A Real-Time Estimate of Gold's Market Cap and Bitcoin's Potential Value

My real-time estimate of gold's market cap is USD 15+ trillion, leaving a Bitcoin price target of USD 140-170K.

In last Friday’s Weekly Market Monitor, I highlighted my newly-created ‘real-time’ estimate of gold’s market cap. It strikes me that the data used in the few posts that do pay attention to gold’s market value tend to be two, sometimes even three years outdated. Since I anticipate gold taking on a more prominent role in most (multi-asset) portfolios – with Bank of America data showing that the average allocation by US wealth advisors is only 0.7% – and because the market value of gold is the crucial input for my Bitcoin valuation model, I’ve created a real-time estimate of its market value.

Methodology

The methodology is straightforward. Once a year, the World Gold Council releases its estimates for the above-ground stock of gold. That alone means that using old data is unnecessary. Moreover, the above-ground stock increases at a very steady pace. Over the past four years, it has grown by an average of 1.75% per year, with variations between 1.74% and 1.77%. Assuming this percentage is evenly mined throughout the year, one can reasonably estimate the ‘current’ above-ground stock. This, multiplied by the current price, gives the ‘real-time’ market value of gold.

USD 15 Trillion

Based on the above estimate, the current market value of gold is just above USD 15 trillion. That’s about USD 2 trillion more than most (old) data suggest.

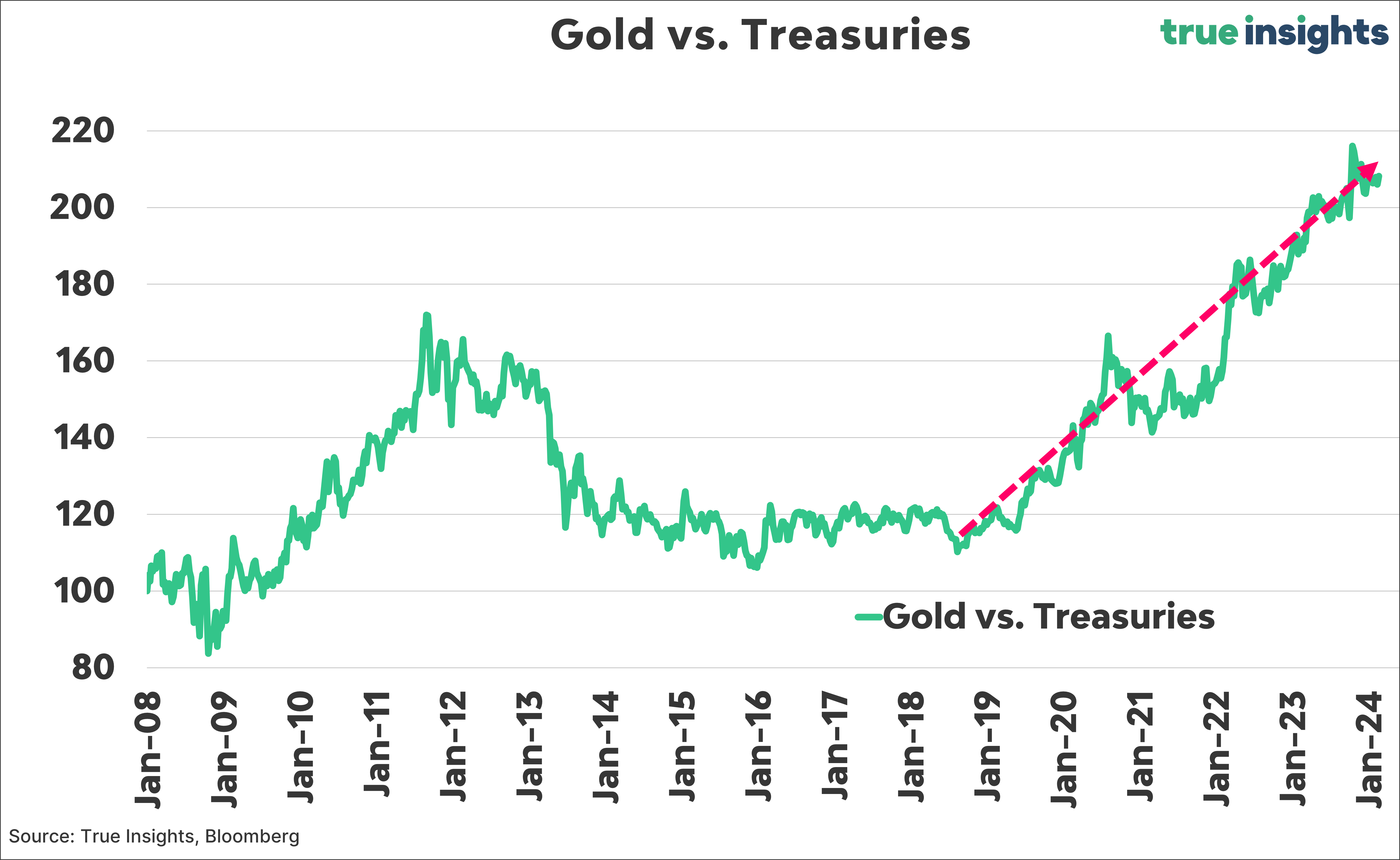

Gold vs. Treasuries

It should come as no surprise, but I expect bonds to be less attractive than they used to. Bonds can still realize solid returns now and then, but I anticipate structurally low-interest rates over the long term. Moreover, inflation is likely to be higher and more volatile, thus increasing the odds of negative real returns. Finally, I expect bonds to become more volatile due to growing concerns about debt sustainability. This means less diversification in a multi-asset portfolio.

