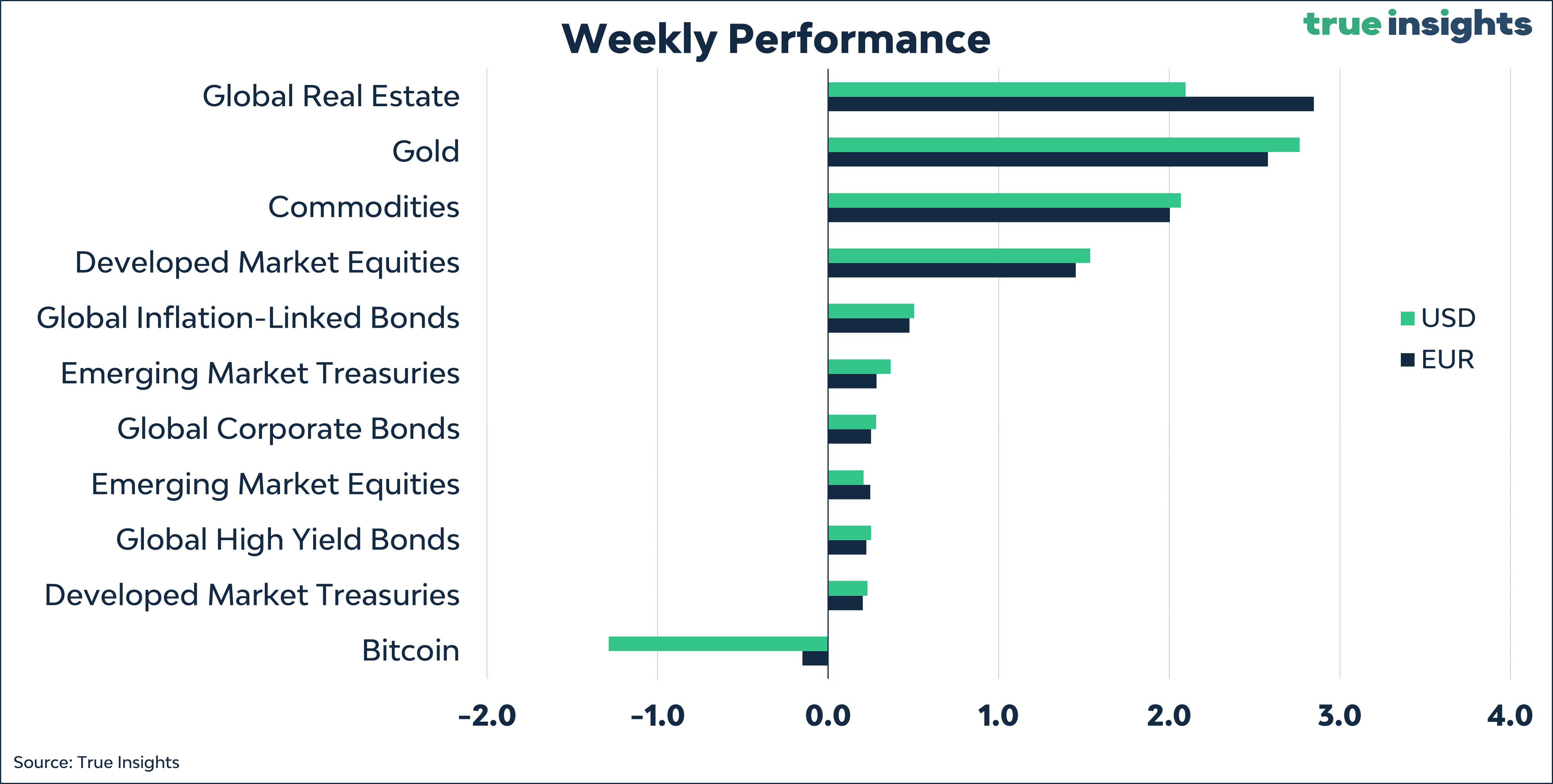

The Weekly Market Monitor – Total Return is dead; long live Gold!

Bill Gross is throwing the towel on bonds. I have been there for quite some time, confirming the great migration is underway.

First Things First – True Insights Will Come to an End

As I announced earlier this week, True Insights will be coming to an end. While I still derive satisfaction from helping investors interpret the markets and make investment decisions, I must make a choice. With the Blokland Smart Multi-Asset Fund, I believe I have created a unique investment solution that bridges two vastly different worlds: the traditional investment realm with its outdated 60-40 thinking and the alternative investments angle, which attracts investors bracing for the end of the world. Reality lies somewhere in between, and I expect this fund to significantly contribute to future-proof portfolios.

Don’t worry—I’m not going away. In fact, expect more useful content that will be available to everyone. You can find more about my decision and the process going forward here.

MACRO

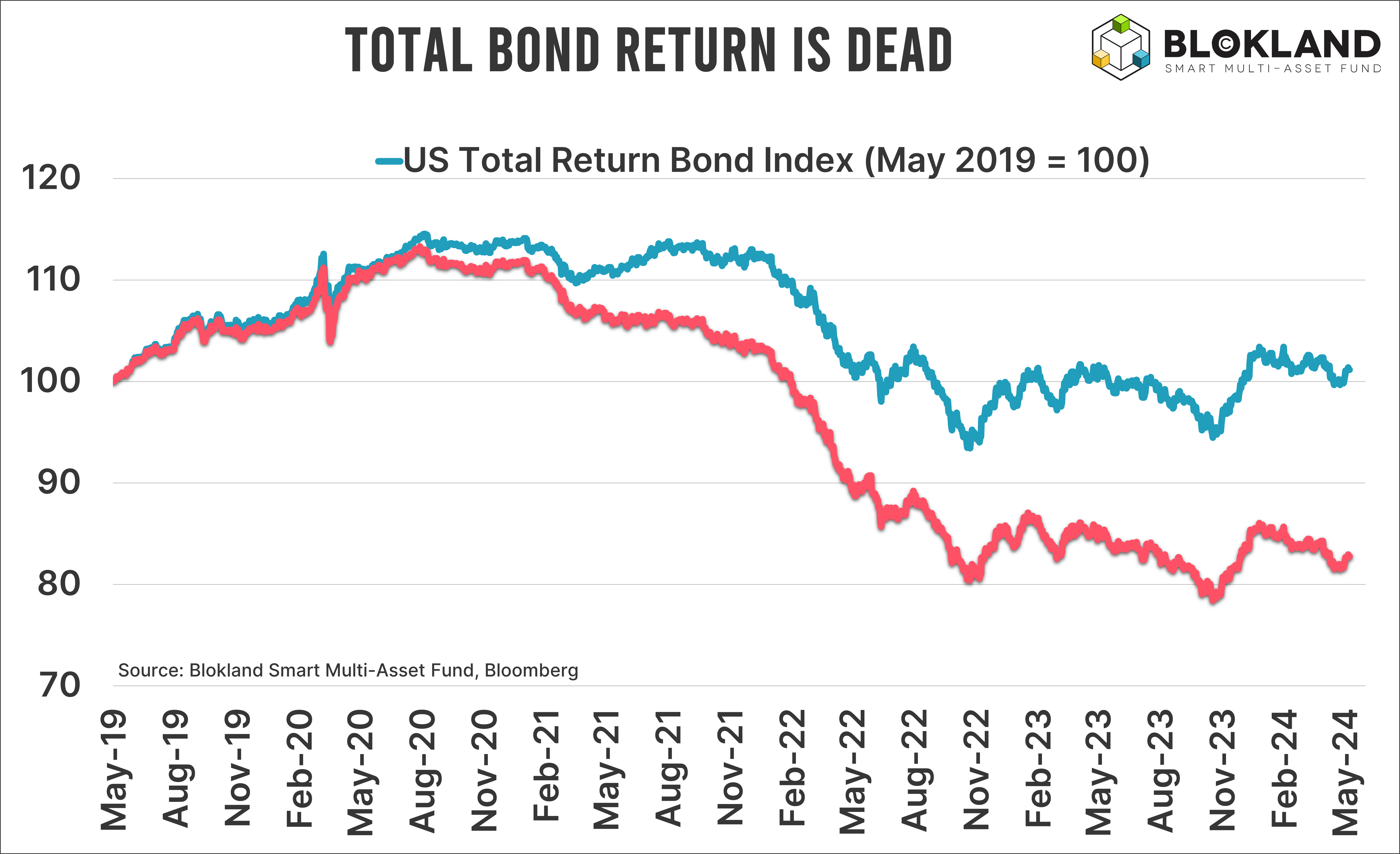

Total Return is dead

Bill Gross no longer believes in the ‘total return’ concept for bonds. In fact, in his latest blog, he basically states that total return is dead after realizing zero return over the last five years.

The chart below shows the Bloomberg US Total Return Bond Index, which, indeed, has gone nowhere in the past five years. To make things worse, I adjusted the Total Return Bond Index for inflation, resulting in an average negative return of over 4% over the past five years.

