US inflation: Bad enough for Powell to change course?

US inflation: Bad enough for Powell to change course?

For the second month, US inflation came in higher than expected. And while this will not impact the Federal Reserve that much, Powell will have to make an effort to keep short-term rate cuts alive!

For the second consecutive month, inflation has exceeded expectations, raising questions about the ‘stickiness’ of core inflation and its anticipated path toward the Federal Reserve’s 2% target.

The numbers:

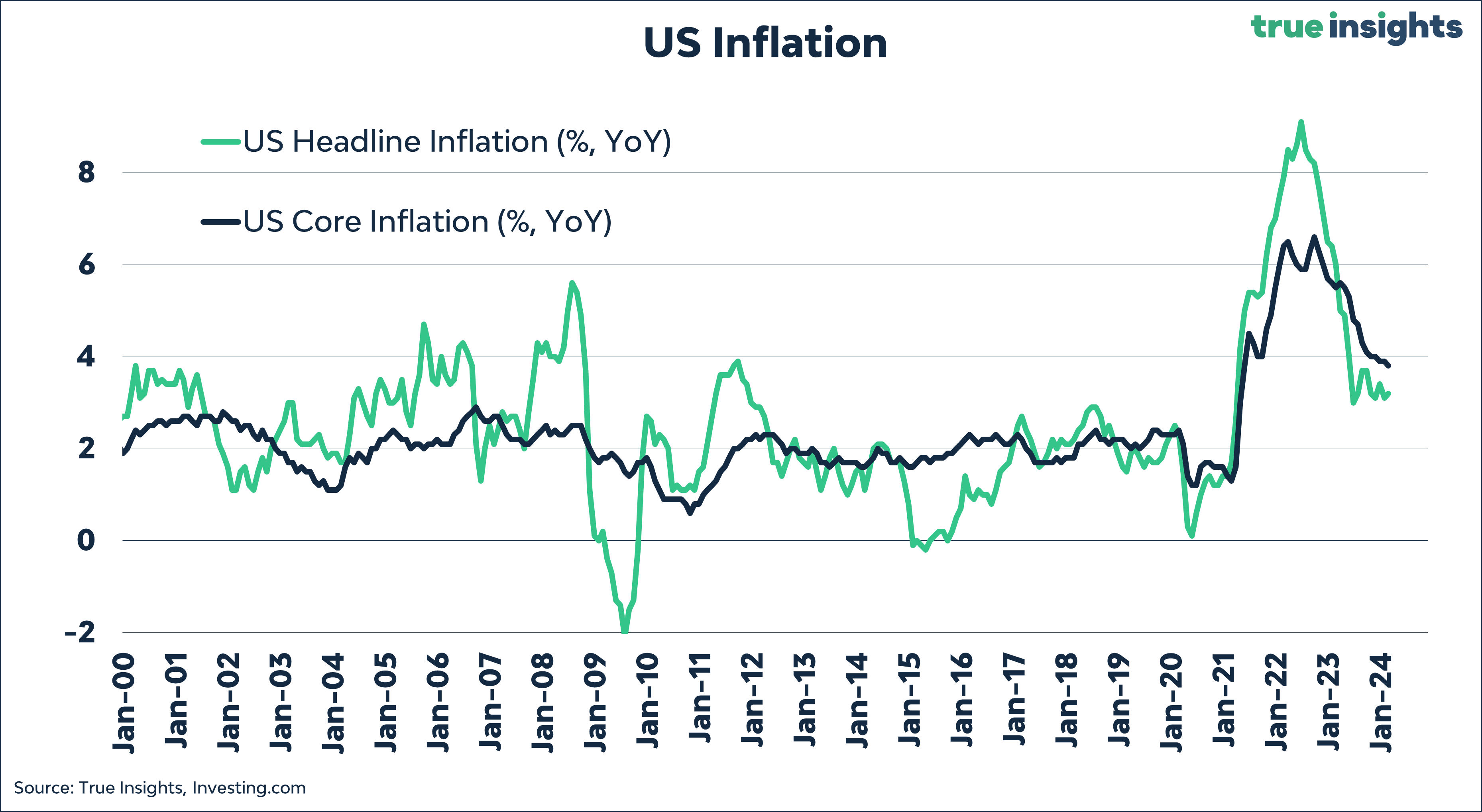

February saw US headline inflation at 3.2%, 0.1 percentage point higher than anticipated, with Core CPI dropping to 3.8%, also 0.1 percentage point above forecasts.

Core CPI increased by 0.4% month-on-month for the second month, which is too much.

The three-month annualized core CPI rose by 4.2%, marking the fastest increase since last June.