Because of bonds’ diminishing attractivity and the ongoing accumulation of debt, scarce financial assets will outperform. The chart below shows my real-time market value of gold compared to the market cap of bonds since the beginning of 2020. This starting point is because COVID decisively confirmed that governments, with central banks as their extension, will try to address any crisis by drastically lowering interest rates and issuing loads of new debt. Since COVID, the market value of gold has risen relative to bonds, even though the latter are being issued in unprecedented amounts.

It also makes sense to look at the relative price momentum. This is shown below from the Great Financial Crisis, when central banks began their extraordinary policies (except for the Fed during World War II). Gold has outperformed bonds.

Of course, nothing moves in a straight line, but I expect both trends to continue over the next ten to twenty years.

Bitcoin Value Update

My case for Bitcoin is that it has the potential to function as, or indeed already serves as, digital gold. This means that the valuation of Bitcoin should be derived from the value of gold, which presents a second important reason to have access to a real-time estimate of gold’s value.

Deriving the value of Bitcoin from gold’s market cap looks like this:

A key assumption is that gold’s value is largely determined by its role as an insurance premium, stemming from gold’s long-term status as money and a store of value.

To put a number on this, I look at gold’s relative scarcity compared to silver. Estimates vary, but gold is about 17 times scarcer.

Currently, gold is 90 times more expensive than silver. The relative scarcity and price reveal how much of gold’s market value is explained by the value of the insurance premium. Currently, this is USD 12.3 trillion, or more than 80% of the real-time market value.

Next, I assume that this insurance premium – again driven by issues around debt sustainability – will increase by 5% each year, which is quite conservative.

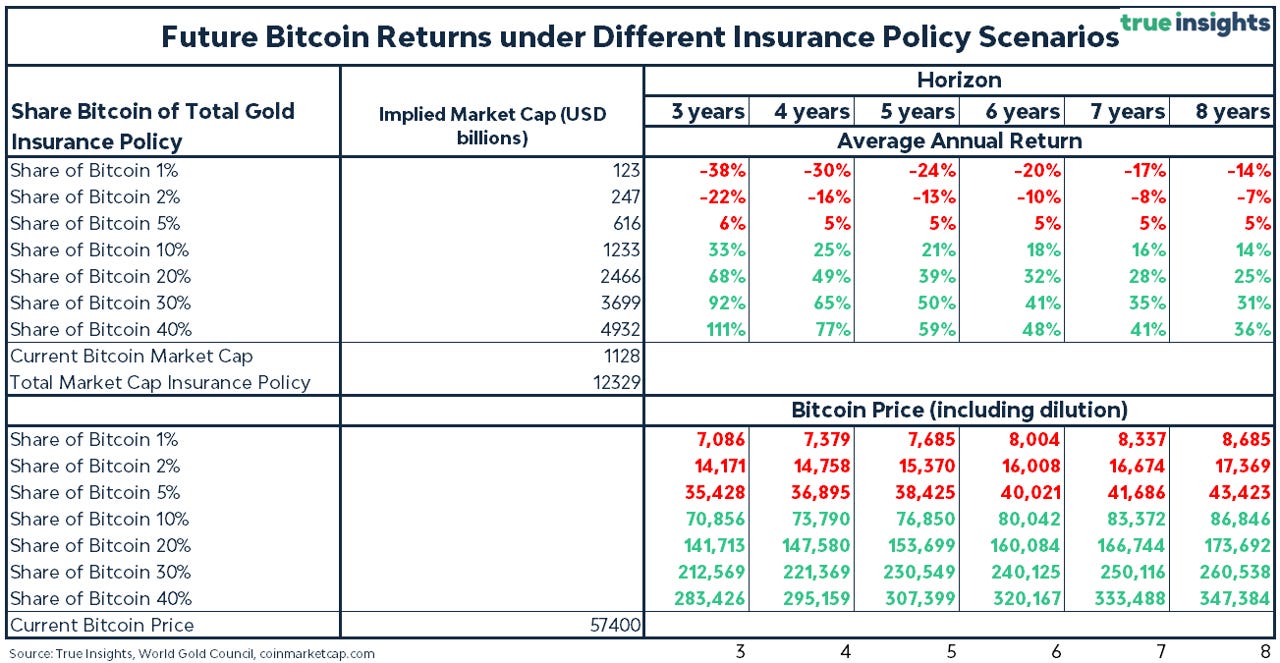

Finally, I look at Bitcoin’s market value in seven scenarios, each with a different share of Bitcoin in the total insurance premium of gold, ranging from 1% to 40%. I also vary the speed at which Bitcoin reaches these shares, from three to eight years.

This results in the table below. My base case is that Bitcoin’s market value will grow to 20% of the total insurance value of gold. This yields an estimated price per Bitcoin, accounting for dilution, of USD 141,000 to USD 173,000. I’m sticking to that 20% for now, but judging by both price formation and especially the strong inflows into spot Bitcoin ETFs, Bitcoin is currently on track for a higher share. However, we should consider the possibility that Bitcoin might ‘eat into’ a part of gold’s insurance premium. Unsurprisingly, the numbers in the table are nothing more than educated guesses. Yet, having a real-time estimate of gold’s market cap makes a lot of sense.

By the way: you expect lower interest rates for the current year, which means that the FED will cut rates, which means that some cataclysmic event will happen, because the FED doesn't cut rates out of the goodness of its heart, even more so as JP doesn't want to be remembered as the one who didn't manage to curb inflation. Any thought about the kind of event that might happen? Another banking crisis after lifting of the BTFP perhaps?

Yes, a lot of wild guesses, but nevertheless a nice piece of analysis and deduction. Thank you