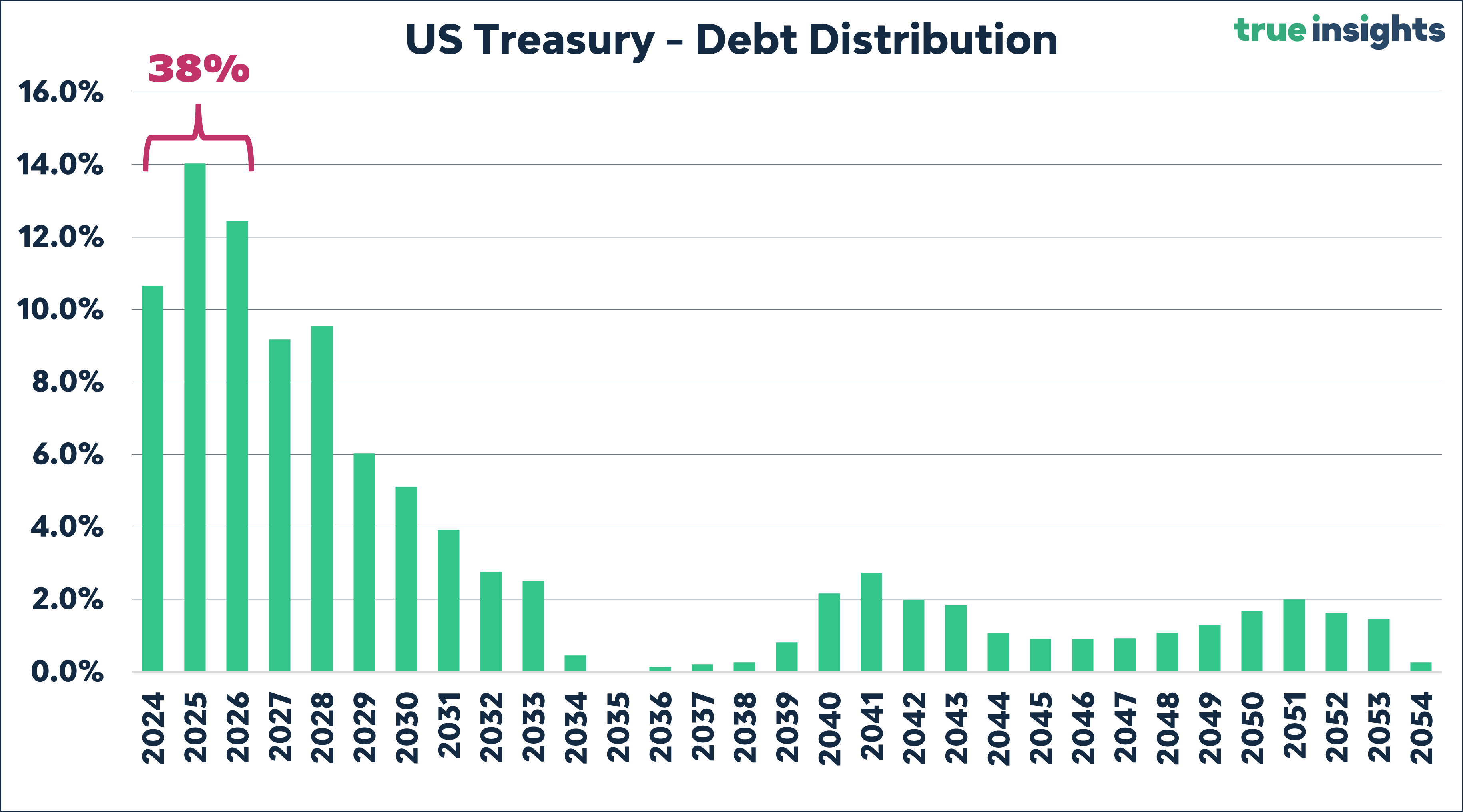

Unsurprisingly, Gross’s biggest worry concerning future bond returns is debt. If the US wants to keep growing, it must issue tons of additional debt. Paradoxically, the higher interest rates go, the lower the return on bonds, and the more debt the US must issue.

Gross also argues that at 4.6%, the margin of error (to realize positive returns) is relatively small compared to when the total return concept originated in the 1980s. In his blog, he mentions that bond market pundits expect 4% yields and 2-3% inflation. But that inflation outlook is pretty mild, with risks clearly on the upside.

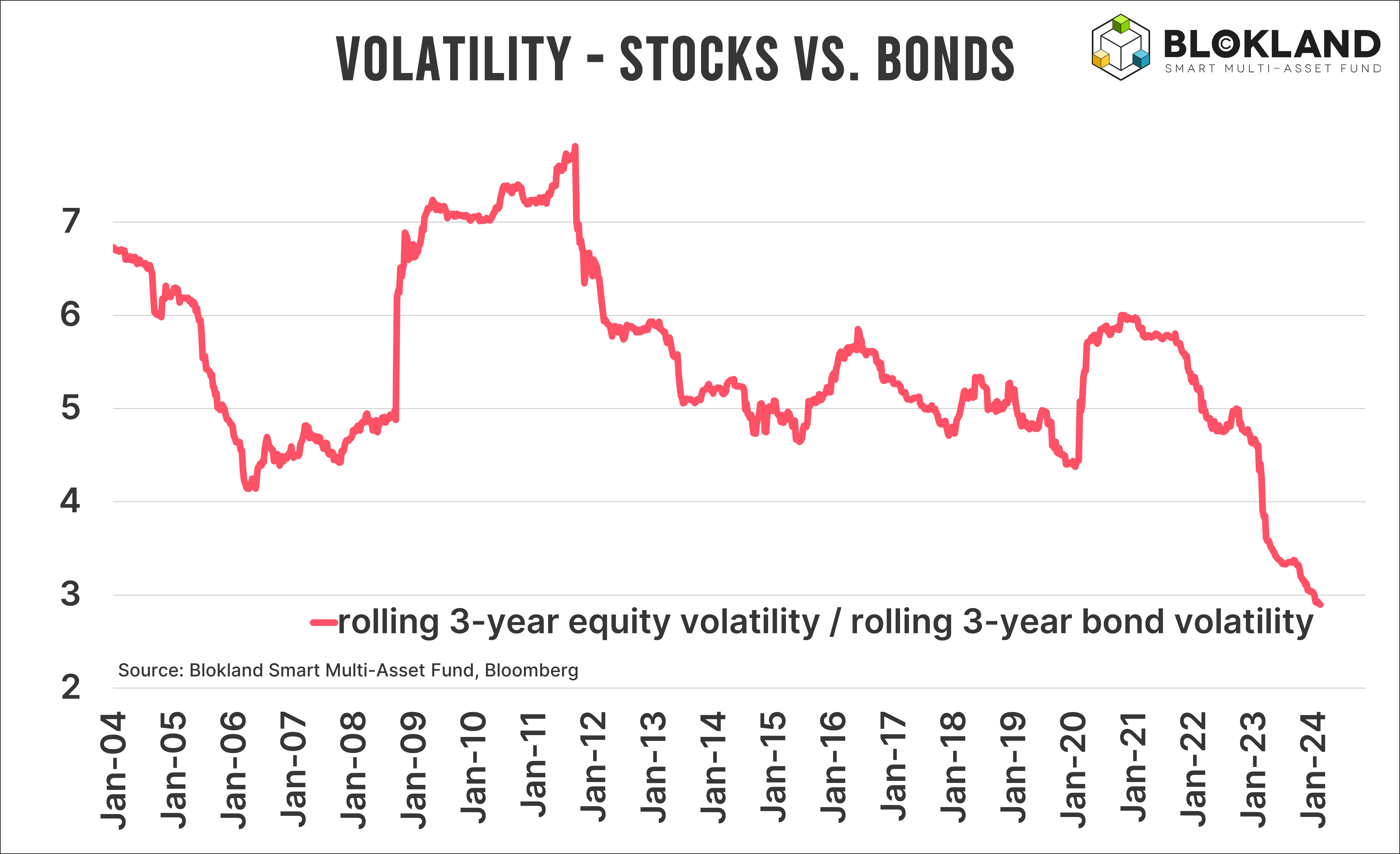

To complete the outlook for bonds, we must add volatility and diversification. And both of them are far less compelling than they used to be. The chart below shows the ratio of realized volatility of equities vs. bonds. It has been going down like crazy, largely explained by a (structural) increase in bond market volatility. By the way, implied volatility (MOVE Index vs. VIX Index) will give you the same result.

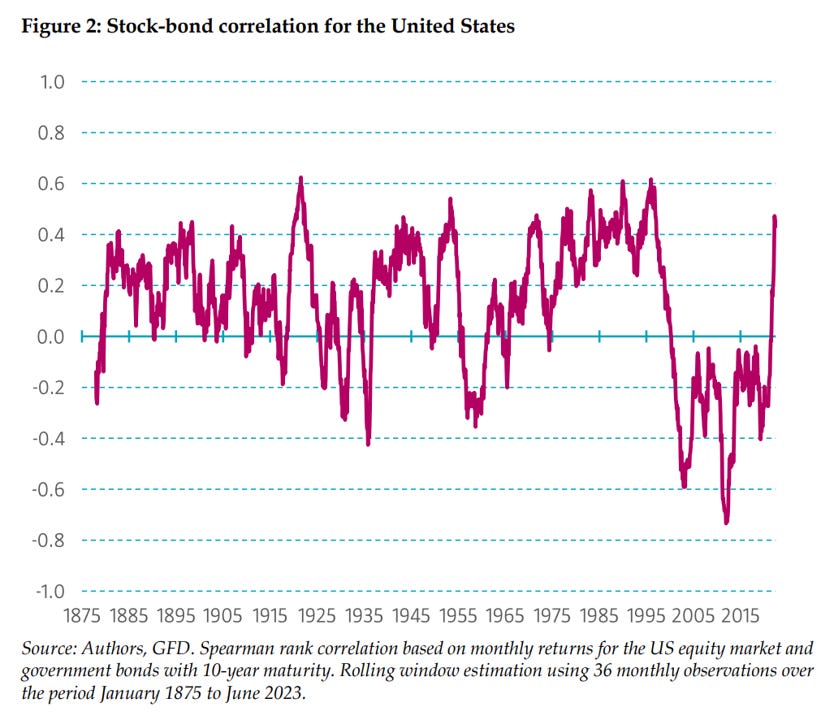

Finally, I expect the correlation between equities and bonds to become positive more often. As my ex-colleagues at Robeco neatly revealed, positive correlation has been the norm, with 1980-2020 being the exception.

I expect a massive diversification from abundant bonds into scarce assets in the coming years. Every multi-asset portfolio should reflect this migration.

Snooze the SLOOS?

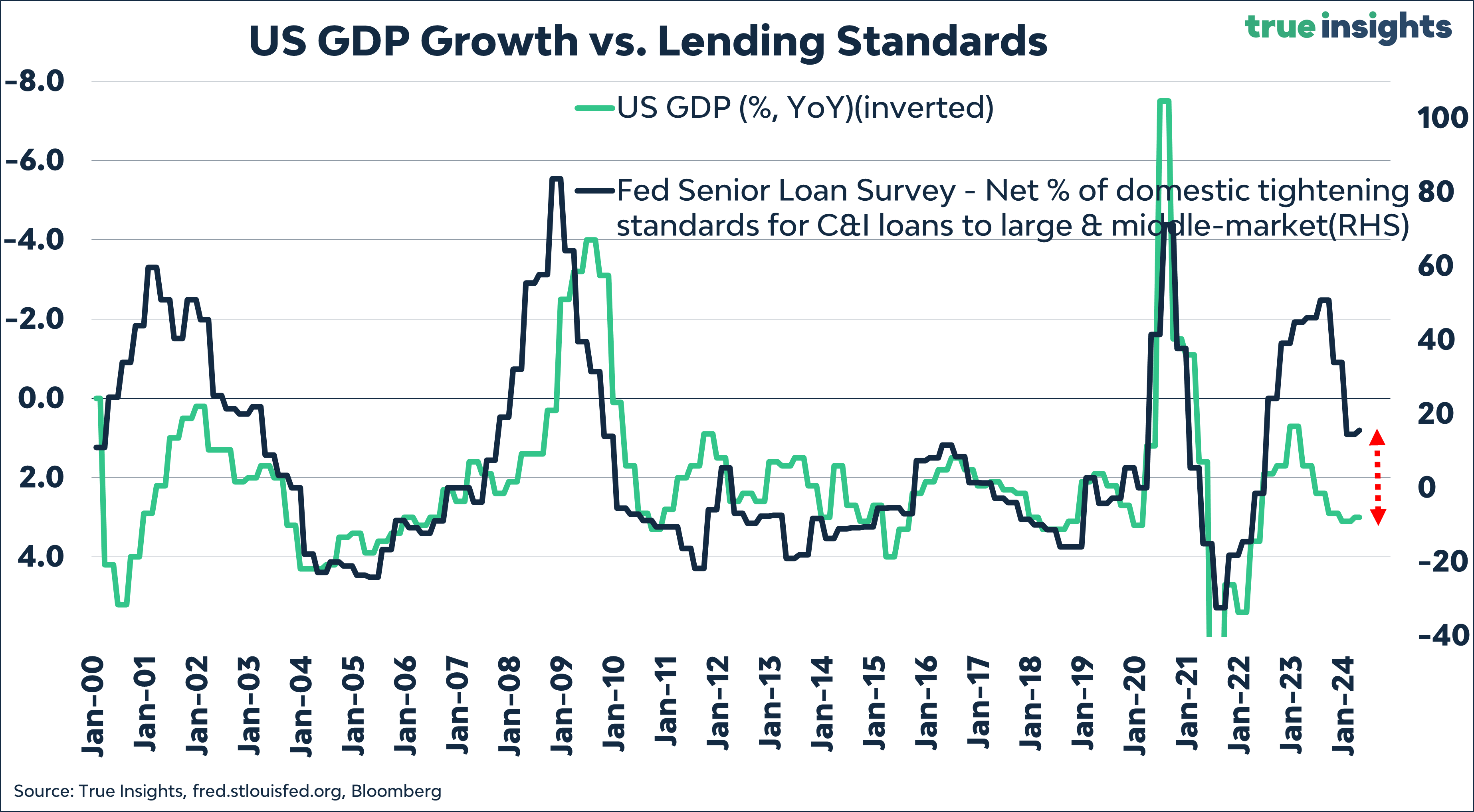

This week, the Federal Reserve released its latest Senior Loan Officer Opinion Survey on Bank Lending Practices, SLOOS. Below are the key findings:

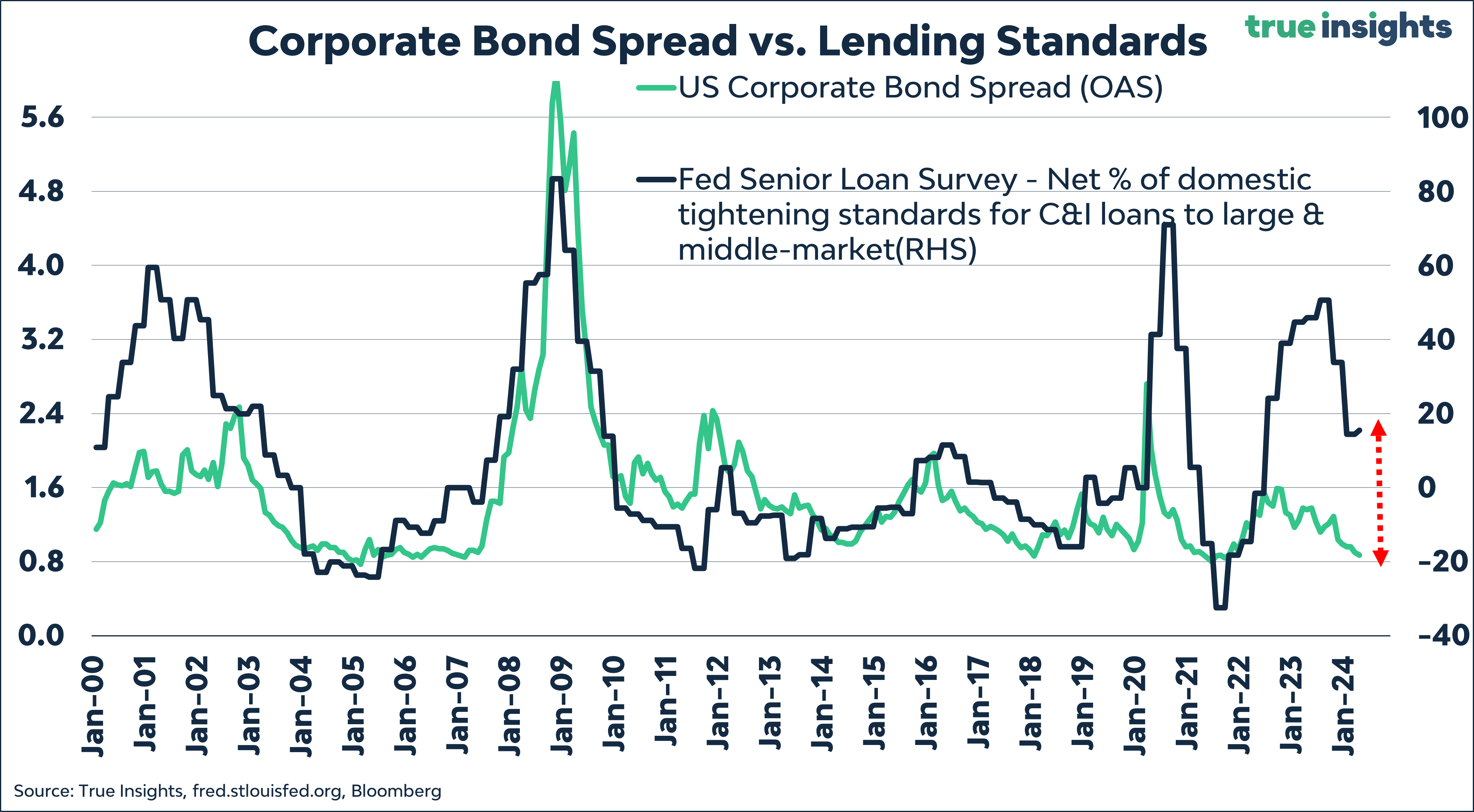

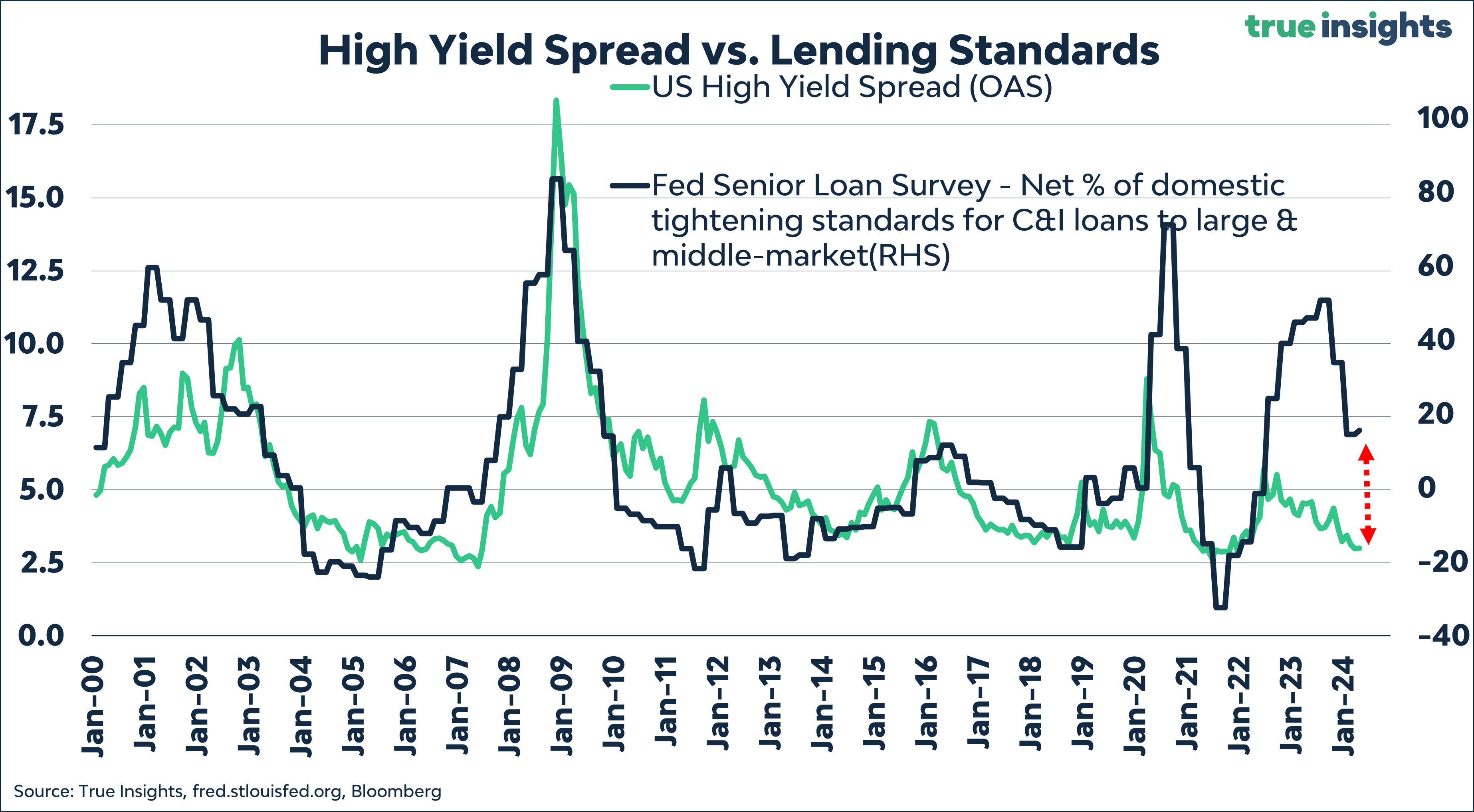

In the first quarter, banks slightly tightened their lending standards. However, this was at a level that is already quite tight from a historical perspective. Consequently, the SLOOS indicates a further weakening of the US economy.

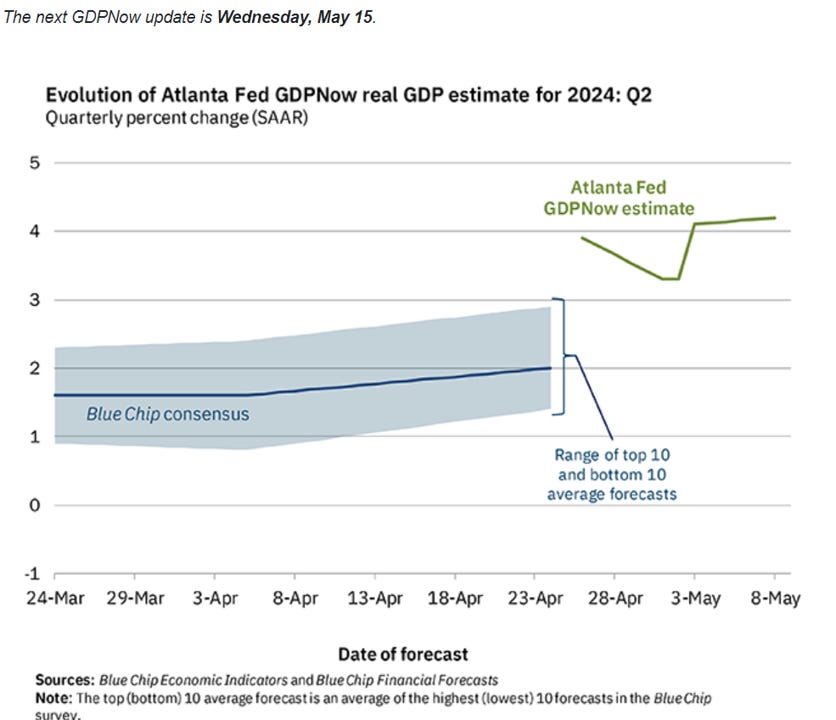

Moreover, the Atlanta Fed GDP Nowcast forecasts a 4.2% annualized growth in Q2.