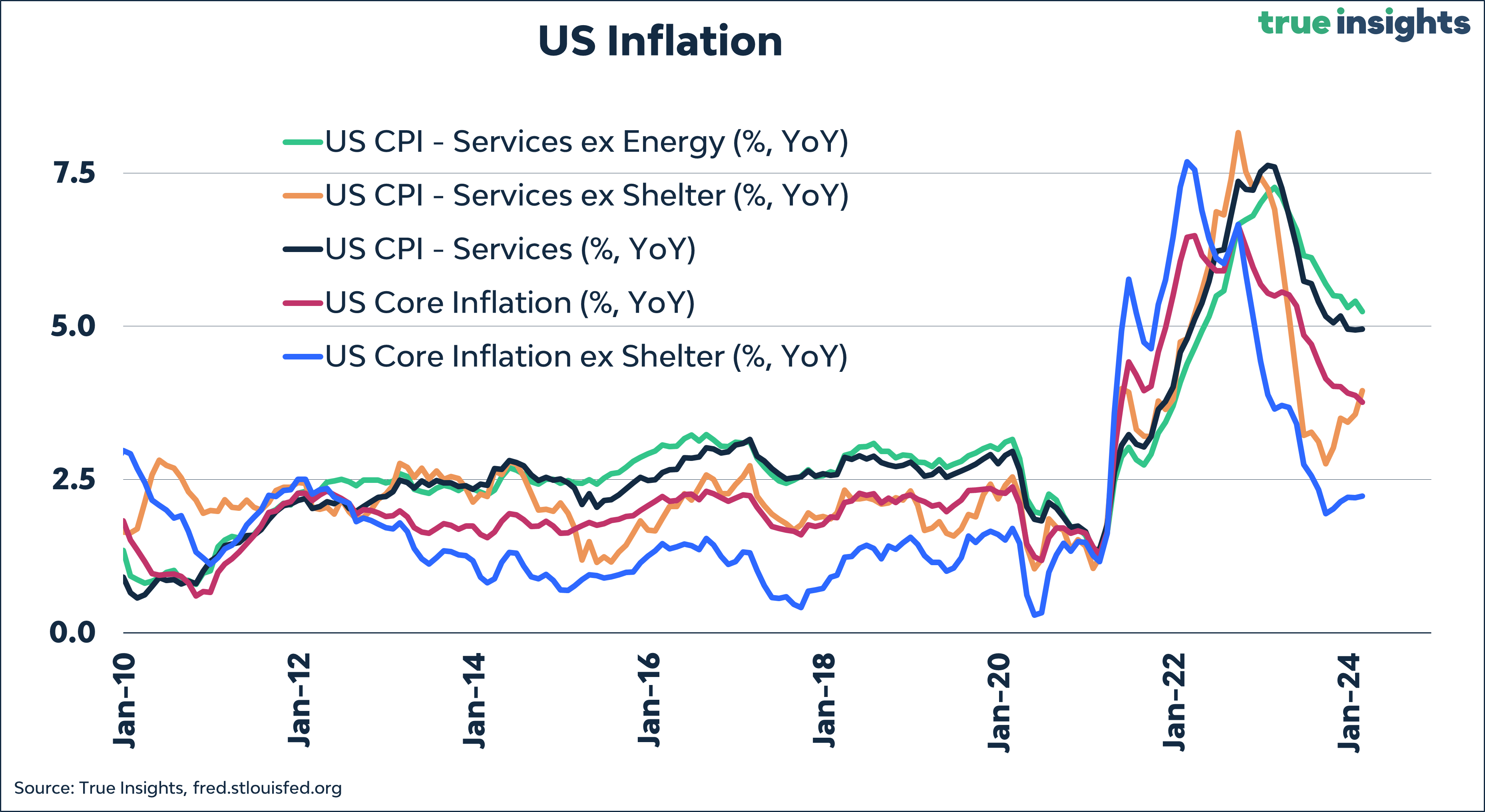

However, like the previous month, the real shocker was the Core Services excluding Housing CPI, which increased to an eye-popping 6.8% on a three-month annualized basis. This makes February, after April to June 2022, the month with the fourth highest Core Services excluding Housing inflation in this cycle.

Including housing, the picture isn’t great either, with Service inflation still at 5.0%, about two percentage points higher than headline inflation.

This means lower inflation must come from deflation in goods prices. While this is still the case for items like used cars, the prices of goods cannot keep falling indefinitely. According to the CPI report, deflation in used cars slowed to just 1%.

Shelter and gasoline accounted for over 60% of the overall monthly increase in core CPI. Although Shelter has a lower weight in the Fed’s preferred Core PCE index, the disinflation trend has now ground to a halt.

Change of direction?

The critical question remains whether this makes a significant difference. We’ll know the precise answer on March 20th, the date of the next FOMC meeting.

But please recall these two lines from Federal Reserve Chairman Powell last week:

‘Interest rates right now are well into restrictive territory.’

‘We’re far from neutral now.’

As of writing, the S&P 500 Index future is up by 0.3%, slightly more than before the CPI report was released.

The 2-year yield is up four basis points, while the expected number of rate hikes has slightly decreased to 3.4 from 3.6 yesterday.

