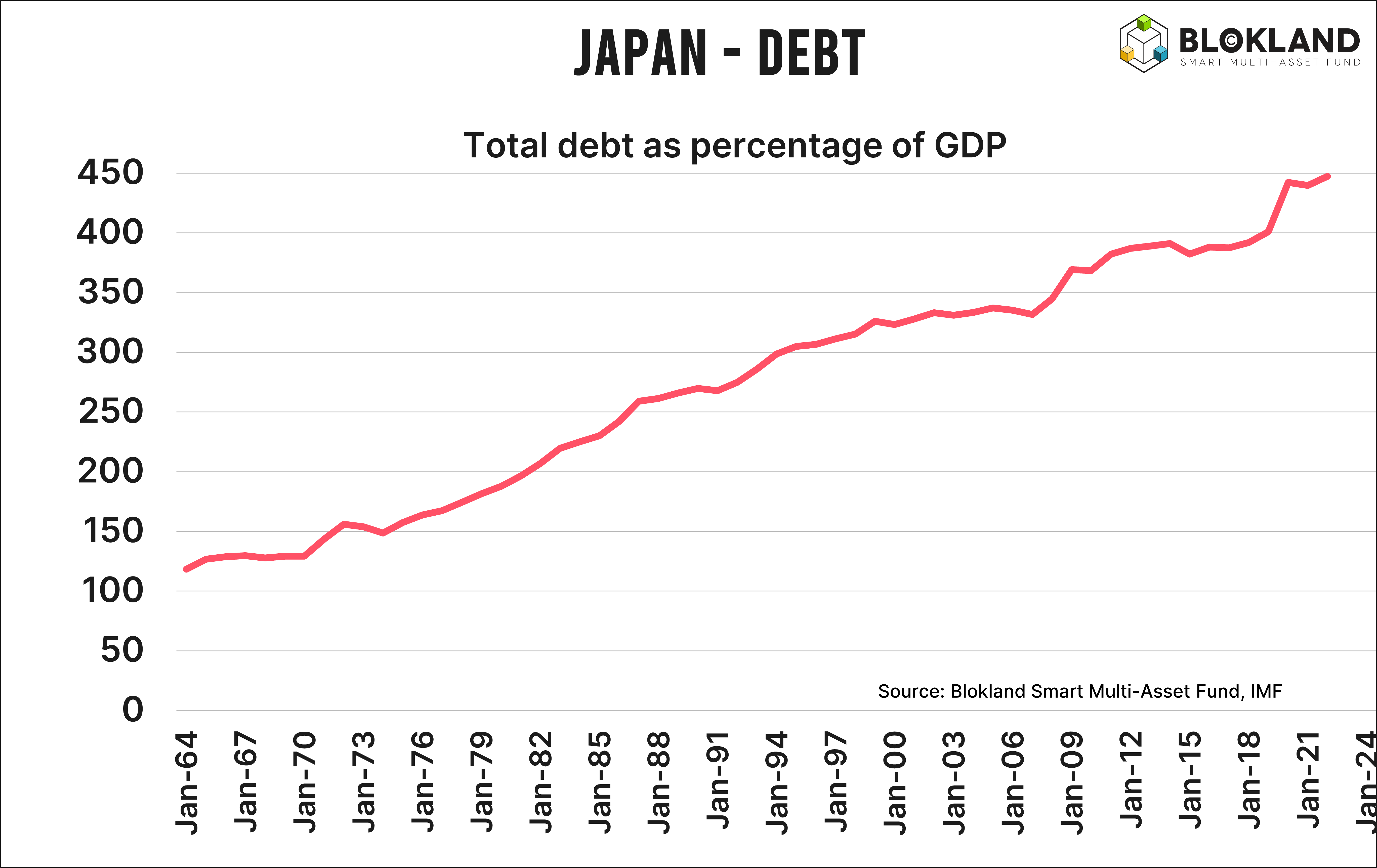

Japanification is Still Real

Japan remains the quintessential example. It has a total debt-to-GDP ratio of nearly 450%.

The Bank of Japan owns nearly 50% of all outstanding government bonds.