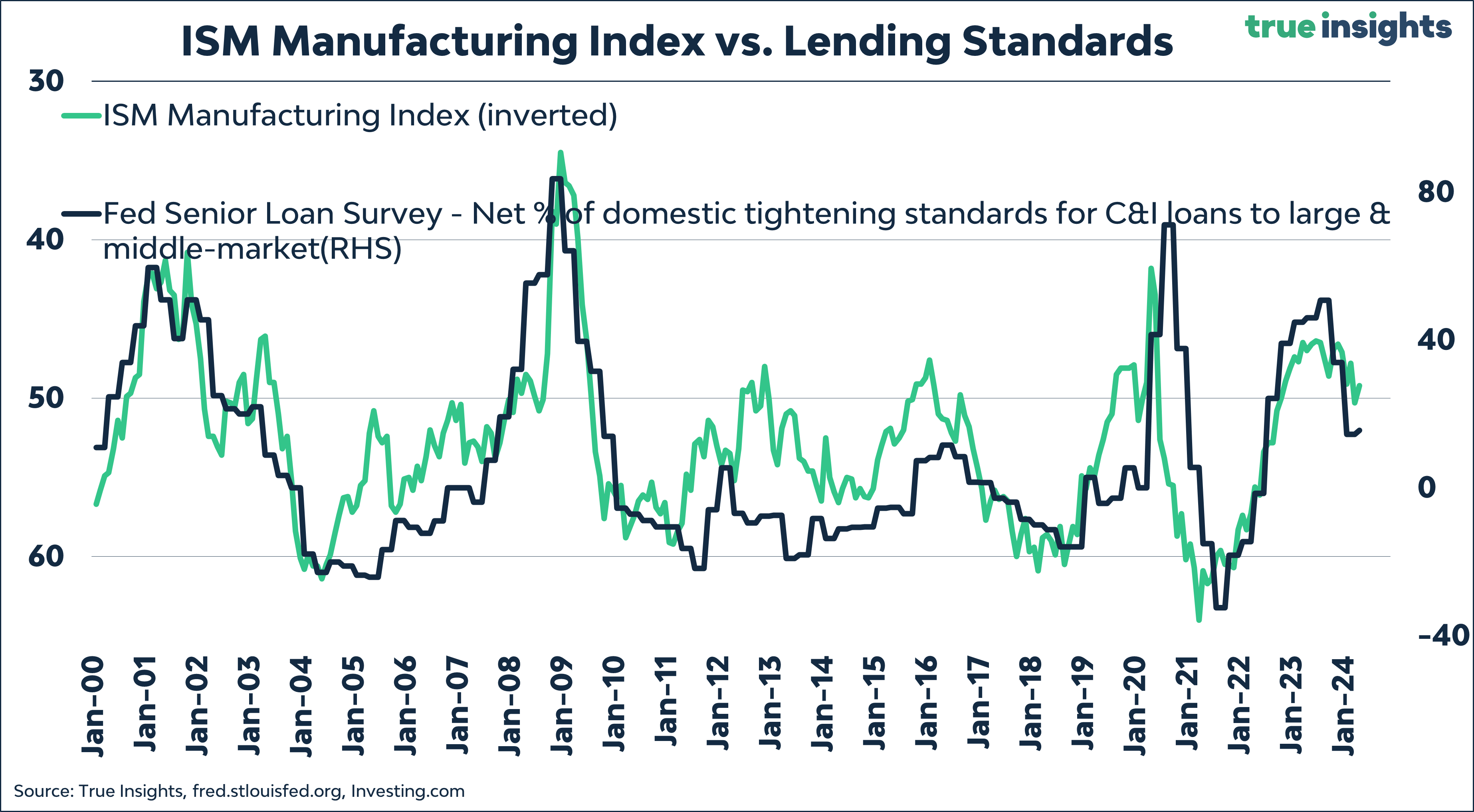

For months, the ISM Manufacturing Index has been pointing to a macro picture weaker than the SLOOS.

Corporate bond spreads are excessively tight.

High yield bond spreads are excessively tight.

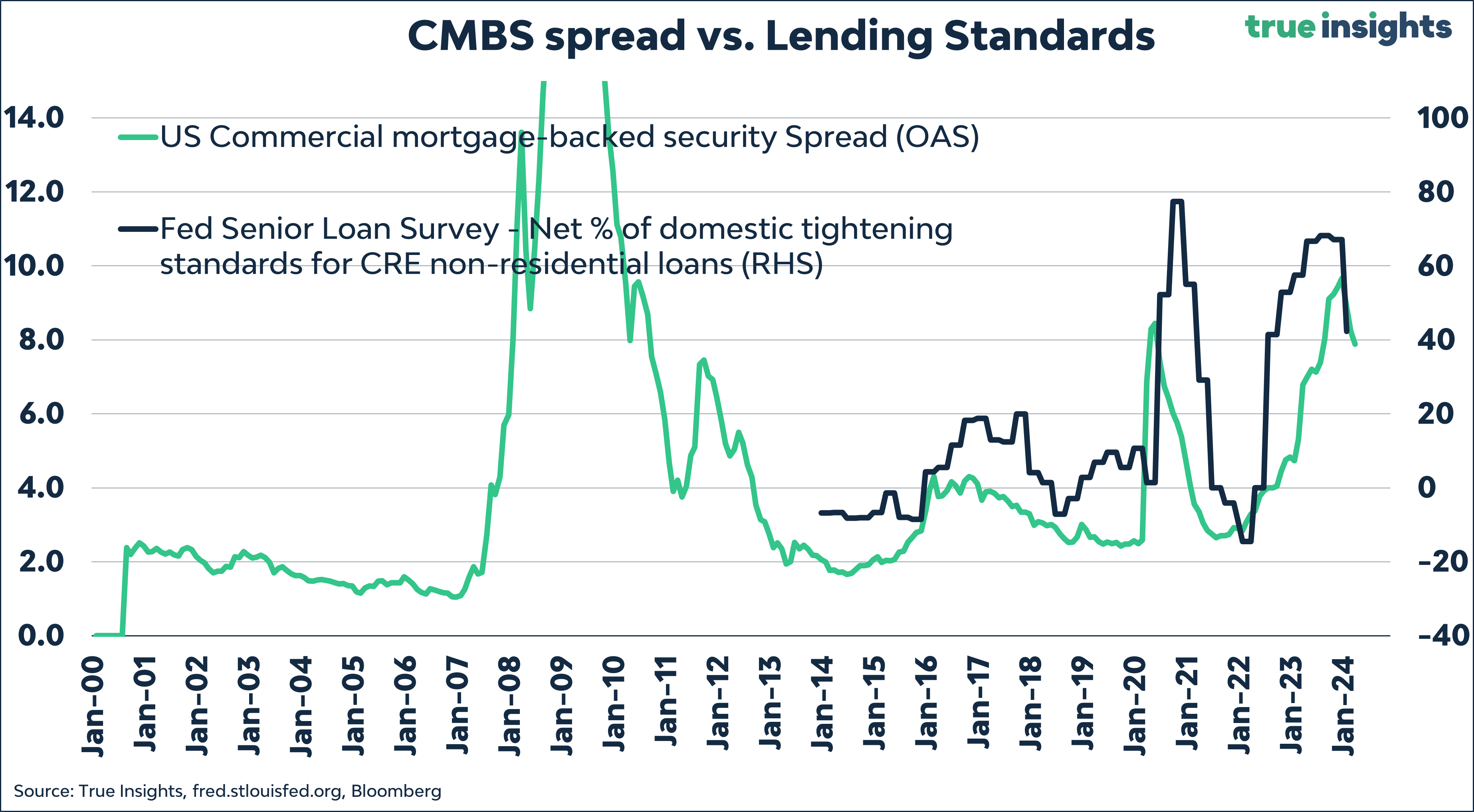

Commercial Mortgage-Backed Security spreads align with the SLOOS but remain high for a reason. The likelihood of a credit event from this sector remains significant, especially now that interest rates have risen again.

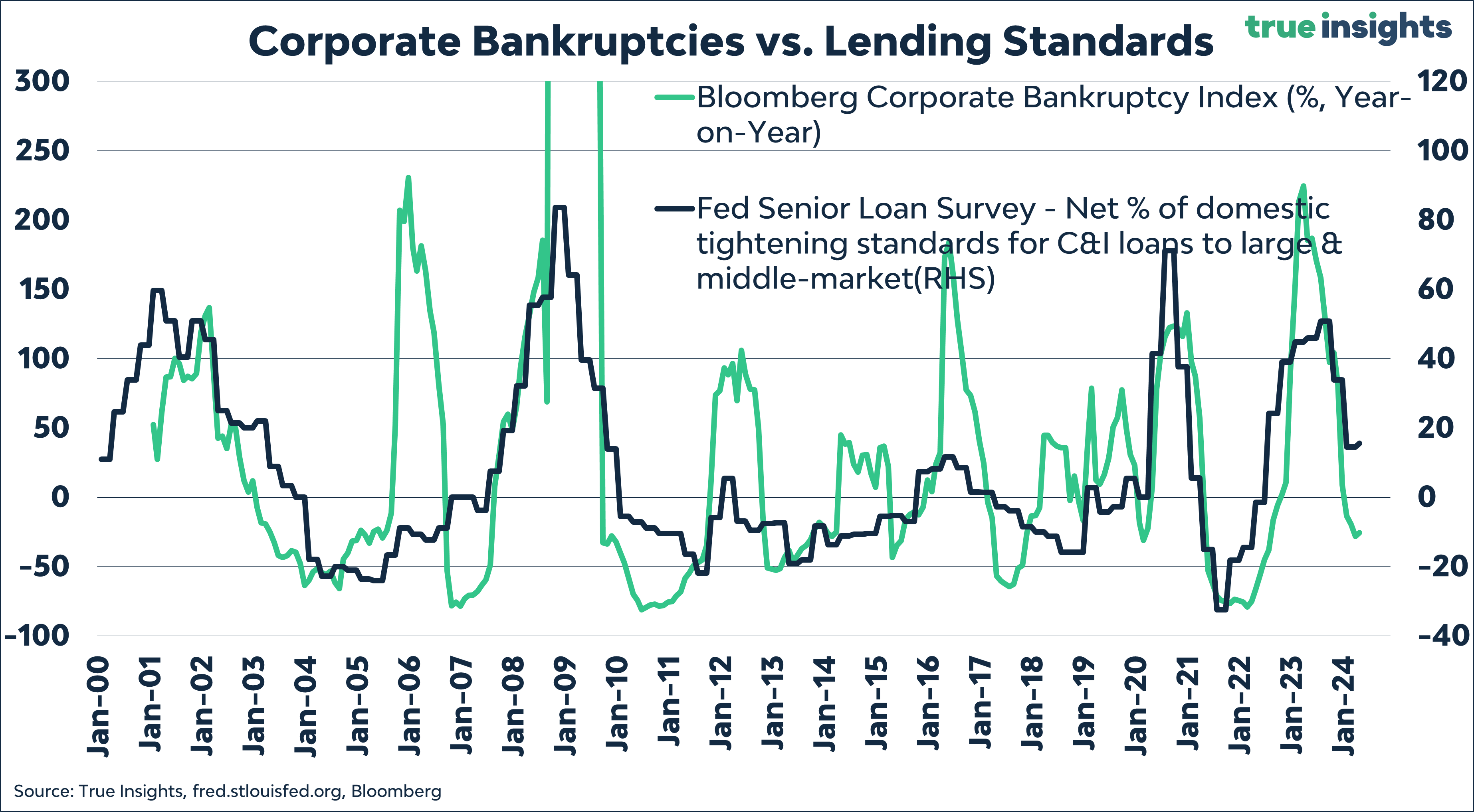

Finally, a chart suggests that the recession may already be behind us. In response to the rapid increase – often it’s the speed of change rather than the level that matters most – we’ve just gone through a complete bankruptcy cycle.