Investment conclusion: Most likely, the latest CPI numbers aren’t the catalyst that ends the stock market rally. The 0.1% higher-than-expected inflation should not deter Powell from his intrinsically dovish stance.

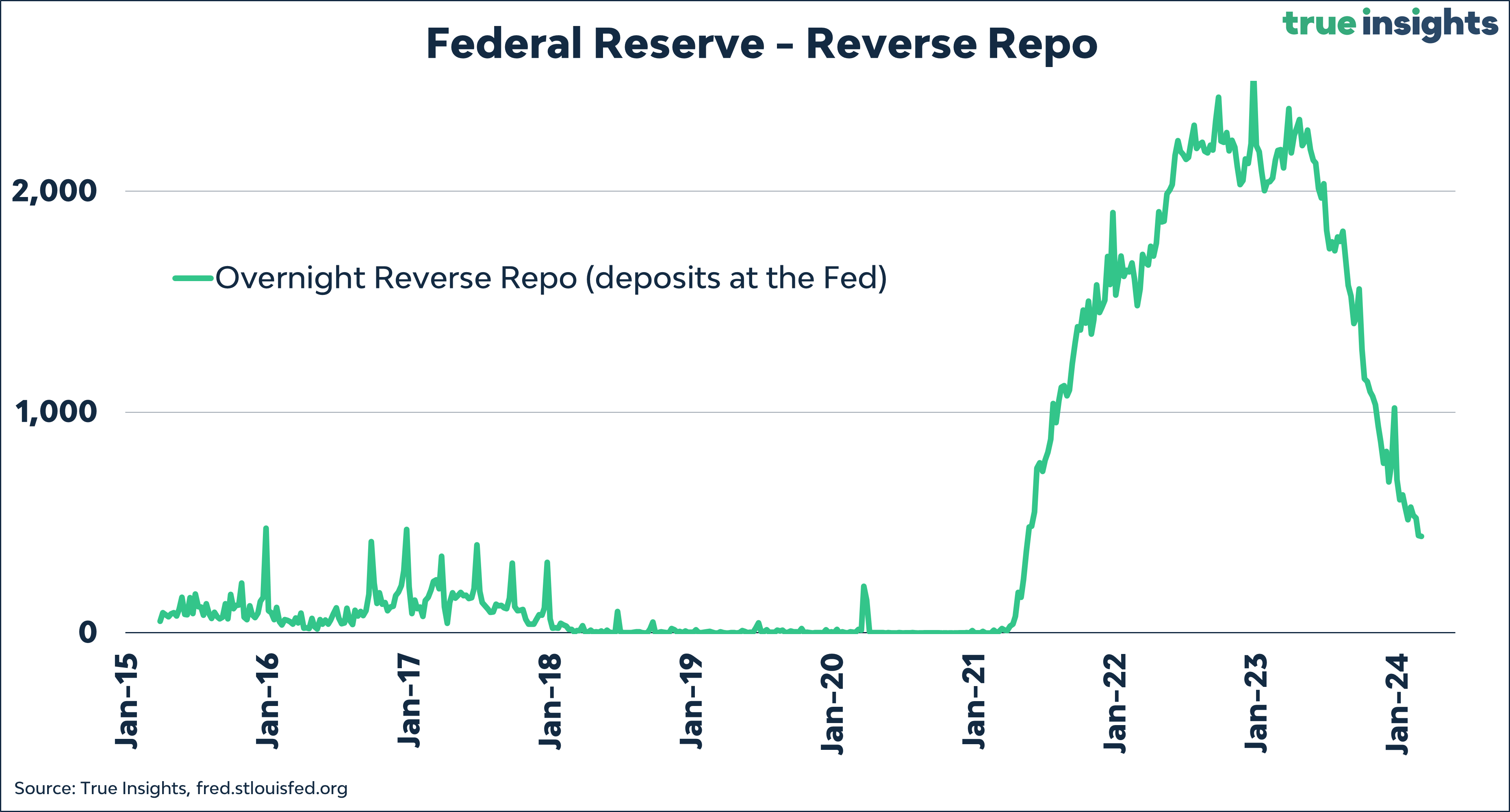

However, some underlying inflation figures remain significantly off the Fed’s target. This means Powell cannot hasten to lower the rates. If Powell feels compelled to adopt a more cautious stance based on the latest CPI numbers, the likelihood of a correction will increase. This is especially true given that issues related to commercial real estate have escalated again in recent weeks while the draining of the Fed’s reverse repo rate facility is impacting liquidity.

I anticipate another somewhat hawkish-sounding FOMC statement followed by a dovish-sounding Powell in the press conference, eager to keep the prospect of a soft landing alive.

What do we know about inflation?

Finally, despite what many economists and central bankers might think they know about inflation, it’s probably not much. Since World War II, we’ve only seen two major inflation trends: the first rising from 1950 to the early ’80s and the second declining from the early ’80s until COVID. However, as history shows, inflation was ‘all over the place’ before 1950.