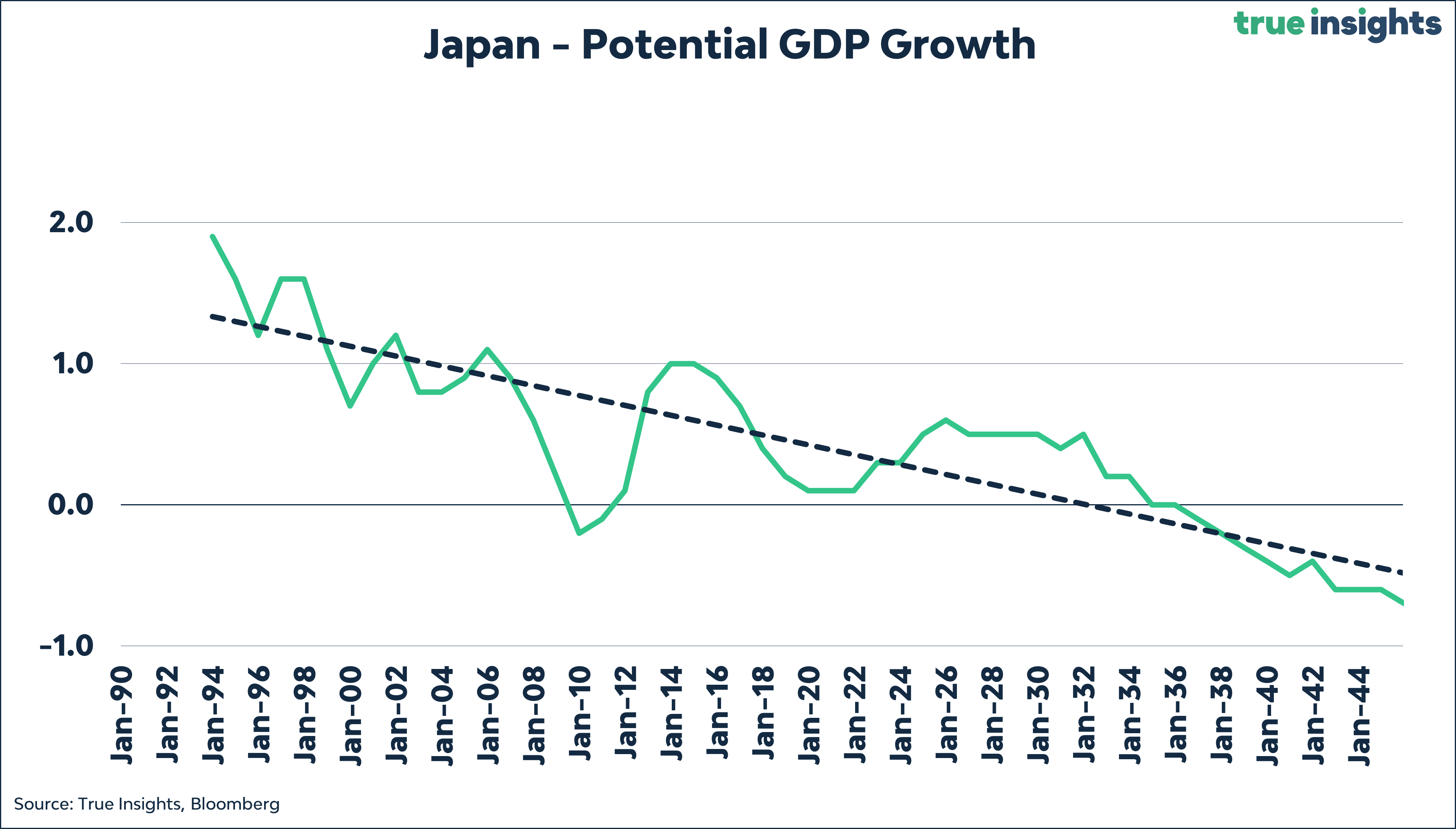

Japan’s potential GDP growth will turn negative in the not-so-distant future.

As a result, its 10-year government bond yield is a paltry 0.89% after the biggest global tightening cycle in decades.

For the eternal optimists among us, Japan is still here, and the country is not doing too poorly. To some extent, this is true because the principle of more debt, a bit of growth, and ever-lower interest rates holds to this day.

However, the combination of high debt, low interest rates, and low growth must manifest somewhere, and that is in the Japanese yen. Below is a chart of the Nikkei Index measured in gold and yen. That is one hell of a gap!

Returning to this week. The Ministry of Finance can intervene as it wishes, and of course, the signaling may temporarily stop depreciation. Still, with other regions less advanced in the Japanification mode after the latest tightening cycle, the pressure on the yen remains immense.

This also creates geopolitical tensions as China aims to stabilize its currency to avoid triggering more capital outflows at the expense of its competitive position in Asia and beyond.

SENTIMENT

Fear & Frenzy

My Fear & Frenzy Sentiment Index remains firmly in Neutral territory.

MARKETS