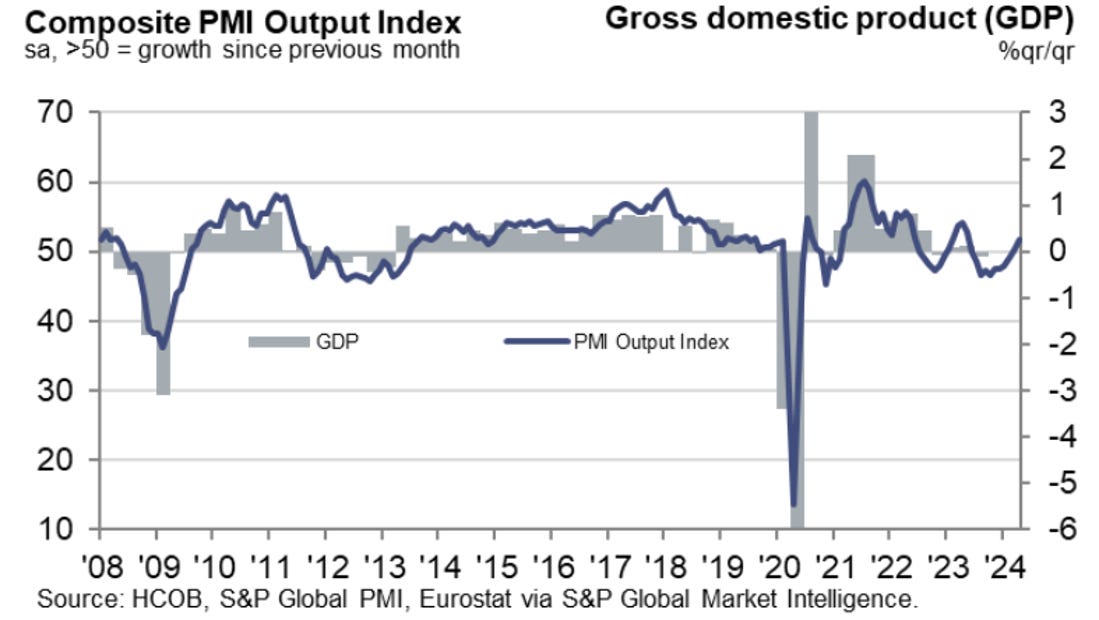

PMIs are on the rise

The recent PMI data partially confirms that we may not necessarily be at the end of the economic cycle.

In the Eurozone, the Composite PMI (Manufacturing + Services) has risen well above 50, indicating that Eurozone GDP growth may finally move away from that dreaded 0%.

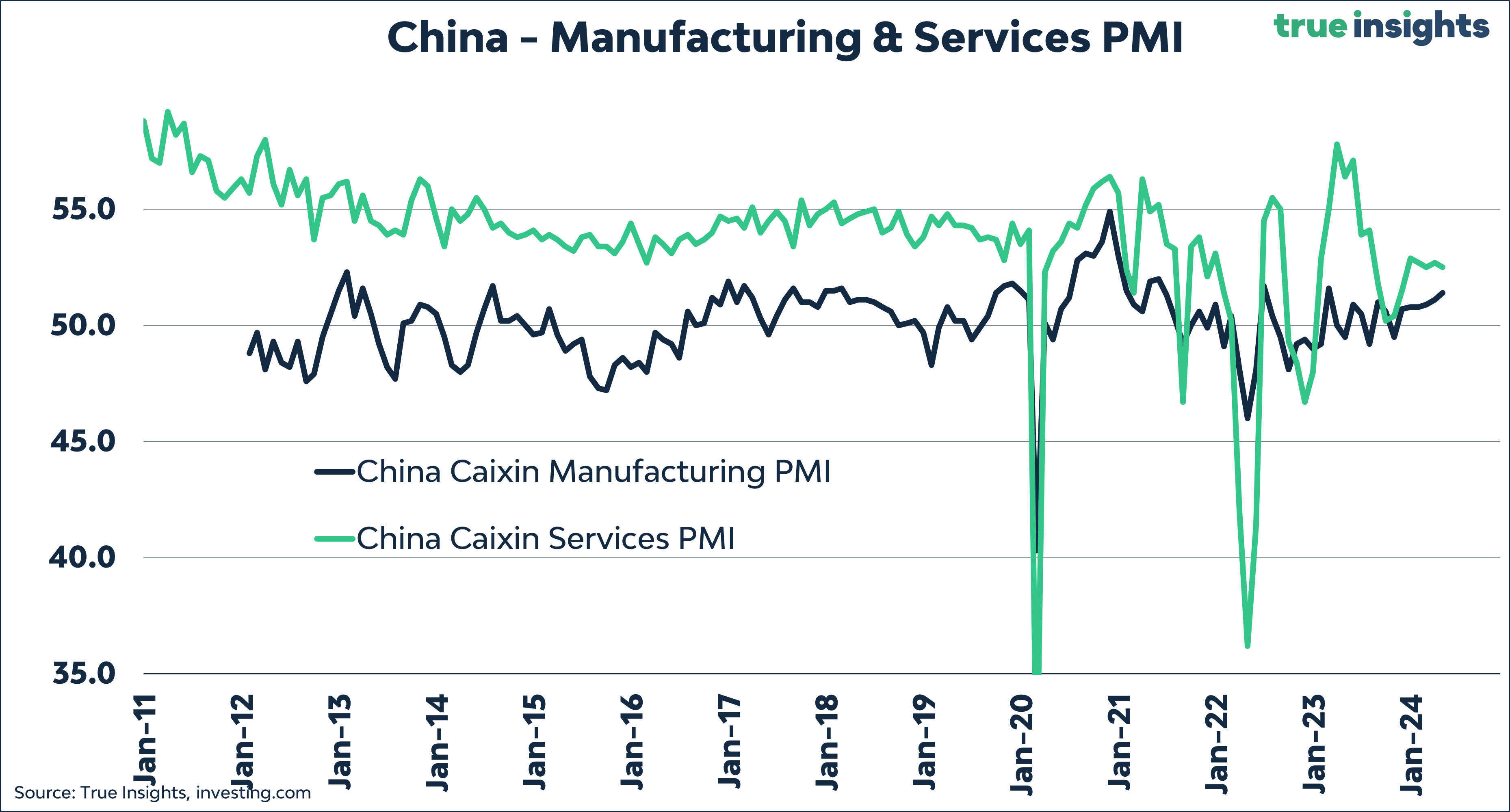

Similarly, in China, we see a steady improvement in PMIs.

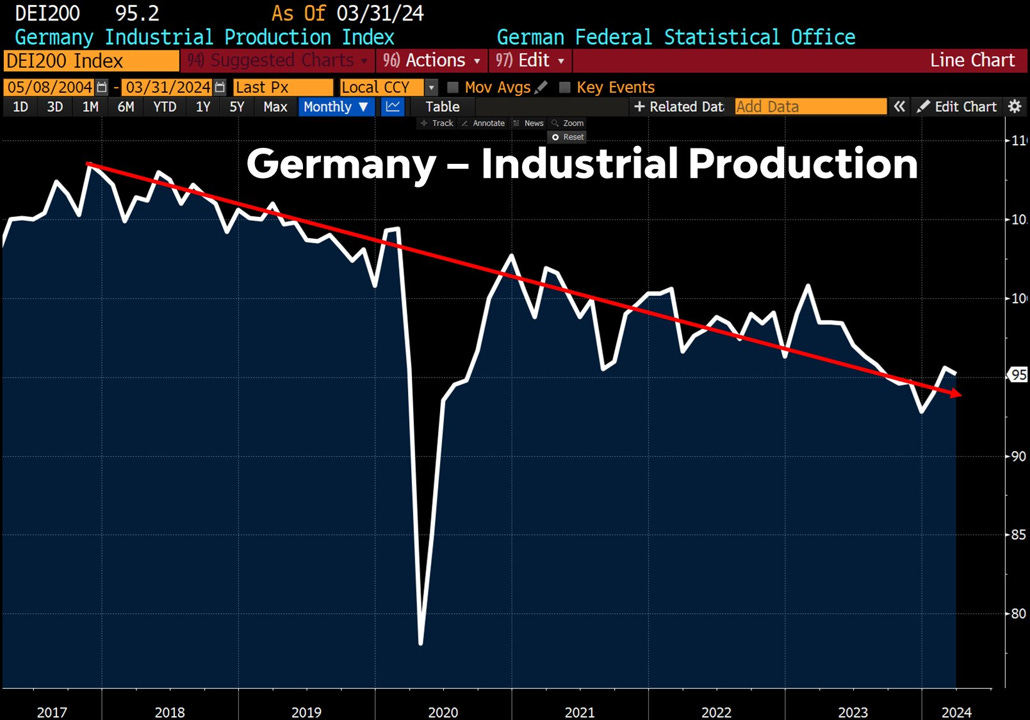

Not everything is rosy. Meanwhile, industrial production in Germany continues to decline, undermining its status as a global manufacturing powerhouse.

There are various reasons for this:

Poor energy policy, Energiewende (sustainability efforts began well before 2017; focusing on the war is too short-sighted)

-Brexit (occurred in 2020, but the trend may have started earlier)

-Covid (no comment needed)

-Loss of competitiveness (German manufacturing goods are expensive)

-China experiencing its real estate recession (seems plausible)

-EV troubles (Germany was late to the EV party)

-Bad management (quality of politicians has severely declined)

I guess that all of these factors are at play!

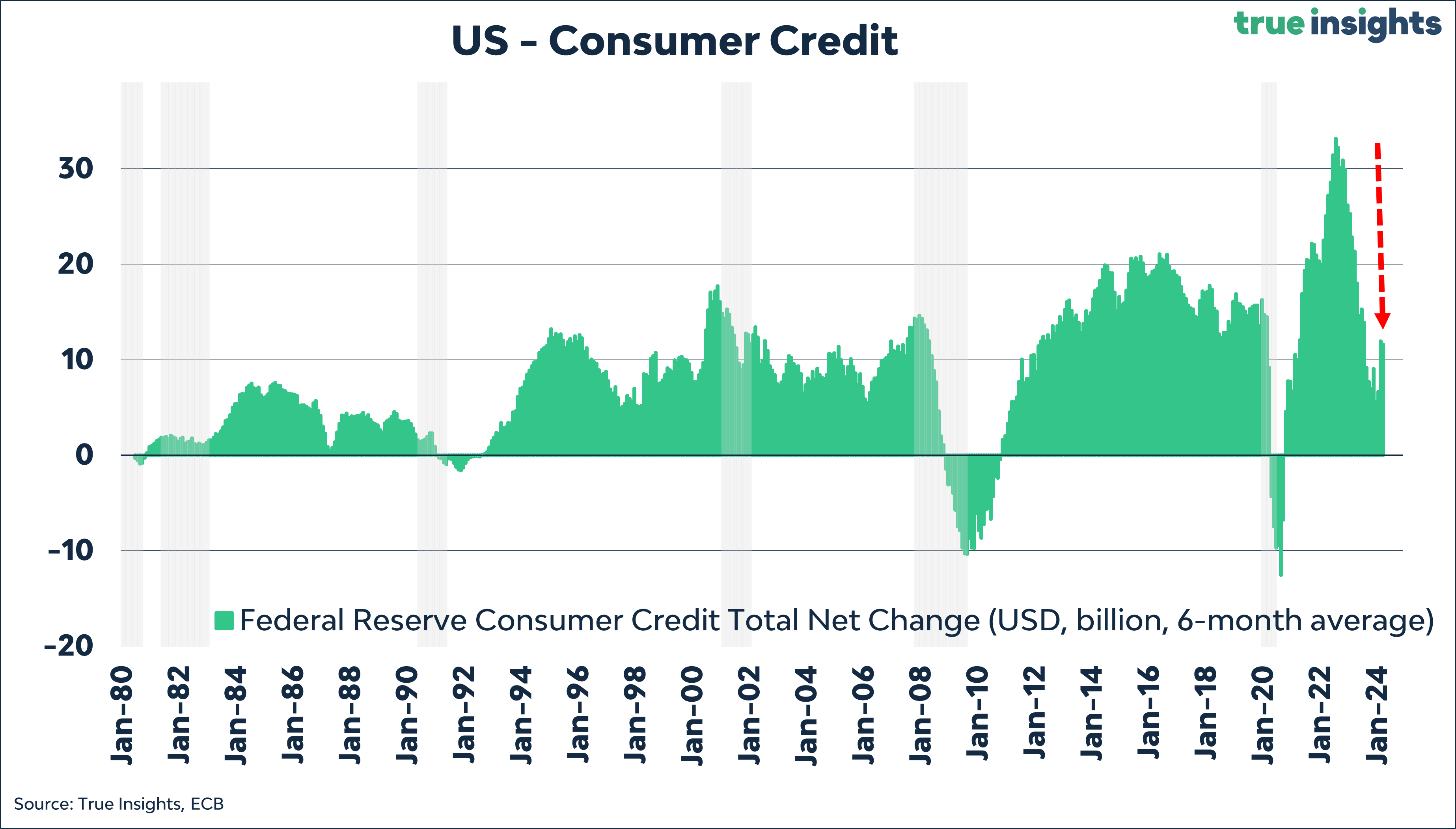

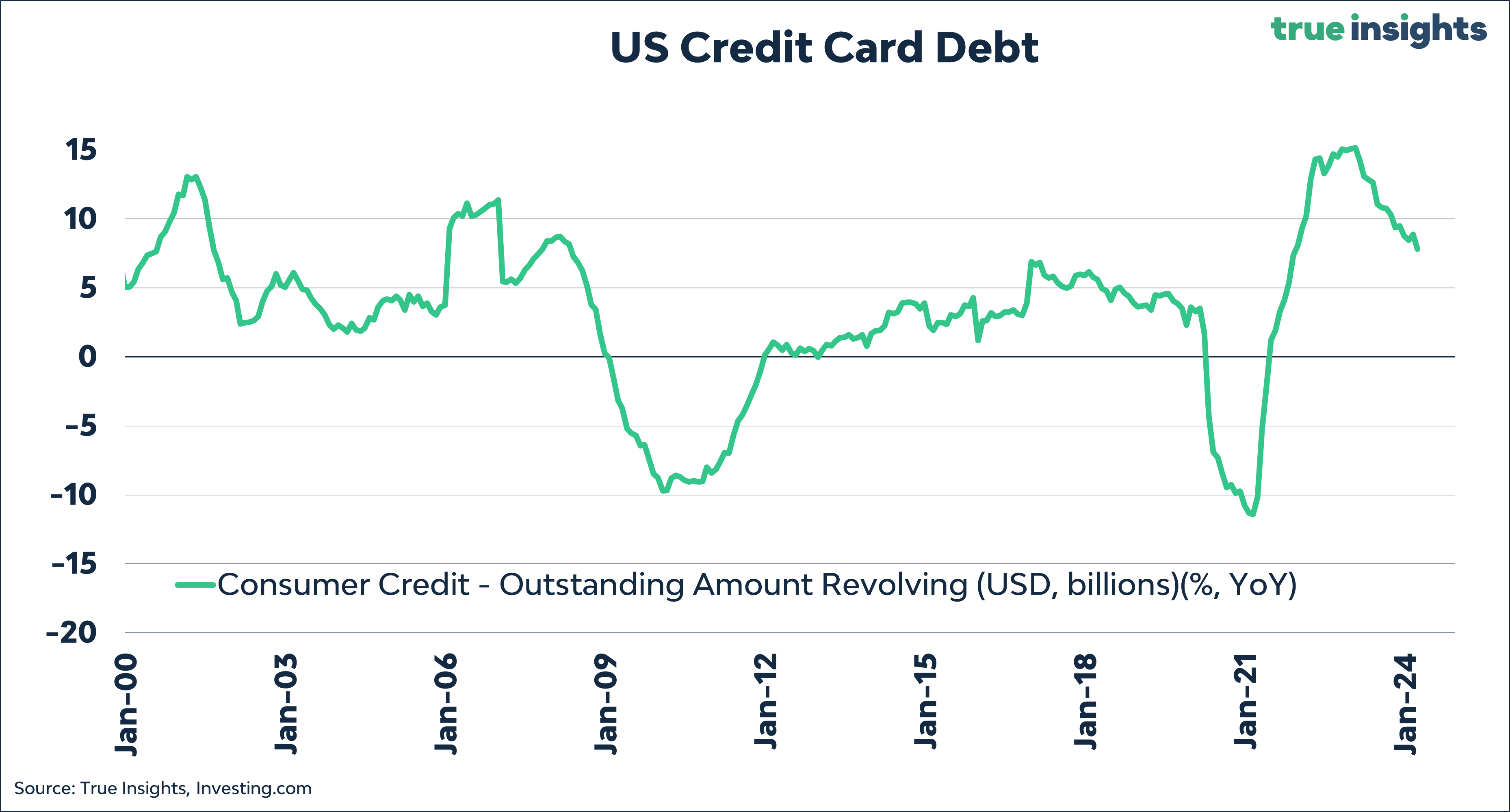

US Consumer Debt

Consumer debt is not the primary concern. While I like to look at total debt-to-GDP ratios, the composition of debt is also important. US household debt is far less of an issue compared to government debt, even though the US issues the world’s reserve currency. Printing more money will have major repercussions for the relative performance of asset classes.

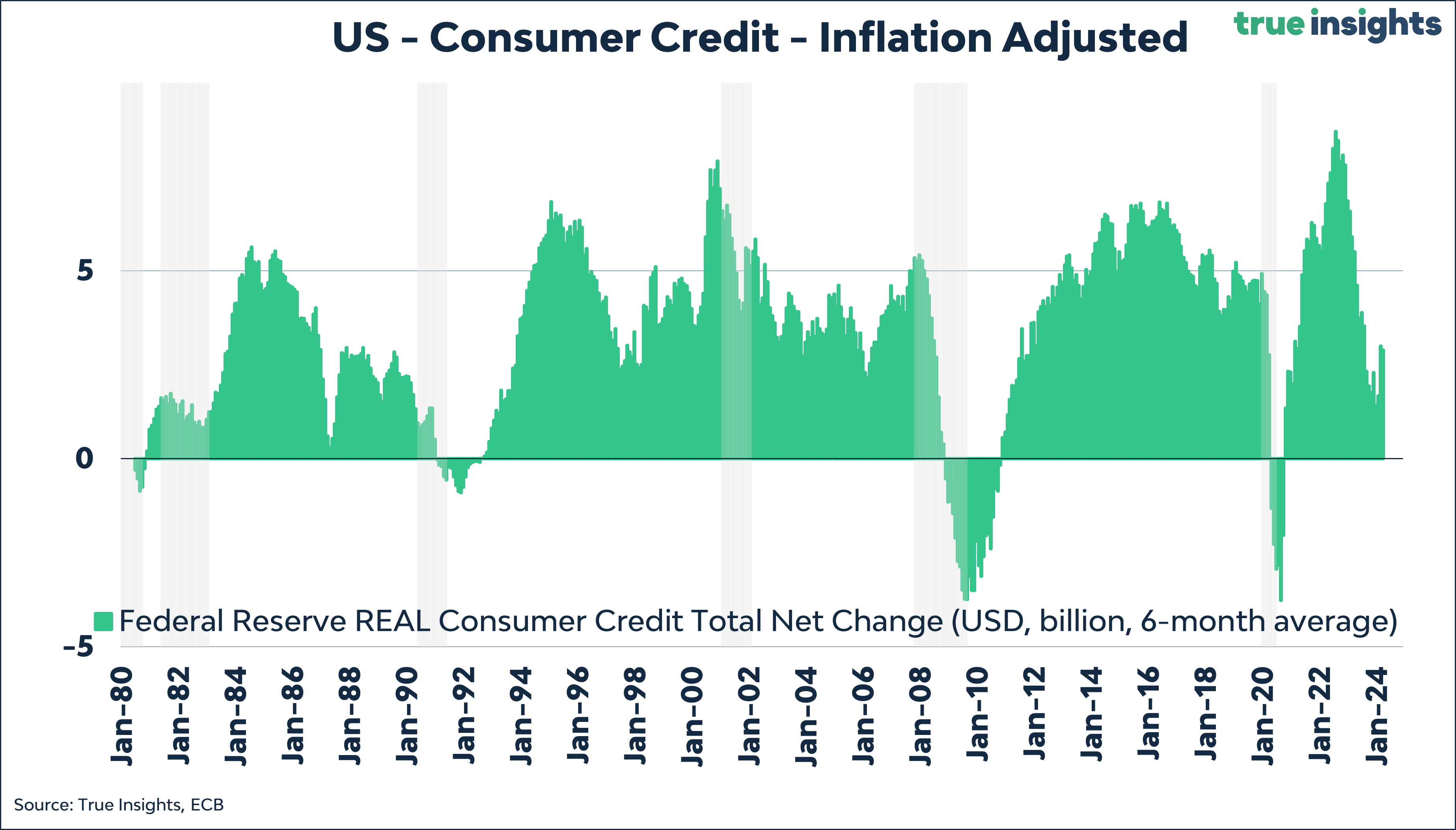

Anyway, the chart below shows the 6-month change in consumer credit. Although there has been some acceleration in the last two months, the growth in consumer credit has significantly decreased, although it remains above the long-term average.

But this is mainly because inflation also remains relatively high. To get a better picture of the growth of US household credit, I adjusted the numbers for the Consumer Price Index. This appears far less exuberant than headlines suggest.

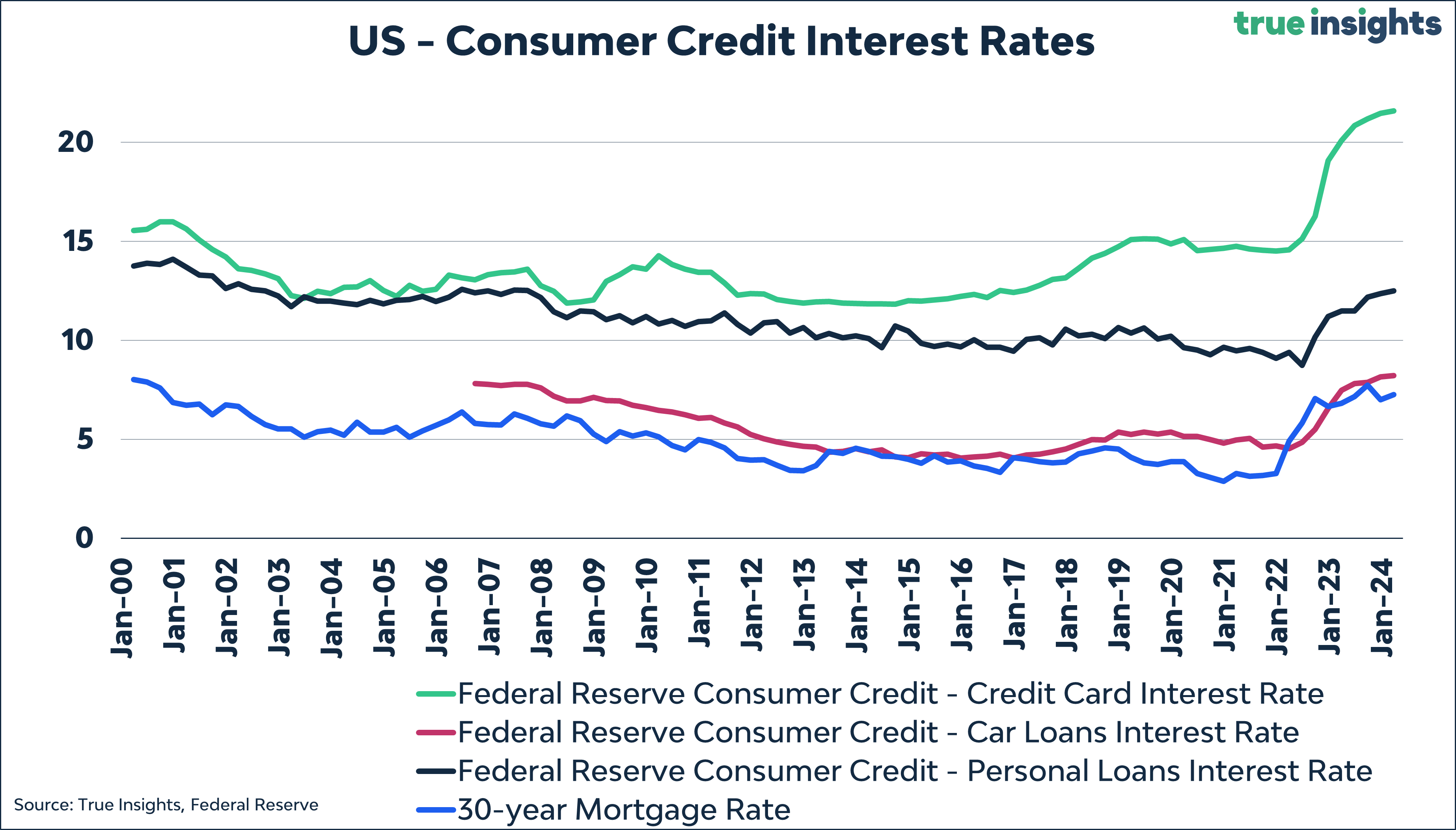

Of course, there is the well-known ‘higher for longer’ risk. However, compared to the past, yields on credit card debt have risen to unprecedented levels.

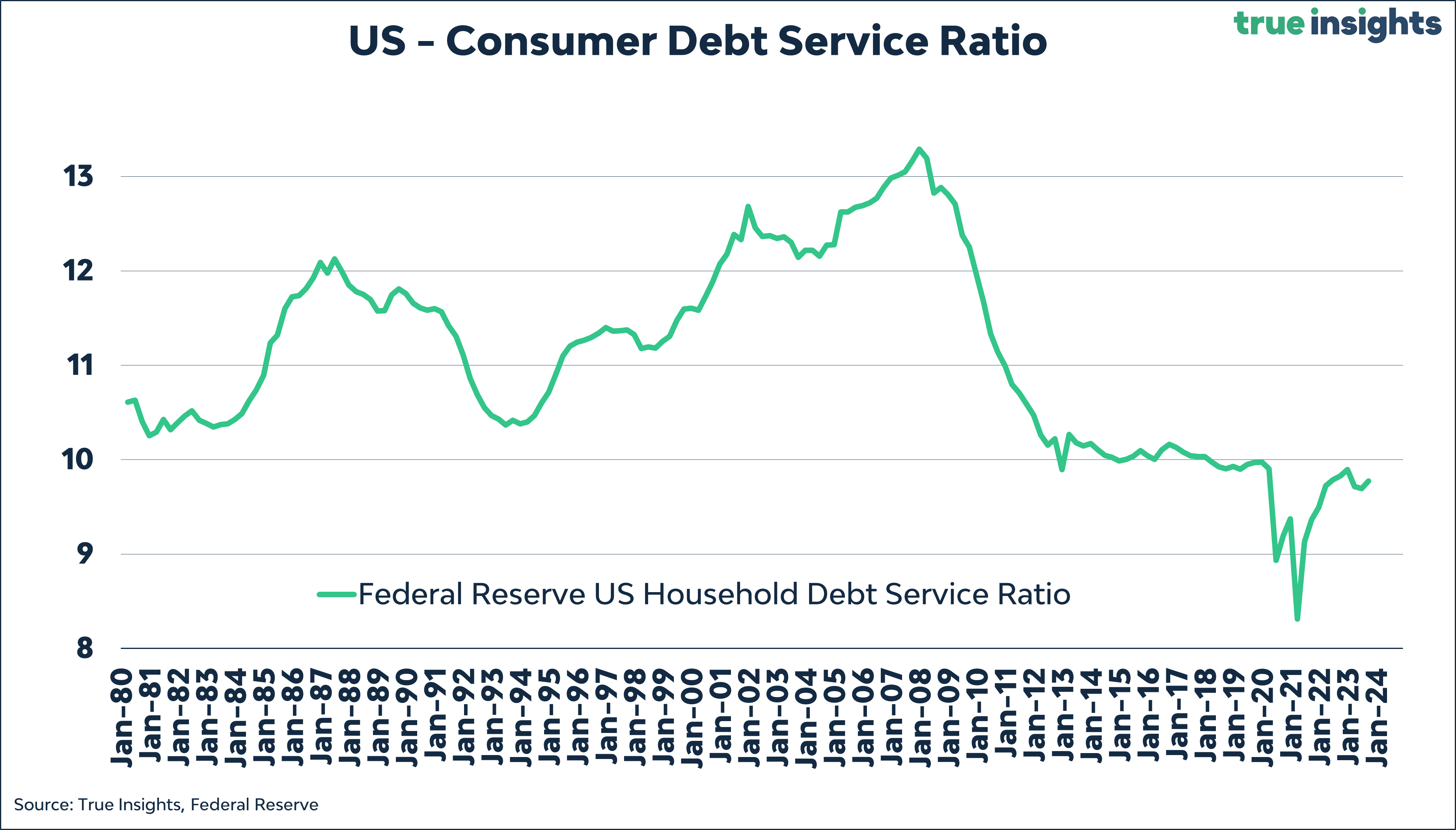

The Consumer Debt Service Ratio confirms that, while debt-related risks are elevated, household debt is not the direct cause.

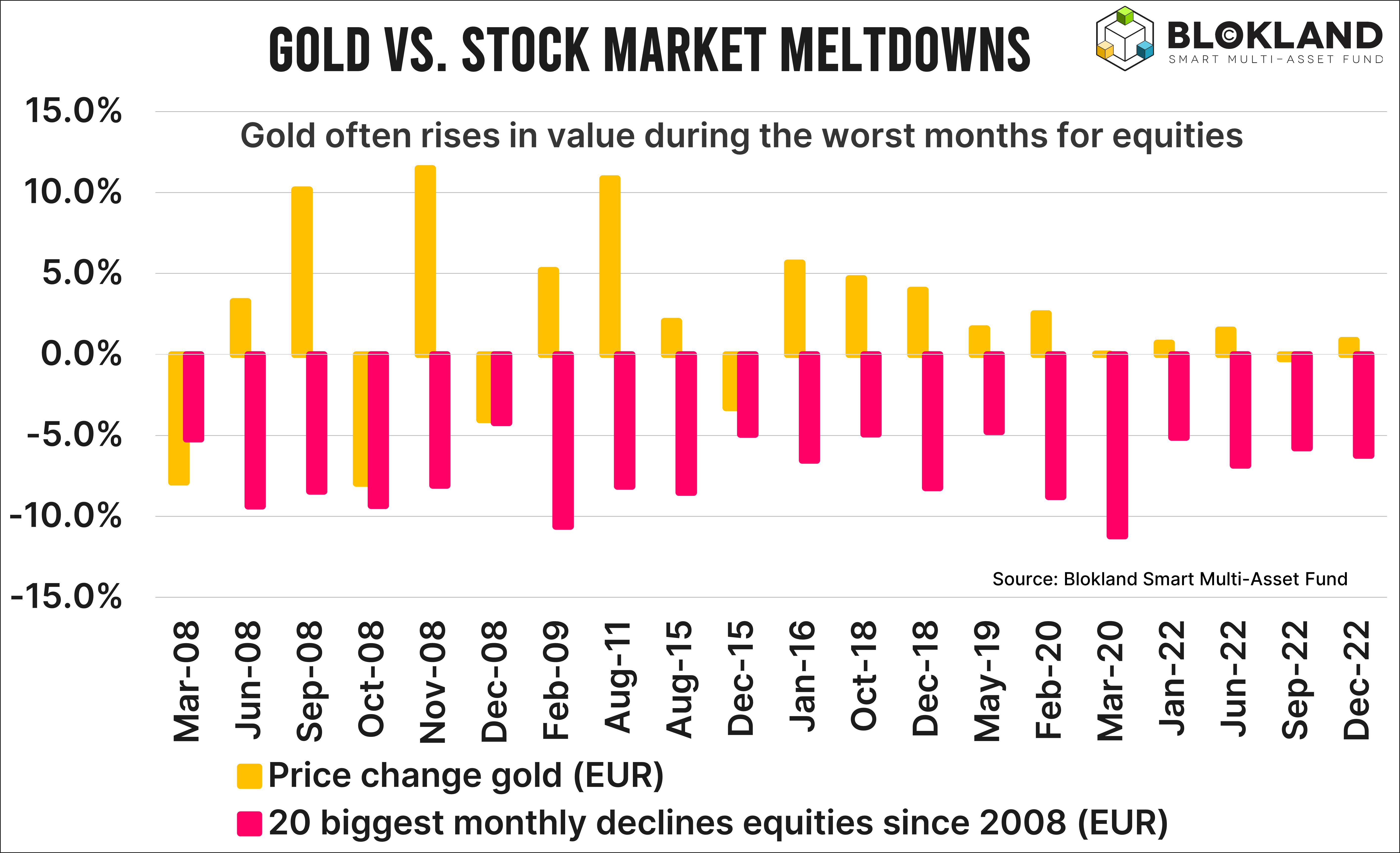

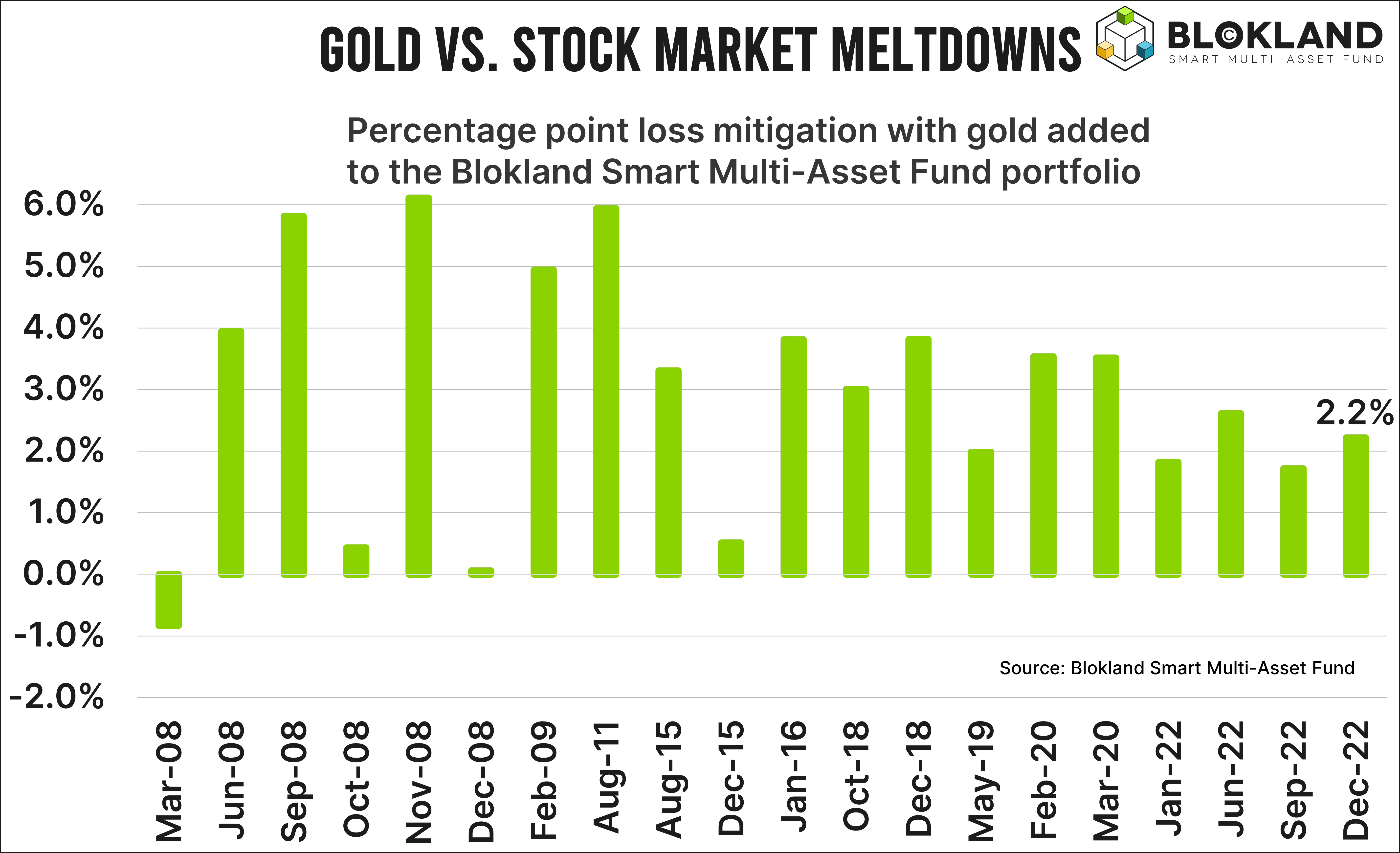

Got gold?

Earlier this week, I wrote about the excellent diversification skills of gold added to equities:

In the 20 worst months for equities, stock prices declined by a whopping 7.3% on average.

Gold rose in 15(!) of those 20 months and by 2.1% on average.

Adding gold would have mitigated losses in 19(!) out of the 20 worst months for equities. (The numbers here are based on the weight of Equities (55%) and Gold (25%) in the Blokland Smart Multi-Asset Fund)

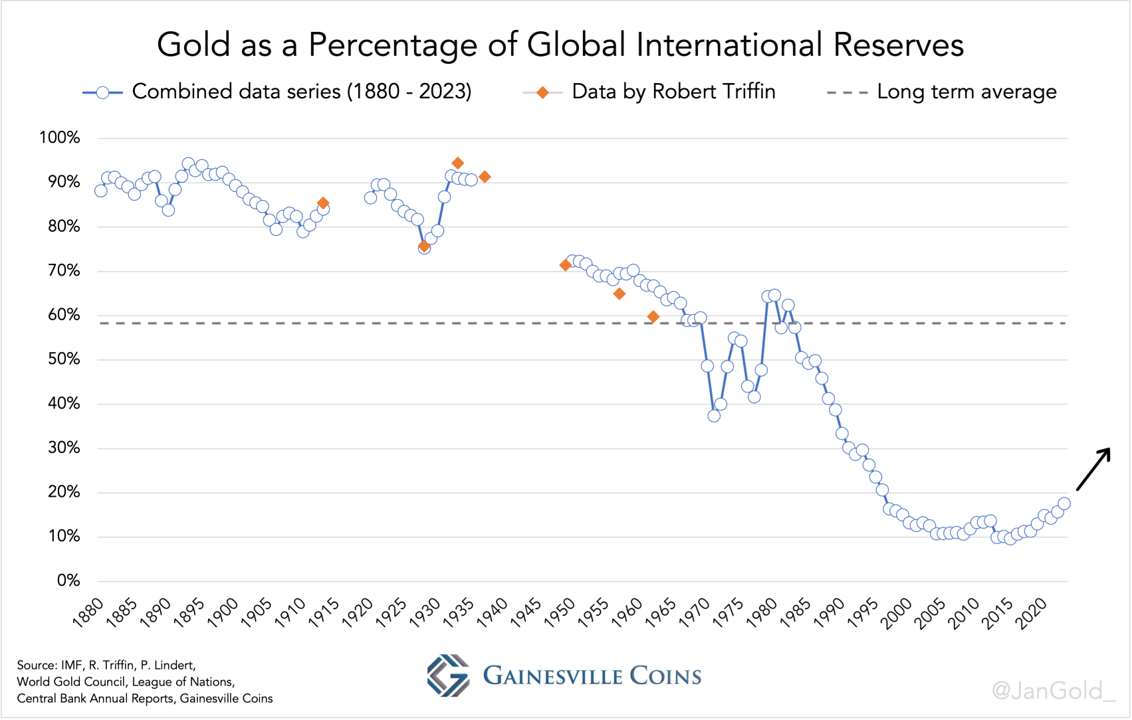

My friend and gold expert, Jan Nieuwenhuijs, wrote another excellent piece on where gold is heading. One of his charts especially stands out:

The weight of gold as a percentage of Global International Reserves is still exceptionally low. This is remarkable given the current state of debts, the desire for de-dollarization (which, in practice, initially results in the depreciation of all other fiat currencies), the confiscation of Russian central bank assets, and simply the desire for optimal diversification of reserves.

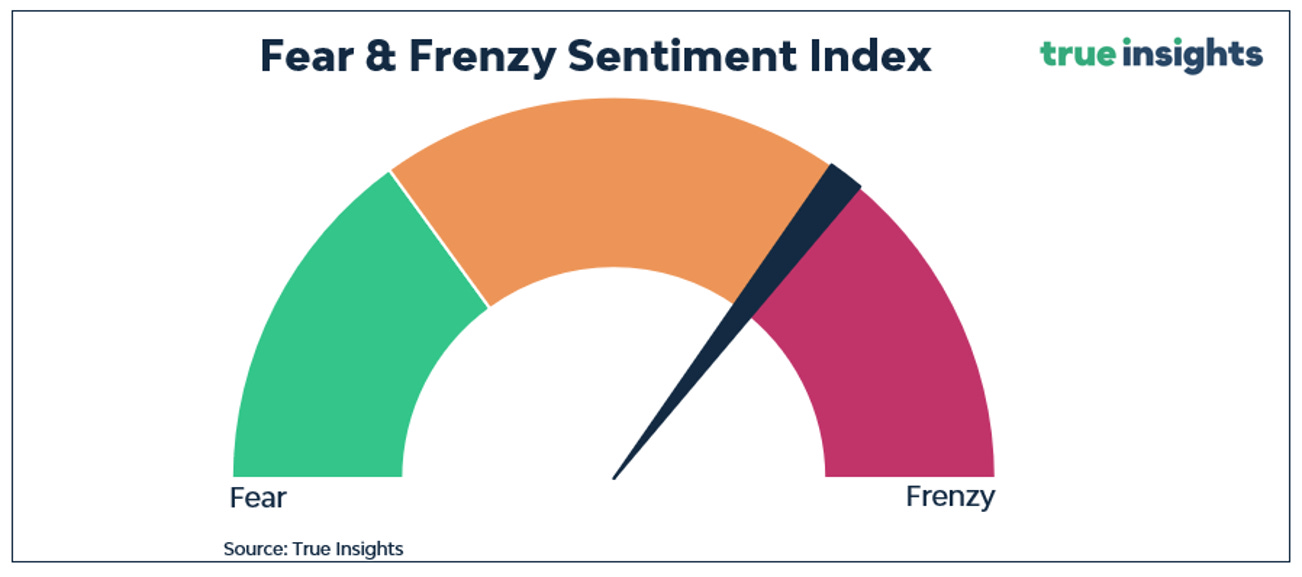

Sentiment

My Fear & Greed Sentiment Indicator is getting uncomfortably close to ‘Frenzy’ again.

MARKETS